What Is a Confidential Information Memorandum (CIM) in Healthcare M&A?

Published September 24th 2024

Volume 11, Issue 18, September 24, 2024

By: David Purinton, MBA, CM&AA

There's the expression, "You never get a second chance to make a first impression." For many healthcare business owners thinking about selling their company, the first impression they may personally make on prospective buyers will come from a confidential information memorandum (CIM). If that CIM doesn't represent the business in a professional, positive, and transparent manner, the owner may not get a chance to receive a fair offer.

What exactly is a CIM? It's the confidential document used to market a healthcare business to potential buyers. It may go by other names, including a pitch deck, investor deck, the "book," or confidential information presentation (CIP). The marketing document is typically called a CIM when used in the sale of a mature healthcare businesses and a pitch deck for healthcare startups.

While the name is interchangeable, the content is not. A CIM is the initial source of data and information a buyer uses to evaluate the candidacy of an investment target relative to its investment thesis. Broadly speaking, the CIM explains what the business does and the type of transaction the owners are seeking.

Most business owners do not create a CIM until they are prepared to actively market their business for a sale. However, if an unsolicited buyer takes interest in your company, immediate signals are sent if you do not have a CIM, let alone one that's current: You're unprepared for a sale, and the buyer is in a good position to negotiate a value deal. At least those are the signals potential buyers receive, regardless of whether they're true. Simply responding to interested buyers with an annually updated CIM signals a posture toward prospective buyers that you are not interested in a low-ball offer.

On the other hand, if you intend to execute a coordinated, professional healthcare M&A process to sell your business, a CIM is required. You will be marketing your business to dozens — if not hundreds — of potential buyers, many of whom analyze numerous potential acquisitions each week. Without the data about your healthcare business consolidated in a professional manner, buyers are much less likely to invest the time into understanding your company's raw information. Note: Marketing your healthcare company is essential to finding the right buyer and securing a fair price for your business, which I previously discussed in this column.

Moreover, organizing and presenting the data allows you to structure the narrative in ways that emphasize your company's strengths while providing explanation on any potential weaknesses. You can tell your story to potential buyers in ways that benefit you as opposed to allowing a buyer to "discover" the hair — the operational, legal, financial, or other aspects of the business that have had errors, inefficiencies, or other liabilities — and speculating on any other skeletons that could be in your closet.

This column takes a closer look at the importance and development of a CIM is written for two audiences: 1) sellers who are hiring a professional healthcare M&A advisor, like VERTESS, to help them proceed with a sale and develop a supporting CIM or to double check that their current advisor included the relevant, key points in the CIM and 2) owners who endeavor to manage the sale of their business without a professional M&A advisor (not advisable) and therefore need tips and best practices to create an impactful CIM.

Confidential Information Memorandum Best Practices

Let's take a look at a few general CIM best practices before we discuss key components of a well-rounded CIM.

First, do not use a Word or similar document to create your CIM. Nobody wants to open up a CIM and be greeted by a wall of text — even a wall that has an occasional chart or image dropped in. Buyers review hundreds of CIMs, so the last thing you want to do is have a CIM that makes a negative first impression (remember what I said in the first paragraph). Make your CIM simple, nice to look at, and easy to review and digest. Include graphics, charts, and pictures, and present them in an attractive layout. This is best achieved using software like Microsoft PowerPoint.

Second, don't exaggerate or attempt to mislead a reader. An investor competent enough to buy your company is also competent enough to eventually learn the truth about your company. Be as honest as possible in the CIM. That's what buyers are expecting.

Third, and this goes back to the purpose of the CIM: Keep it concise. This means around 40 pages, although fewer is fine if that's what's required to effectively tell your story. If you feel compelled to create a CIM that's longer than 40 pages, you should feel that those "extra" pages are absolutely essential to better positioning your company in a competitive landscape.

After sending a CIM to potential buyers, you will find many will respond with additional questions deriving from their specific investment thesis. You can't try to get ahead of every question as questions change between differing theses. An industry specialist can help you create a CIM with specific data points that all investors in your vertical will want to understand. Investors will begin analyzing the data, using it in their own models; ask questions relating to their own thesis; and, if they feel like there could be an interesting opportunity, they will set up a "coffee meeting." This meeting gets final questions out of the way. When using a healthcare M&A advisor, the coffee meeting isn't something you should need to do as the seller.

From here, a potential buyer should have the preponderance of data needed to meet with you, the seller; identify chemistry and synergy; dig deeper into the data; visit your operations (if applicable); and eventually, if all goes well, submit a letter of intent (LOI).

What To Include in Your Healthcare Confidential Information Memorandum

Below we identify some of the core components of a good CIM. There may be reasons to exclude, modify, or expand on this list. Each business is different, and your M&A advisor should know what is most important to include in your CIM, assuming your advisor is a specialist in your healthcare industry.

Company overview

The first page of the CIM with meaningful content — usually the overview — gets a fair amount of attention and then most buyers will scroll to the financial section found later in the CIM. If buyers like both pages, they'll go back and read the rest of the document.

In your business overview, summarize the offering in a way any reader (potential buyer) can understand. Define your audience, which is often demographics of end users, the business types you sell to, and/or possibly a job function (i.e., your customers). Show how you solve a problem(s) and explain it in a way that's easy to follow.

The final element to include in your overview is your "secret sauce" — your unique approach to solving the problem with your target audience.

Some quick tips for writing the overview:

Avoid using adjectives like "first," "only," "huge," or "best," which are words that signal inexperience and possibly exaggeration.

Take time to properly define your target audience.

Eliminate buzzwords or jargon.

Keep it concise.

Include the ownership structure, reason(s) for the sale, and details on the desired deal structure, if known.

Company history

When you reflect on the history of your business, you'll probably think about the experience of opening the company, your first customer, the first time you hired and fired someone, your first insurance reimbursement check, a customer experience that went wrong, or a major accolade. Investors want to know about the background of your company, but they are really looking to understand your history through the lens of growth. Help buyers visualize the way your footprint expanded, customers grew, patients diversified, contracts were secured, and staff increased. Include the challenges and risk factors you faced along the way and how you overcame or navigated them.

Remember: A buyer is acquiring your business so they don't need to face all the challenges you encountered and overcame. If they wanted to face those challenges, they would start their own company. Let buyers know how much work it took to grow the company to its current state, even if those growth pains are in your distant memory.

After reading the history, potential buyers should come away with two sentiments: 1) I'm glad I don't have to go through all that effort, and 2) The skill, effort, and luck involved to advance the business to its current state are difficult to reproduce, so it's less risky to buy than build.

Team

Include an organization ("org") chart and explain why your team is qualified to execute your operations better than competitors. Work history, networks, and skills are key points to highlight, as is your history together as a team. This may include how you knew each other before working together.

Resume highlights or short bios are expected. Limit these to your leadership team. While the organization chart may show all the positions (ideally grouped by division or function), investors are most interested in and likely looking to acquire your management team. They want to know the management team that they're acquiring is worth their investment.

Healthcare market

In many healthcare verticals, the market is known or assumed, but potential buyers want to know how big the opportunity is associated with your company. Yes, they may plan to expand your business, but the core market is a starting point, and they want to know that you know it.

Beyond providing a market overview, also provide a clear picture of your audience. What is your market size? Who are they, and how many are in your market? How do you reach/communicate with your audience? What are your referral sources? What is your market position?

When putting together this market analysis, you may decide to share the "total addressable market" (TAM), which includes every potential member of your audience seeking services or products from your business, or you may decide to refine it to your "total serviceable market" (TSM), which are the customers you are able to reach.

Business model

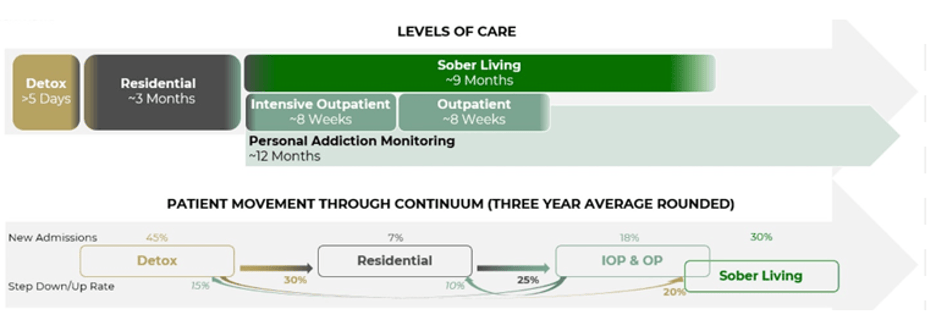

How do you make money? Who pays you, how much, when, and from where? I've seen sellers drop the business model canvas into a pitch, but that may signal inexperience. You should be able to synthesize your business model into a succinct, visual, and possibly creative way where everyone can understand the model.

For example, with substance use disorder (SUD) providers, I model the American Society of Addiction Medicine (ASAM) continuum in a visual, then overlay the company's position in the continuum and add relevant data. See an example below. It's a simple visual to depict a client's business model, and even an investor not experienced in the space will understand exactly what the client does, how they're paid, how patients move around the continuum, and some outcome measurements.

Competition

Not all CIMs include information on competition, but I personally like to discuss it. In the SUD/mental health spaces, it's helpful to see the density of providers in a geography since that helps buyers understand in-network reimbursement rates better.

When providing a competitive analysis in the CIM, you do not need to know and/or identify every competitor, but you should have command over the competitors in proximity to your operations. Communicate how they're trying to address the problems you're working to solve and how your solution is similar or different — or whether any difference matters.

If you have a competitive advantage, share it. If your service is similar to your competitors, leave this section out. It may be unnecessary and spur questions you don't want to answer.

Business growth

Buyers deploy capital to generate a return on their investment. How might they generate a higher return on capital with your asset versus another? While you might not receive the "credit" in valuation for future revenues associated with growth (the buyer will need to do the work to achieve that growth, so they're not going to pay for it ahead of time and be accountable to execute it), you'll see increased interest from potential buyers if you can show demonstratable pathways to that growth.

Case studies that highlight a recent initiative and discuss how that initiative and its success can be reproduced is one effective way to demonstrate growth opportunities. In SUD, this may be a new level of care in an existing geography or starting an intensive outpatient program (IOP) to see if there's demand in a new geography before launching a residential treatment center (RTC). In mental health, a case study might speak to marketing to new populations, telehealth, psychedelics, or transcranial magnetic stimulation (TMS). Including data points that give a clear picture of the path toward growth can effectively demonstrate growth potential.

There are areas of low-hanging fruit for growth in most businesses. Even if they seem obvious, explain them. There are also growth initiatives you may have considered but chose not to pursue due to the effort, capital requirements, lack of manpower, lack of expertise, or simply because you were approaching a sale. Put numbers and timelines to these initiatives and offer the buyer a blueprint to a higher return on capital.

You're the expert. Help show it in the CIM. Buyers want to know what you might do to grow first before considering their own plans.

Financial overview

Historical and projected financials are key elements to a CIM. Explain volatility, and defend the proforma. Potential buyers will scrutinize any years where revenue and expense variance were substantial, so it helps to set the narrative for those likely questions in the CIM.

It's best that proformas provide a realistic outlook for the current scope and scale of the business if it is mature or a defensible and conservative outlook for growth initiatives for a newer business or startup. Sellers tend to have a bright outlook for future performance, but buyers know that storms can quickly appear in even the bluest of skies. In other words, your proforma should point "up and to the right" (it would be uncommon for an owner to believe plans will result in declining revenues) but avoid signaling inexperience by including assumptions that paint an unrealistic or overly optimistic growth trajectory.

Make sure the data you've peppered throughout your CIM clearly ties to and is reflected accurately in the proforma. We call this "tick and tie," where advisory teams put a "tick" mark next to every data point in a CIM and "tie" them out to all the other data to ensure everything checks out. If you don't tick and tie your CIM, there's a good chance a buyer will — and if they do, expect them to catch any errors, which will damage your credibility.

Metrics

Not all businesses operate off metrics, which is a travesty. If you have metrics, the key is to compare yours to industry norms. Common metrics in healthcare businesses include prior authorization versus claims collected, census, inventory turnover, and rounding, so you should be able to identify the benchmarks (a healthcare M&A advisor will help with this as well). If you have substantial variance from any benchmarks, you must address the reason(s) why. It's better to have an upfront explanation than to let buyers discover these variances and develop their own narrative for why your business is underperforming.

Creating An Optimal Healthcare Confidential Information Memorandum

Developing an informative and effective healthcare CIM takes time, expertise, comfort with software, and other skills. An experienced M&A advisor will have these skills or a team supporting them with such talents. An advisor will know how to present your company's most important data and what data to omit. An advisor will also know how to pepper the CIM with data points allowing buyside analysts to prepare their own models so they can analyze your business operating in their portfolio or model.

Completing a CIM is possible without an expert M&A advisor but doing so is not without risks. For most business owners, the work required to create a proper CIM is usually difficult to effectively execute while operating and leading the company and do so in a way that creates a limited auction for the company.

Since the CIM is essentially the first true experience, interaction, and impression a potential buyer will have with you and your company, it's likely in your best interests to hire a healthcare M&A advisor and task them with taking the lead on drafting the CIM. This will better help ensure the final document communicates what buyers want to see, positions your business correctly under current market conditions and buyer interests, and gives qualified buyers a starting point for the "coffee meetings."

David Purinton, MBA, CM&AA

After working in M+A advisory and corporate financial consulting, I was fortunate to co-found Spero Recovery, a provider of drug and alcohol recovery services with over 100 beds in its continuum of residential, outpatient, and sober living care. As its CFO I led the company to significant revenue and margin growth while ensuring it adhered to the strictest principles of integrity and client care. After selling Spero I remained in leadership with the buyer as its CFO and quickly realized accretion and integration. Of the myriad lessons not learned while earning my MBA with Distinction in Finance from a Tier 1 university, the most profound was the importance of investing in my staff and clients. I learned that the numbers on a spreadsheet represent humans, families, and dreams, which was a radically different paradigm from investment banking.

At VERTESS I am a Managing Director providing M+A and consulting services to the Behavioral Health, Substance Use Disorder treatment, and other verticals, where I bring a foundation of financial expertise with the value-add of humanness and care for the business owners I am honored to represent.

We can help you with more information on this and related topics. Contact us today!

Want to stay current with trends in the medical/healthcare space as well as receive expert advice of veteran medical entrepreneurs?

SUBSCRIBE TO OUR BI-WEEKLY NEWSLETTER VERTESSPRESS

For over 10 years, we've been teaching ways you can improve the value of your healthcare company, focusing on informing you about mergers + acquisitions, including M+A trends in the healthcare market.