Selling your healthcare business, especially when you're the founder or long-time owner, is one of the most emotionally complex and taxing journeys you'll ever take. The sale is not just a financial transaction. It's the culmination of years, and sometimes even decades, of work. The lengthy process of selling your company brings a whirlwind of feelings, expectations, excitement, and challenges that can — and often will — impact every step of the transaction process.

In our extensive history and experience working with healthcare business owners, there's a recurring psychological pattern we've seen play out time and again. And it's this pattern — this rollercoaster of emotions — that can make or break a deal.

You Believe Your Healthcare Company is the Best

By the time you decide to sell your business, you've likely built something you believe is exceptional. With all the long hours you've put into the company, you know it inside and out. You may know the inner workings of your business better than those of your home. You've spent countless hours working to optimize operations, assembling a talented supporting team, building a strong customer base and referral network, and establishing a brand and reputation that customers and partners have come to trust and value.

When you look at your company, you see an asset that you strongly believe should command top dollar.

That belief is important. It's that confidence which has helped you find success with your business and will drive your desire to find a buyer that truly understands and appreciates the value of what you've worked to build.

But that belief is also the foundation for a deep emotional attachment that can complicate matters as you move through the transaction experience.

The Initial Surge of Seller's Motivation

When you first make the decision to bring your company to market, it's like flipping a switch. After what was likely extensive contemplation, you make the call, and the sales journey begins. Once that happens, the adrenaline will likely kick into overdrive, and you operate with intense focus and energy, which is exciting and one of the reasons many CEOs become addicted to healthcare mergers and acquisitions (M&A). You engage an M&A advisor, gather documents, clean up financials, and undergo a healthcare business valuation. You work with the advisor to assemble your detailed confidential information memorandum (CIM).

The first discussions with potential buyers fill you with excitement and nervousness. You rehearse talking points and then overanalyze your delivery afterward. You try to read between the lines of every question asked of you and your advisor and every follow-up email you receive.

This first surge of motivation that comes with bringing a company to market can make the beginning of the transaction process feel like a sprint.

And that's potentially a big trap.

The Transaction Process Slows, But You're Still Running

After the first few weeks or even few months of research, preparation, outreach to buyers, and calls, the deal process inevitably slows down. Gaps between communications grow. Buyers go dark temporarily as they work through their own — and extensive — diligence processes. A process that once seemed urgent now begins to feel sluggish, which naturally makes you uncomfortable and a little bit skeptical about the future.

At this stage, your motivation begins to shift. You're still committed to the transaction, but you're no longer sprinting. It's more like you're jogging or walking. Some days, there's no movement at all.

Despite all the work that's gone into the transaction, the finish line is still a ways away.

Under LOI: An Emotional Letdown

When your company finally goes under a letter of intent (LOI), it justifiably feels like a huge milestone. But emotionally, this is where a seller's psychology can really start to change.

You feel like you're in the home stretch, but in reality, you're about halfway there.

Due diligence accelerates. The quality of earnings (QoE) evaluation starts. Legal teams get involved or further engaged. The buyer starts asking more prodding questions that can feel personal at times. Some questions may have you believing that the buyer is undervaluing or misunderstanding your business. Conversations get tougher, and the excitement you had for selling your company crashes.

Then comes the fatigue.

Fatigue as a Common Deal Killer

By the time you're in the final stretch, which includes steps like negotiating the purchase agreement, resolving working capital targets, answering diligence questions for what feels like the tenth time, it's only natural to feel exhausted. After all, you've also been trying to run your company while knowing the end of your ownership is on the horizon. The team members you involved in the transaction are tired, and the rest of your staff may sense something big is happening behind the scenes. Your advisors are juggling a hundred things. And emotionally, you're drained, and you may even doubt whether you should have started this process in the first place.

This is the part of the transaction experience that is often unknown, surprising, and disappointing.

What we sometimes see in our seller partners at this stage is a kind of emotional paralysis. Owners slow down. They stop responding to emails as quickly. They delay document requests. They take longer to make decisions. They express skepticism in the buyer.

These actions typically don't stem from a lack of desire to close the deal. More often, it's simply that they've run out of gas.

And that, in the words of Kenny Loggins, is the "danger zone." Healthcare transactions don't usually die because of a single issue. They die from a loss of momentum. Buyers get nervous. Timelines slip. People — including the buyer's team — start second-guessing. Before you know it, the whole deal unravels and it's largely back to square one.

The Healthcare M&A Marathon Mindset

The key to succeeding — and surviving — in the prolonged sale process is understanding that a healthcare business transaction is almost never a sprint. It's more like a marathon. For some deals, it could even feel like an ultramarathon. From the get-go, you need to try to pace yourself — both emotionally and mentally. It's okay to feel everything talked about in this column: pride, anxiety, excitement, doubt, concern, and even grief. But what matters is showing up consistently, focused on the tasks at hand, and ready to do what's needed and asked of you.

The good news is that this is not a journey you should do alone. Build a team you trust and be transparent with them. Ask questions, speak up when you're struggling, and don't be afraid to let others carry the load when you need a mental or physical break — or when your still-operating business requires your complete attention. Above all else, make sure you're working with an experienced healthcare M&A advisor — someone you trust and with whom you feel comfortable picking up the phone and talking through the process, including the emotional side of it.

Throughout it all, stay focused on the end goal. Remind yourself why you started this process in the first place. And most importantly, save some fuel for the finish line — because that's when you'll need it most.

David Purinton, MBA, CM&AA

After working in M+A advisory and corporate financial consulting, I was fortunate to co-found Spero Recovery, a provider of drug and alcohol recovery services with over 100 beds in its continuum of residential, outpatient, and sober living care. As its CFO I led the company to significant revenue and margin growth while ensuring it adhered to the strictest principles of integrity and client care. After selling Spero I remained in leadership with the buyer as its CFO and quickly realized accretion and integration. Of the myriad lessons not learned while earning my MBA with Distinction in Finance from a Tier 1 university, the most profound was the importance of investing in my staff and clients. I learned that the numbers on a spreadsheet represent humans, families, and dreams, which was a radically different paradigm from investment banking.

At VERTESS I am a Managing Director providing M+A and consulting services to the Behavioral Health, Substance Use Disorder treatment, and other verticals, where I bring a foundation of financial expertise with the value-add of humanness and care for the business owners I am honored to represent.

We can help you with more information on this and related topics. Contact us today!

There's the expression, "You never get a second chance to make a first impression." For many healthcare business owners thinking about selling their company, the first impression they may personally make on prospective buyers will come from a confidential information memorandum (CIM). If that CIM doesn't represent the business in a professional, positive, and transparent manner, the owner may not get a chance to receive a fair offer.

What exactly is a CIM? It's the confidential document used to market a healthcare business to potential buyers. It may go by other names, including a pitch deck, investor deck, the "book," or confidential information presentation (CIP). The marketing document is typically called a CIM when used in the sale of a mature healthcare businesses and a pitch deck for healthcare startups.

While the name is interchangeable, the content is not. A CIM is the initial source of data and information a buyer uses to evaluate the candidacy of an investment target relative to its investment thesis. Broadly speaking, the CIM explains what the business does and the type of transaction the owners are seeking.

Most business owners do not create a CIM until they are prepared to actively market their business for a sale. However, if an unsolicited buyer takes interest in your company, immediate signals are sent if you do not have a CIM, let alone one that's current: You're unprepared for a sale, and the buyer is in a good position to negotiate a value deal. At least those are the signals potential buyers receive, regardless of whether they're true. Simply responding to interested buyers with an annually updated CIM signals a posture toward prospective buyers that you are not interested in a low-ball offer.

On the other hand, if you intend to execute a coordinated, professional healthcare M&A process to sell your business, a CIM is required. You will be marketing your business to dozens — if not hundreds — of potential buyers, many of whom analyze numerous potential acquisitions each week. Without the data about your healthcare business consolidated in a professional manner, buyers are much less likely to invest the time into understanding your company's raw information. Note: Marketing your healthcare company is essential to finding the right buyer and securing a fair price for your business, which I previously discussed in this column.

Moreover, organizing and presenting the data allows you to structure the narrative in ways that emphasize your company's strengths while providing explanation on any potential weaknesses. You can tell your story to potential buyers in ways that benefit you as opposed to allowing a buyer to "discover" the hair — the operational, legal, financial, or other aspects of the business that have had errors, inefficiencies, or other liabilities — and speculating on any other skeletons that could be in your closet.

This column takes a closer look at the importance and development of a CIM is written for two audiences: 1) sellers who are hiring a professional healthcare M&A advisor, like VERTESS, to help them proceed with a sale and develop a supporting CIM or to double check that their current advisor included the relevant, key points in the CIM and 2) owners who endeavor to manage the sale of their business without a professional M&A advisor (not advisable) and therefore need tips and best practices to create an impactful CIM.

Confidential Information Memorandum Best Practices

Let's take a look at a few general CIM best practices before we discuss key components of a well-rounded CIM.

First, do not use a Word or similar document to create your CIM. Nobody wants to open up a CIM and be greeted by a wall of text — even a wall that has an occasional chart or image dropped in. Buyers review hundreds of CIMs, so the last thing you want to do is have a CIM that makes a negative first impression (remember what I said in the first paragraph). Make your CIM simple, nice to look at, and easy to review and digest. Include graphics, charts, and pictures, and present them in an attractive layout. This is best achieved using software like Microsoft PowerPoint.

Second, don't exaggerate or attempt to mislead a reader. An investor competent enough to buy your company is also competent enough to eventually learn the truth about your company. Be as honest as possible in the CIM. That's what buyers are expecting.

Third, and this goes back to the purpose of the CIM: Keep it concise. This means around 40 pages, although fewer is fine if that's what's required to effectively tell your story. If you feel compelled to create a CIM that's longer than 40 pages, you should feel that those "extra" pages are absolutely essential to better positioning your company in a competitive landscape.

After sending a CIM to potential buyers, you will find many will respond with additional questions deriving from their specific investment thesis. You can't try to get ahead of every question as questions change between differing theses. An industry specialist can help you create a CIM with specific data points that all investors in your vertical will want to understand. Investors will begin analyzing the data, using it in their own models; ask questions relating to their own thesis; and, if they feel like there could be an interesting opportunity, they will set up a "coffee meeting." This meeting gets final questions out of the way. When using a healthcare M&A advisor, the coffee meeting isn't something you should need to do as the seller.

From here, a potential buyer should have the preponderance of data needed to meet with you, the seller; identify chemistry and synergy; dig deeper into the data; visit your operations (if applicable); and eventually, if all goes well, submit a letter of intent (LOI).

What To Include in Your Healthcare Confidential Information Memorandum

Below we identify some of the core components of a good CIM. There may be reasons to exclude, modify, or expand on this list. Each business is different, and your M&A advisor should know what is most important to include in your CIM, assuming your advisor is a specialist in your healthcare industry.

Company overview

The first page of the CIM with meaningful content — usually the overview — gets a fair amount of attention and then most buyers will scroll to the financial section found later in the CIM. If buyers like both pages, they'll go back and read the rest of the document.

In your business overview, summarize the offering in a way any reader (potential buyer) can understand. Define your audience, which is often demographics of end users, the business types you sell to, and/or possibly a job function (i.e., your customers). Show how you solve a problem(s) and explain it in a way that's easy to follow.

The final element to include in your overview is your "secret sauce" — your unique approach to solving the problem with your target audience.

Some quick tips for writing the overview:

Avoid using adjectives like "first," "only," "huge," or "best," which are words that signal inexperience and possibly exaggeration.

Take time to properly define your target audience.

Eliminate buzzwords or jargon.

Keep it concise.

Include the ownership structure, reason(s) for the sale, and details on the desired deal structure, if known.

Company history

When you reflect on the history of your business, you'll probably think about the experience of opening the company, your first customer, the first time you hired and fired someone, your first insurance reimbursement check, a customer experience that went wrong, or a major accolade. Investors want to know about the background of your company, but they are really looking to understand your history through the lens of growth. Help buyers visualize the way your footprint expanded, customers grew, patients diversified, contracts were secured, and staff increased. Include the challenges and risk factors you faced along the way and how you overcame or navigated them.

Remember: A buyer is acquiring your business so they don't need to face all the challenges you encountered and overcame. If they wanted to face those challenges, they would start their own company. Let buyers know how much work it took to grow the company to its current state, even if those growth pains are in your distant memory.

After reading the history, potential buyers should come away with two sentiments: 1) I'm glad I don't have to go through all that effort, and 2) The skill, effort, and luck involved to advance the business to its current state are difficult to reproduce, so it's less risky to buy than build.

Team

Include an organization ("org") chart and explain why your team is qualified to execute your operations better than competitors. Work history, networks, and skills are key points to highlight, as is your history together as a team. This may include how you knew each other before working together.

Resume highlights or short bios are expected. Limit these to your leadership team. While the organization chart may show all the positions (ideally grouped by division or function), investors are most interested in and likely looking to acquire your management team. They want to know the management team that they're acquiring is worth their investment.

Healthcare market

In many healthcare verticals, the market is known or assumed, but potential buyers want to know how big the opportunity is associated with your company. Yes, they may plan to expand your business, but the core market is a starting point, and they want to know that you know it.

Beyond providing a market overview, also provide a clear picture of your audience. What is your market size? Who are they, and how many are in your market? How do you reach/communicate with your audience? What are your referral sources? What is your market position?

When putting together this market analysis, you may decide to share the "total addressable market" (TAM), which includes every potential member of your audience seeking services or products from your business, or you may decide to refine it to your "total serviceable market" (TSM), which are the customers you are able to reach.

Business model

How do you make money? Who pays you, how much, when, and from where? I've seen sellers drop the business model canvas into a pitch, but that may signal inexperience. You should be able to synthesize your business model into a succinct, visual, and possibly creative way where everyone can understand the model.

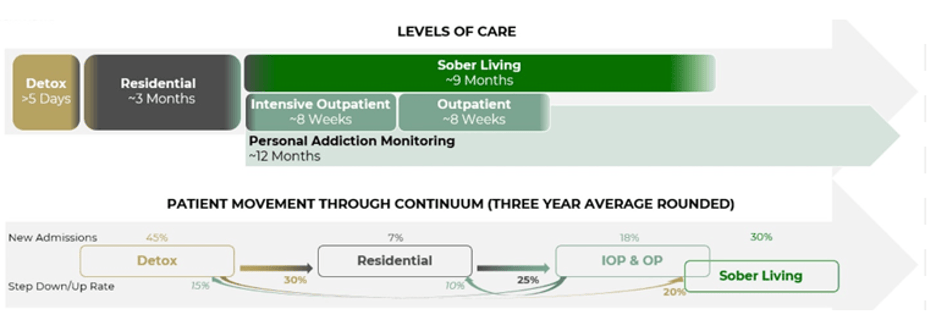

For example, with substance use disorder (SUD) providers, I model the American Society of Addiction Medicine (ASAM) continuum in a visual, then overlay the company's position in the continuum and add relevant data. See an example below. It's a simple visual to depict a client's business model, and even an investor not experienced in the space will understand exactly what the client does, how they're paid, how patients move around the continuum, and some outcome measurements.

Competition

Not all CIMs include information on competition, but I personally like to discuss it. In the SUD/mental health spaces, it's helpful to see the density of providers in a geography since that helps buyers understand in-network reimbursement rates better.

When providing a competitive analysis in the CIM, you do not need to know and/or identify every competitor, but you should have command over the competitors in proximity to your operations. Communicate how they're trying to address the problems you're working to solve and how your solution is similar or different — or whether any difference matters.

If you have a competitive advantage, share it. If your service is similar to your competitors, leave this section out. It may be unnecessary and spur questions you don't want to answer.

Business growth

Buyers deploy capital to generate a return on their investment. How might they generate a higher return on capital with your asset versus another? While you might not receive the "credit" in valuation for future revenues associated with growth (the buyer will need to do the work to achieve that growth, so they're not going to pay for it ahead of time and be accountable to execute it), you'll see increased interest from potential buyers if you can show demonstratable pathways to that growth.

Case studies that highlight a recent initiative and discuss how that initiative and its success can be reproduced is one effective way to demonstrate growth opportunities. In SUD, this may be a new level of care in an existing geography or starting an intensive outpatient program (IOP) to see if there's demand in a new geography before launching a residential treatment center (RTC). In mental health, a case study might speak to marketing to new populations, telehealth, psychedelics, or transcranial magnetic stimulation (TMS). Including data points that give a clear picture of the path toward growth can effectively demonstrate growth potential.

There are areas of low-hanging fruit for growth in most businesses. Even if they seem obvious, explain them. There are also growth initiatives you may have considered but chose not to pursue due to the effort, capital requirements, lack of manpower, lack of expertise, or simply because you were approaching a sale. Put numbers and timelines to these initiatives and offer the buyer a blueprint to a higher return on capital.

You're the expert. Help show it in the CIM. Buyers want to know what you might do to grow first before considering their own plans.

Financial overview

Historical and projected financials are key elements to a CIM. Explain volatility, and defend the proforma. Potential buyers will scrutinize any years where revenue and expense variance were substantial, so it helps to set the narrative for those likely questions in the CIM.

It's best that proformas provide a realistic outlook for the current scope and scale of the business if it is mature or a defensible and conservative outlook for growth initiatives for a newer business or startup. Sellers tend to have a bright outlook for future performance, but buyers know that storms can quickly appear in even the bluest of skies. In other words, your proforma should point "up and to the right" (it would be uncommon for an owner to believe plans will result in declining revenues) but avoid signaling inexperience by including assumptions that paint an unrealistic or overly optimistic growth trajectory.

Make sure the data you've peppered throughout your CIM clearly ties to and is reflected accurately in the proforma. We call this "tick and tie," where advisory teams put a "tick" mark next to every data point in a CIM and "tie" them out to all the other data to ensure everything checks out. If you don't tick and tie your CIM, there's a good chance a buyer will — and if they do, expect them to catch any errors, which will damage your credibility.

Metrics

Not all businesses operate off metrics, which is a travesty. If you have metrics, the key is to compare yours to industry norms. Common metrics in healthcare businesses include prior authorization versus claims collected, census, inventory turnover, and rounding, so you should be able to identify the benchmarks (a healthcare M&A advisor will help with this as well). If you have substantial variance from any benchmarks, you must address the reason(s) why. It's better to have an upfront explanation than to let buyers discover these variances and develop their own narrative for why your business is underperforming.

Creating An Optimal Healthcare Confidential Information Memorandum

Developing an informative and effective healthcare CIM takes time, expertise, comfort with software, and other skills. An experienced M&A advisor will have these skills or a team supporting them with such talents. An advisor will know how to present your company's most important data and what data to omit. An advisor will also know how to pepper the CIM with data points allowing buyside analysts to prepare their own models so they can analyze your business operating in their portfolio or model.

Completing a CIM is possible without an expert M&A advisor but doing so is not without risks. For most business owners, the work required to create a proper CIM is usually difficult to effectively execute while operating and leading the company and do so in a way that creates a limited auction for the company.

Since the CIM is essentially the first true experience, interaction, and impression a potential buyer will have with you and your company, it's likely in your best interests to hire a healthcare M&A advisor and task them with taking the lead on drafting the CIM. This will better help ensure the final document communicates what buyers want to see, positions your business correctly under current market conditions and buyer interests, and gives qualified buyers a starting point for the "coffee meetings."

David Purinton, MBA, CM&AA

After working in M+A advisory and corporate financial consulting, I was fortunate to co-found Spero Recovery, a provider of drug and alcohol recovery services with over 100 beds in its continuum of residential, outpatient, and sober living care. As its CFO I led the company to significant revenue and margin growth while ensuring it adhered to the strictest principles of integrity and client care. After selling Spero I remained in leadership with the buyer as its CFO and quickly realized accretion and integration. Of the myriad lessons not learned while earning my MBA with Distinction in Finance from a Tier 1 university, the most profound was the importance of investing in my staff and clients. I learned that the numbers on a spreadsheet represent humans, families, and dreams, which was a radically different paradigm from investment banking.

At VERTESS I am a Managing Director providing M+A and consulting services to the Behavioral Health, Substance Use Disorder treatment, and other verticals, where I bring a foundation of financial expertise with the value-add of humanness and care for the business owners I am honored to represent.

We can help you with more information on this and related topics. Contact us today!

If you own a healthcare company, you are probably receiving inquiries from interested buyers. We view this as buyers marketing themselves to you. At VERTESS, we emphasize the importance of clients marketing their company to buyers as a key step in securing the eventual right buyer and partner.

With potential buyers coming and marketing to you, why should you put in the time and effort to market to potential buyers?

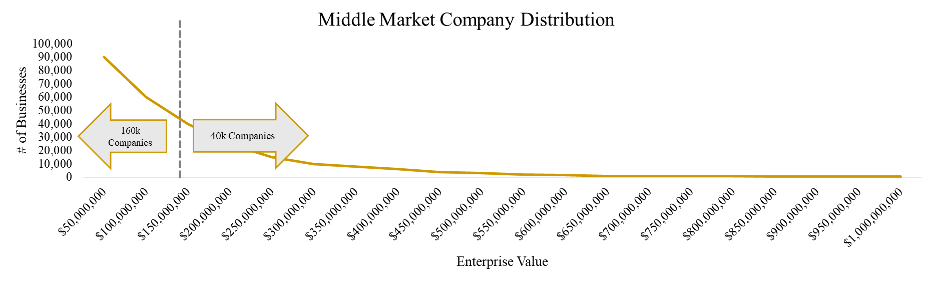

To answer this question, it's helpful to take a step back and understand the current market for sellers and buyers, specifically focusing on the lower middle market. This market has the vast majority of operating companies since most companies have under $150 million in enterprise value, as the following chart represents:

Given the volume of potential targets, there are more investors in the lower middle market than you can probably imagine. The role of these investors (i.e., buyers) is generally to acquire founder-owned companies, professionalize them, scale them organically and inorganically, integrate them, and then sell the larger entity to the next investor. The acquired company scales up as it passes through the hands of various investors.

These investors are financially motivated to market themselves as the appropriate buyer for your company. After all, they stand to make millions of dollars when their acquisition and subsequent growth and transaction strategies succeed. They're aggressively trying to find companies to buy and then execute these strategies.

Buyers view their outreach efforts as a sales cycle. They reach out to X number of business owners, hope that Y number of business owners will engage in discussions about selling their companies, and then the buyers weed out the companies they don't want to own, ultimately acquiring Z. In this sales cycle, buyers are essentially in control.

Owners who market to potential buyers take control of the sales cycle — one that's very similar to the cycle executed by buyers. Owners, usually supported by healthcare M+A advisors like those at VERTESS, reach out to X number of potential buyers and hope that Y number of buyers will engage in discussions about buying the company. Owners and their M+A advisors then weed out the buyers the owners don't want to sell to. The remaining options are engaged in discussions about the potential acquisition, ultimately concluding with the owner signing an agreement with Z.

The Value of Control

Putting the power on your side of the equation matters. Consider the following reasons:

More likely to find the right fit. There are several thousand healthcare investors. Not everyone is going to be a good fit for your company. In fact, most will not. Similarly, a random buyer is not likely to magically be the right fit for you. When you control who you market your company to, you are more likely to market toward companies perceived as potential good fits.

Investors will know you're ready to sell if you're marketing to them. This increases interest and reduces risk. When buyers find potential targets by marketing to companies, the investors usually do not know how willing a seller is to sign a contract. Given the costs of due diligence, that lack of knowledge presents a six- or seven-figure risk.

However, when an owner markets to buyers, investors feel more comfortable spending money in due diligence since they know the owner is more likely to sign the contract at the end of the process. The appearance of an owner interested in at least considering a sale attracts a greater number of investors.

Likelihood of better results. When you can identify multiple potential buyers who might be a good fit for your company, you put yourself in a position to leverage the interest in your asset to negotiate up valuation and terms. You cannot do this without leverage, as buyers aren't interested in spending more money to acquire your business unless they have competition — and competition perceived as legitimate and strong.

Tips for Buyers

While we understand the strategy, we respectfully ask that you stop showing premium valuations in your letters of intent (LOI) to unrepresented sellers. You may not see it as a bait-and-switch tactic, but that's exactly what the seller experiences, and they leave the process believing the initial offer is still achievable with someone else. Even if re-trading has worked for you in the past, this is the kind of tactic that makes sellers skeptical of any buyer.

If you're looking for off-market deals, be prepared for the time and effort required to achieve a discount. First and foremost, develop the relationship before discussing valuation. If the seller asks for an indication of value too soon, you probably know it's not going to the finish line. Cut bait and move on until you find a potential seller willing to spend time forming a relationship with you that can eventually be leveraged into a sale.

If you haven't already done so, create a pre-LOI request list and open a data room. You should have about 75% confidence in a deal before signing an LOI. Submit an LOI that you would submit to an M+A advisory firm like VERTESS. Start with a cash deal you're prepared to execute, then add structure if there's a valuation gap. It's difficult to re-trade down.

Meet With Me at TCIV

I'll be attending TCIV East in Palm Beach Gardens, Florida, from April 15–17. If you will be attending this conference and are interested in meeting up to discuss the topics covered in this column or any other issue concerning M+A, please reach out to me using my contact information below.

Here to Help

If you're an owner thinking about selling, contact the M+A team at VERTESS. We're specialized healthcare advisors who help our clients with exit planning and executing that plan, including marketing directly to those buyers likely to be a good fit for your company and serious about executing an acquisition. We'll help you determine the right path forward for the sale of your business and then do much of the heavy lifting that typically ends with a successful transaction.

David Purinton MBA, CM&AA

After working in M+A advisory and corporate financial consulting, I was fortunate to co-found Spero Recovery, a provider of drug and alcohol recovery services with over 100 beds in its continuum of residential, outpatient, and sober living care. As its CFO I led the company to significant revenue and margin growth while ensuring it adhered to the strictest principles of integrity and client care. After selling Spero I remained in leadership with the buyer as its CFO and quickly realized accretion and integration. Of the myriad lessons not learned while earning my MBA with Distinction in Finance from a Tier 1 university, the most profound was the importance of investing in my staff and clients. I learned that the numbers on a spreadsheet represent humans, families, and dreams, which was a radically different paradigm from investment banking.

At VERTESS I am a Managing Director providing M+A and consulting services to the Behavioral Health, Substance Use Disorder treatment, and other verticals, where I bring a foundation of financial expertise with the value-add of humanness and care for the business owners I am honored to represent.

We can help you with more information on this and related topics. Contact us today!

There's the expression, "You never get a second chance to make a first impression." For many healthcare business owners thinking about selling their company, the first impression they may personally make on prospective buyers will come from a confidential information memorandum (CIM). And if that CIM doesn't represent the business in a professional, positive, and transparent manner, the owner may not get a chance to receive a fair offer.

What exactly is a CIM? It's the document used to market your business to potential buyers. It may go by other names, including a pitch deck, investor deck, the "book," or confidential information presentation (CIP). The document is typically called a CIM when used in the sale of a mature business and a pitch deck for startups.

While the name is interchangeable, the content is not. A CIM is the initial source of data and information a buyer uses to evaluate the candidacy of an investment target relative to its investment thesis. Broadly speaking, the CIM explains what the business does and the type of transaction the owners are seeking.

Most business owners do not create a CIM until they are prepared to actively market their business for a sale. However, if an unsolicited buyer takes interest in your company, immediate signals are sent if you do not have a CIM, let alone one that's current: You're unprepared for a sale, and the buyer is in a good position to negotiate a value deal. At least those are the signals buyers receive, regardless of whether they're true. Simply responding to interested buyers with an annually updated CIM signals a posture toward prospective buyers that you are not interested in a low-ball offer.

On the other hand, if you intend to execute a coordinated, professional M+A process to sell your business, a CIM is required. You will be marketing your business to dozens — if not hundreds — of potential buyers, many of whom analyze numerous potential acquisitions each week. Without the data about your healthcare business consolidated in a professional manner, buyers are much less likely to invest the time into understanding your company's raw data.

Moreover, organizing and presenting the data allows you to structure the narrative in ways that emphasize your company's strengths while providing explanation on potential weaknesses. You can tell your story in ways that benefit you as opposed to allowing a buyer to "discover" the hair — the operational, legal, financial, or other aspects of the business that have had errors, inefficiencies, or other liabilities — and speculating on any other skeletons.

This article taking a closer look at the importance and development of a CIM is written for two audiences: 1) sellers who are hiring a professional M+A advisor, like VERTESS, to help them proceed with a sale and develop a supporting CIM or to double check that their current advisor included the relevant, key points in the CIM and 2) owners who endeavor to manage the sale of their business without a professional M+A advisor (not advisable) and therefore need tips and best practices to create an impactful CIM.

CIM Best Practices

Let's take a look at a few general CIM best practices before we discuss key components in a well-rounded CIM.

First, do not use a Word document to create your CIM. Nobody wants to open up a CIM and be greeted by a wall of text — even a wall that has an occasional chart or image dropped in. Buyers review hundreds of CIMs, so the last thing you want to do is have a CIM that makes a negative first impression (remember what I said in the first paragraph). Make your CIM simple, nice to look at, and easy to review and digest. Include graphics, charts, and pictures and present them in an attractive layout. This is best achieved using software like PowerPoint.

Second, don't exaggerate or attempt to mislead a reader. An investor competent enough to buy your company is also competent enough to learn the truth about your company. Be as honest as possible in the CIM. That's what buyers are expecting.

Third, and this goes back to the purpose of the CIM: Keep it concise. This means around 40 pages, although fewer is fine if that's what's required to effectively tell your story.

After sending a CIM to potential buyers, you will find many will respond with additional questions deriving from their specific investment thesis. You can't try to get ahead of every question as questions change between differing theses. An industry specialist can help you create a CIM with specific data points that all investors in your vertical will want to understand. Investors will begin analyzing the data, using it in their own models; ask questions relating to their own thesis; and, if they feel like there could be an interesting opportunity, they will set up a "coffee meeting." This meeting gets final questions out of the way. When using an M+A advisor, the coffee meeting isn't something you should need to do as the seller.

From here, the buyer should have the preponderance of data needed to meet with you, the seller; identify chemistry and synergy; dig deeper into the data; visit your operations; and eventually, if all goes well, submit a letter of intent (LOI).

What To Include in Your CIM

Below we identify some of the core components of a good CIM. There may be reasons to exclude, modify, or expand on this list. Each business is different, and your M+A advisor should know what is most important to include in your CIM, assuming your advisor is a specialist in your industry.

Overview. The first page of the CIM with meaningful content — usually the overview — gets a fair amount of attention and then most buyers will scroll to the financial section found later in the CIM. If buyers like both pages, they'll go back and read the rest of the document.

In your overview, summarize the offering in a way any reader (buyer) can understand. Define your audience, which is often demographics of end users, the business types you sell to, or possibly a job function (i.e., your customers). Show how you solve a problem(s) and explain it in a way that's easy to follow.

The final element to include in your overview is your "secret sauce" — your unique approach to solving the problem with your target audience.

Some quick tips for writing the overview:

Avoid using adjectives like "first," "only," "huge," or "best," which are words that signal inexperience and possibly exaggeration.

Take time to properly define your target audience.

Eliminate buzzwords or jargon.

Keep it short.

Include the ownership structure and reason(s) for the sale.

History. When you reflect on the history of your business, you'll probably think about the experience of opening the company, your first customer, the first time you hired and fired someone, your first insurance reimbursement check, a customer experience that went wrong, or a major accolade. Investors want to know about the background of your company, but they are really looking to understand your history through the lens of growth. Help buyers visualize the way your footprint expanded, customers grew, patients diversified, contracts were secured, and staff increased. Include the challenges you faced along the way and how you overcame or navigated them.

Remember: A buyer is acquiring your business so they don't need to face all the challenges you did. If they wanted to face those challenges, they would start their own company. Let buyers know how much work it took to grow the company to its current state, even if those growth pains are in your distant memory.

After reading the history, buyers should come away with two sentiments: 1) I'm glad I don't have to go through all that effort, and 2) The skill, effort, and luck involved to advance the business to its current state are difficult to reproduce, so it's less risky to buy than build.

Team. Include an organization ("org") chart and explain why your team is qualified to execute your operations better than competitors. Work history, networks, and skills are key points to highlight, as is your history together as a team. This may include how you knew each other before working together.

Resume highlights or short bios are expected. Limit these to leadership. While the organization chart may show all the positions (ideally grouped by division or function), investors are most interested in and likely looking to acquire your leadership team and want to know they're of pedigree.

Market. In many healthcare verticals, this is known or assumed, but buyers want to know how big the opportunity is associated with your company. Yes, they may plan to expand your business. But the core market is a starting point, and they want to know that you know it.

Beyond the market, also provide a clear picture of your audience. Who are they, and how many are in your market? How do you reach/communicate with them? What are your referral sources?

You may decide to share the "total addressable market" (TAM), which includes every potential member of your audience seeking services or products from your business, or you may decide to refine it to your "total serviceable market" (TSM), which are the customers you are actually able to reach.

Business model. How do you make money? Who pays you, how much, when, and from where? I've seen sellers drop the business model canvass into a pitch, but that may signal inexperience. You should be able to synthesize your business model into a succinct, visual, and possibly creative way where everyone can understand the model.

For example, with substance use disorder (SUD) providers, I model the American Society of Addiction Medicine (ASAM) continuum in a visual, then overlay the company's position in the continuum and add relevant data. See an example below. It's a simple visual to depict a client's business model, and even an investor not experienced in the space will understand exactly what the client does, how they're paid, how patients move around the continuum, and some outcome measurements.

Competition. Not all CIMs include information on competition, but I personally like to discuss it. In the SUD/mental health spaces, it's helpful to see the density of providers in a geography since that helps buyers understand in-network reimbursement rates better.

When discussing your competition in the CIM, you do not need to know and identify every competitor, but you should have command over the competitors in proximity to your operations. Communicate how they're trying to address the problems you're trying to address and how your solution is similar, different, or whether that matters.

If you have a competitive advantage, share it. If your service is similar to your competitors, leave this section out. It may be unnecessary and spur questions you don't want to discuss.

Growth. Buyers deploy capital to generate a return on their investment. How might they generate a higher return on capital with your asset versus another? While you might not receive the "credit" in valuation for future revenues associated with growth (the buyer will need to do the work to achieve that growth, so they're not going to pay for it ahead of time and be accountable to execute it), you'll see increased interest from buyers if you can show demonstratable pathways to that growth.

Case studies that highlight a recent initiative and discuss how that initiative and its success can be reproduced is one effective way to demonstrate growth opportunities. In SUD, this may be a new level of care in an existing geography or starting an intensive outpatient program (IOP) to see if there's demand in a new geography before launching a residential treatment center (RTC). In mental health, a case study might speak to marketing to new populations, telehealth, psychedelics, or transcranial magnetic stimulation (TMS). Including data points that give a clear picture to the path toward growth can also be effective at demonstrating growth potential.

There are areas of low-hanging fruit for growth in most businesses. Even if they seem obvious, explain them. There are also growth initiatives you may have considered but chose not to pursue due to the effort, capital requirements, lack of manpower, lack of expertise, or simply because you were approaching a sale. Put numbers and timelines to these initiatives and offer the buyer a blueprint to a higher return on capital.

You're the expert. Help show it in the CIM. Buyers want to know what you might do to grow first before considering their own plans.

Financial overview. Historical and projected financials are key elements to a CIM. Explain volatility and defend the proforma. Buyers will scrutinize any years where revenue and expense variance were substantial, so it helps to set the narrative for those likely questions in the CIM.

It's best that proformas provide a realistic outlook for the current scope and scale of the business if it is mature or a defensible and conservative outlook for growth initiatives for a newer business or startup. Sellers tend to have a bright outlook for future performance, but buyers know that storms can quickly appear in even the bluest of skies. In other words, your proforma should point "up and to the right" (it would be uncommon for an owner to believe plans will result in declining revenues) but avoid signaling inexperience by including assumptions that paint an unrealistic or overly optimistic growth trajectory.

Make sure the data you've peppered throughout your CIM clearly ties to and is reflected accurately in the proforma. We call this "tick and tie," where advisory teams put a "tick" mark next to every data point in a CIM and "tie" them out to all the other data to ensure everything checks out. If you don't tick and tie your CIM, there's a good chance a buyer will. If they do, expect them to catch any errors, which will damage your credibility.

Metrics. Not all businesses operate off metrics, which is a travesty. I'll write a future article on how to develop metrics for your company and why that matters in an M+A transaction. If you do have metrics, the key is to compare yours to industry norms. Common metrics in healthcare businesses include prior authorization vs. claims collected, census, inventory turnover, and rounding, so you should be able to identify the benchmarks (an M+A advisor will help with this as well). If you have substantial variance from the benchmarks, you must address the reason(s) why. It's better to have an upfront explanation than to let buyers discover these variances and develop their own narrative for why your business is underperforming.

Creating An Optimal Confidential Information Memorandum

Developing an informative and effective CIM takes time, expertise, comfort with software, and other skills. An experienced M+A advisor will have these skills or a team supporting them with such talents. An advisor will know how to present your company's most important data and what data to omit. An advisor will also know how to pepper the CIM with data points allowing buyside analysts to prepare their own models so they can analyze your business operating in their portfolio or model.

Completing a CIM is possible without an expert advisor, but not without risks. For most business owners, the work required to create a proper CIM is usually difficult to effectively execute while operating and leading the company and do so in a way that creates a limited auction for the company.

Since the CIM is essentially the first true experience and interaction (and impression) a buyer will have with you and your company, it's likely in your best interests to hire an M+A advisor and task them with taking the lead on the CIM. This will better help ensure the final document communicates what buyers want to see, positions your business correctly under current market conditions and buyer interests, and gives buyers a starting point for the "coffee meetings."

Volume 8, Issue 15, October 5, 2021

I recently joined VERTESS as a managing director. I'll be providing merger and acquisition (M+A) and consulting services primarily to the behavioral health and substance use disorder (SUD) treatment markets. Like many of my new colleagues, I previously owned and operated a company in the space I will be working in for VERTESS. But that's not all: I also have firsthand, personal experience with substance misuse.

In this column, I'll share a little about this journey with you, how it motivated me to open my company, and several of the key lessons I learned from the sales process.

Personal Background

After years of failed attempts to stop drinking — and my own bias toward Alcoholics Anonymous, which kept me out of the rooms during those years — my family held an intervention for me in 2009. This resulted in a plane ride to Denver and a visit to a residential treatment program. I knew nothing of what the experience would be like but quickly realized that I was going to be in a one-year, behavioral modification program.

During that year, I never met with a therapist or generated the recovery capital that would be necessary to support me in the difficult years ahead following treatment. After completing the program, I found out that my family could not find a clinical treatment facility that would cost them less than $30,000 for a single month of care. They did the best they could without an understanding of the SUD treatment industry, insurance requirements, and admissions criteria. They sent me to a low-cost behavioral modification program because they could not afford a clinical program but needed to help me get into a safe place.

The Accessibility Challenge

After my experience, I became somewhat obsessed with accessible treatment and began consulting with residential programs a few years later. As a proponent of the parity initiatives discussed on Capitol Hill, I was disappointed when the passage of the Affordable Care Act ignited a series of lawsuits against providers who fraudulently manipulated insurance reimbursements to line their own pockets.

Furthering my disappointment in the industry was the lack of appropriations to states’ Medicaid budgets for inpatient and residential reimbursements. In Colorado, where I was living, Medicaid appropriations dried up for inpatient and residential care after the closure of the largest facility in Colorado, which mismanaged finances and operations to the point of insolvency.

Accessible care has advanced substantially over the past several years but still faces significant headwinds. In 2019, legislatures said that there should be enough beds in the country to support the demand for clinical treatment. However, there were not sufficient affordable and “attractive” beds. Those beds offered at an accessible price point were often behavioral modification or homeless-oriented programs, which all but those in dire need will not likely access. Without affordable and attractive options, people are less likely to get the support they need and more likely to continue using their substance(s) of choice.

Co-Founding Spero Recovery

Along with a treatment veteran and clinician, I started Spero Recovery with the intention of providing residential drug and alcohol care at a fraction of the national average cost. I wanted to create the type of environment I would have wanted to find back in 2009 and at a price point I could have afforded. My co-founders drew up programming plans and systems and began marketing the new program to other providers. Meanwhile, I secured real estate, funding, developed the IT systems, and managed financial operations. Before our intended opening, we had so many people calling us for admissions that we decided to move our opening date up by two months.

One difficultly of providing SUD treatment is the fixed costs of staffing. You must invest ahead of the curve, knowing you are spending significant capital that will not be returned until you can maintain a decent census. About three months after opening, I began analyzing burn rates almost nightly in fear that we were not capitalized sufficiently to last through the period of cash flow losses. But we survived our first year of operations, improved the program, and positioned ourselves for growth.

Around the time we were finding traction, COVID-19 precautions resulted in shelter-in-place orders. Not knowing what would result, we thought we would lose our program before we even had the chance to scale it. We were wrong. With job losses and substance misuse rates increasing from the pandemic, more people than ever were seeking treatment and required financially accessible care if they did not have COBRA insurance coverage. In fact, we remained at 100% occupancy with a paid waitlist since the onset of the pandemic in March 2020. Leadership can take a toll on someone who isn’t prepared to wear a target from disgruntled employees and skeptical onlookers, deal with sleepless nights, and work most weekends. One co-founder required a leave of absence to recover from the stress of scaling a business from $0 to more than $2.5 million in annual revenue in only two years. The other co-founder was only involved in operations part-time, leaving me to lead the entire organization without their support. I decided to sell Spero Recovery to an organization that had sufficient senior leadership to continue scaling it into a national program, but I made a mistake along the way: I first sold it to a tangential organization with unaligned cultures and values. As the interim CFO of the buying company, I decided to divest Spero Recovery to an independent sponsor who was well-known in the industry for practicing the principles of recovery in all his affairs. He was the right fit to scale Spero Recovery to a national program.

Lessons Learned From the Sale

If I had to do it all over, I would have built the organization much differently and transacted it differently as well. I learned the following five invaluable lessons in the sale process that may be relevant to other sellers.

Lesson 1: Culture Eats Strategy for Lunch

The idiom is so cliché that it has become white noise but remember that a cliché has a lot of truth in it. Prior to co-founding Spero Recovery, I was an M+A advisor at an investment bank, equipped with an MBA and a head full of financial knowledge. But I lacked wisdom. I had never seen what post-merger integration looked like or checked to see if employees were happy following the acquisition. Turns out, oftentimes accretion does not occur because integrating cultures poses too significant a challenge. Spero Recovery was fortunate to have a CEO who was more interested in the mission than his own personal return, but most companies do not enjoy that kind of relationship with an owner.

Lesson 2: Hire an Advisor

I had several years of M+A experience before Spero Recovery, so I thought I would be able to handle the transaction without hiring an outsourced advisor. The problem wasn’t my lack of knowledge, motivation, or negotiating skills. Rather, it was that Spero Recovery was my baby. At times during the sale process, I was too emotionally connected to the deal to make the most rational decisions. When I processed decisions and conversations with my colleagues, I noticed significant bias from them as well. Furthermore, I was also managing the organization while running the M+A process and was unable to respond as quickly to targets, nor was I able to give sufficient attention to Spero Recovery. It was less about a lack of skill and more about bandwidth and emotions.

Lesson 3: Dig In Your Heels

This was an area where I succeeded. There were certain deal points on which I would not compromise; others were not mandatory. Knowing that most sales processes will result in negotiations, I needed to hold my ground from the start on certain issues.

Lesson 4: Don’t Pick the Fruit Before It’s Ripe

Spero Recovery has tranches of fixed expenses that grow with scale but, like many residential treatment organizations, has significant economies of scale. The company was on the precipice of entering a new tranche of scale and would have experienced accretion from the associated investments within a year. I knew I was picking the fruit before it was fully ripe (selling before it could yield a higher valuation) and left enterprise value on the table by selling when I did. I had reasons to transfer it to the buyer of choice, but I have often questioned the decision to sell the business a year early.

Lesson 5: Celebrate

Part of celebrating the sale was handing a check to each of my employees after it was consummated. Sharing the celebration with my team was the highlight of the entire transaction process.

Here to Help

If you're ready to sell your company or contemplating a sale down the road, I'd welcome the opportunity to speak with you. As I learned from my experience with Spero Recovery, working with an advisor, whether it's VERTESS or another qualified healthcare M+A advisory firm, is one of the best decisions you can make for your business. If you're not doing everything you can to prepare for and execute a sale, you're doing yourself, your company, your staff, and your clients a disserve and almost certainly leaving value on the table.

Volume 7 Issue 5, March 3, 2020

By David Coit, DBA, CVA, CVGA, CM&AA and Hilsman Knight, CM&AA

The healthcare

industry is continually in flux. Business owners and operators of urgent care

centers (UCCs) are constantly experiencing changing regulatory guidelines and

suppressing reimbursement from payors. These unpreventable changes and a demanding

environment may lead owners to seek monetization of their assets. For those UCC

owners considering selling, there's good news: The marketplace is currently hungry

for your companies and buyers are eagerly gobbling up well-performing UCCs.

Owners of a UCC have the advantage of running businesses that are relied upon by other companies in the healthcare sector. Buyers see the advantage of owning and operating multiple locations and leveraging their current relationships to further extract value. As such, this is an excellent time to sell if you're looking to receive a premium price.

Recent Market Developments

Over the past

several years, UCCs have rapidly emerged as an efficient way for patients to access

specific healthcare needs. This has caused their popularity to grow, with centers

emerging across the country in urban and rural areas. Furthermore, UCCs with multiple

locations have developed synergistic value with other regional emergency

healthcare providers. This has created a spoke-and-wheel-like model to help

manage the continuum of care. Patients with minor, non-emergency services are taken

care of quickly in UCCs, while more severe cases can be transferred out to

freestanding emergency rooms (ERs), micro hospitals, and hospital emergency

departments. In a relatively short amount of time, UCCs made themselves an integral

part of the healthcare system.

Moreover, during

the past five years, a shortage of primary care physicians (PCPs) coupled with

rising costs and ER wait times stimulated even greater demand for UCCs to

provide noncritical care. As such, the UCC industry has enjoyed 6.1% annual

growth over this period, according to IBISWorld.

Industry at a Glance

There are about 4,700 UCCs in the United States. They generate combined annual revenues of $27.8 billion and profits of $5.7 billion. Referrals to UCCs come from hospitals, PCPs, orthopedic surgery providers, and otolaryngology (ENT) physicians, among others. A UCC's average payor mix is approximately 55% private insurance, 17% Medicare, 10% out-of-pocket payments, 5% Medicaid, 5% workers' compensation, 4% other government, and 4% other. The 10 largest UCC chains only own 10% of the total number of UCCs. As such, the industry remains highly fragmented.

Industry Outlook

The industry will continue growing

over the next several years as a result of:

The continued shortage of PCPs

Aging population

The rising number of insured individuals

Greater acceptance of non-hospital urgent care by consumers

Increasing wait times at ERs and with PCPs

Cost-containment measures

Continued expansion of UCC service lines beyond illness and injury treatments that now include vaccinations, blood tests, lab tests, digital X-rays, and annual physicals

Overall, revenue is expected to grow an annualized 2.5% over

the next 4-5 years to reach $31.4 billion in combined annual revenues.

Market Factors to Consider

If you're

thinking of selling your UCC, you should know the following:

The

market is strong now because of the vast amount of money/capital searching for

well-performing UCCs. It's unclear how long this will last and when it will (inevitably)

slow down. The market can change quickly, and you may lose your opportunity to

sell at a favorable price.

As

acquisitions and consolidations continue, you'll likely be competing against

larger, better-capitalized companies. The competitive landscape is changing. Larger

competitors are likely to offer a broad range of medical services, a strong

marketing campaign built around an established brand, and efficient business

processes.

Owners

of UCCs are aging. One estimate is that 60% of UCCs owners are over the age of

55. As such, we expect an increasing number of UCCs seeking buyers in the

market during the next few years.

Buyers' Concerns

Smart buyers

weigh risks versus rewards when considering the purchase of a company. Some of

the perceived risks in the UCC industry are as follows:

Rapid

expansion in the number of UCCs due to low barriers of entry

Escalating

enforcement of Stark and anti-kickback laws

Non-traditional

firms entering retail healthcare

Shortage

of skilled healthcare professionals to fill UCC clinical positions

Buyers' Rewards

Buyers are

looking for rewards or upsides from their purchase of UCCs. Much of the upside

will come from industry market conditions, such as:

Expanded

Medicaid coverage

Increasing

client demand for UCC services that will drive strong annual growth

Average

number of annual visits per patient greater than PCPs and hospital visits

Client

services demand unrelated to economic cycles

Highly

fragmented and cottage industry

What Buyers Are Looking For

In our

experience, the most important feature buyers are looking for when pursuing

UCCs is profitable growth. Buyers want to know that they can take what you have

created and build on it. In their risk/reward analysis, buyers want to see that

your strengths far outweigh your weaknesses. Most buyers have a checklist mentality,

where they'll be looking to see that you have at least some of the following attributes:

Geographical

proximity to underserved healthcare areas

Multiple

service delivery locations and regional density

Solid

in-network relations with payors, and with long-term payor contracts

Multiple

treatment/service options

30-plus

patient visits per day, per location

Strong,

diverse physician and non-physician referral network

Diversified

payor mix

Low

uncollectable accounts receivables

Low

revenue seasonality

Certificate

of Need (CON) for CON states

Tenured,

experienced workforce with low employee turnover

Well-preforming

revenue cycle

Good

revenue growth at or above the industry average, and positive growth outlook

Earnings

before interest, taxes, depreciation, and amortization (EBITDA) margins in the

10%-20% range

How Much Will Buyers Pay (Market Multiples)?

Buyers

typically go through their risk/reward analysis and come up with an offering

purchase price. The offering price is usually based on a multiple of normalized

or adjusted EBITDA.

EBITDA

adjustments include non-recurring expenses, such as one-time legal fees;

discretionary expenses, such as charitable contributions; and owner-related

personal expenses, such as excess owners' salaries and auto leases.

Market

multiples refer to the estimated purchase price relative to EBITDA. The typical

range of market multiples for small- and medium-sized UCCs is 3.5x-8.5x EBITDA,

while large-sized UCCs may see 9.0x-12.0x multiples. Where a particular

provider falls within the range is based on quantitative factors, such as historical

and projected financial performance, and qualitative factors as highlighted

above in the "What Buyers Are Looking For" section. Moreover, size

matters, as larger revenue UCCs tend to attract more buyers than smaller

providers.

The

following are estimated market multiples for UCCs by revenue, assuming positive

qualities related to the "What Buyers Are Looking For" section above:

<

$1 million in annual revenue: 3.5x-4.0x EBITDA

$1

million to $3 million in annual revenue: 4.0x-5.0x EBITDA

$3

million to $5 million in annual revenue: 4.5x-6.0x EBITDA

$5

million to $20 million in annual revenue: 5.5x-8.5x EBITDA

>

$20 million in annual revenue: 7.5x-10.0x EBITDA

Note that there

are outlier market multiples in unique merger and acquisition transactions

where optimal buyer/seller synergies push valuations above the norm. Moreover,

market multiples change over time depending on the overall economy, regulatory

and reimbursement modifications, and industry trends.

Using market multiples is a good way to estimate the value of a company. It is most often accompanied by the use of a discounted cash flow approach. The discounted cash flow approach estimates the value of a company by calculating the future cash flows expected from the company and putting the future cash flows into today's dollars. However, the market multiples approach provides a reasonable shortcut for estimating the value of a company.

What About My Company's Debt?

The market multiples above are used to determine the equity value of companies, not the enterprise value. Most small businesses are sold debt-free, which means buyers assume that all of the company's debts (not to be confused with non-debt current liabilities) will be paid off by the seller at the time of closing. There are occasions, however, where a buyer wishes to assume the debt of the company as a way to finance part of the purchase price.

About VERTESS

VERTESS is the

advisor of choice for many UCC business owners because of our track record of

success and deep industry expertise. You should be speaking with an advisor at

least annually to understand the market and your options.

VERTESS was formed by a visionary group of results-oriented professionals as an alternative to traditional merger and acquisition firms and investment banks. We focus primarily on your personal and professional goals, and we help facilitate transactions that make sense to you for the long term. Every owner of every company has different motivating factors for why they want to sell. Some owners decide to sell for liquidity purposes, especially when most of their net worth is tied up in their company, while others sell because they are increasingly concerned about the future viability of their company. Another reason owners might decide to sell is they feel it's time for a change, so they seek outside partnerships with investors and industry experts. All reasons have their own validity, and VERTESS takes them into consideration. We guarantee integrity, confidentiality, and a commitment to the best outcome for you, your company, and your family.

COMMITTED TO CONSTANT IMPROVEMENT?

Want to stay current with trends in the medical/healthcare space as well as receive expert advice of veteran medical entrepreneurs?

SUBSCRIBE TO OUR BI-WEEKLY NEWSLETTER VERTESSPRESS

For over 10 years, we've been teaching ways you can improve the value of your healthcare company, focusing on informing you about mergers + acquisitions, including M+A trends in the healthcare market.