If you own a healthcare company, you are probably receiving inquiries from interested buyers. We view this as buyers marketing themselves to you. At VERTESS, we emphasize the importance of clients marketing their company to buyers as a key step in securing the eventual right buyer and partner.

With potential buyers coming and marketing to you, why should you put in the time and effort to market to potential buyers?

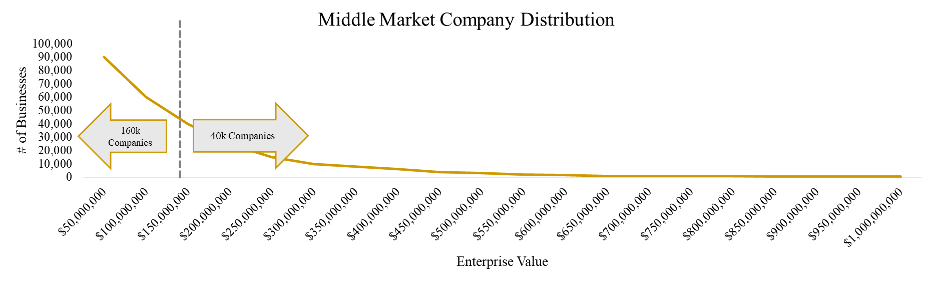

To answer this question, it's helpful to take a step back and understand the current market for sellers and buyers, specifically focusing on the lower middle market. This market has the vast majority of operating companies since most companies have under $150 million in enterprise value, as the following chart represents:

Given the volume of potential targets, there are more investors in the lower middle market than you can probably imagine. The role of these investors (i.e., buyers) is generally to acquire founder-owned companies, professionalize them, scale them organically and inorganically, integrate them, and then sell the larger entity to the next investor. The acquired company scales up as it passes through the hands of various investors.

These investors are financially motivated to market themselves as the appropriate buyer for your company. After all, they stand to make millions of dollars when their acquisition and subsequent growth and transaction strategies succeed. They're aggressively trying to find companies to buy and then execute these strategies.

Buyers view their outreach efforts as a sales cycle. They reach out to X number of business owners, hope that Y number of business owners will engage in discussions about selling their companies, and then the buyers weed out the companies they don't want to own, ultimately acquiring Z. In this sales cycle, buyers are essentially in control.

Owners who market to potential buyers take control of the sales cycle — one that's very similar to the cycle executed by buyers. Owners, usually supported by healthcare M+A advisors like those at VERTESS, reach out to X number of potential buyers and hope that Y number of buyers will engage in discussions about buying the company. Owners and their M+A advisors then weed out the buyers the owners don't want to sell to. The remaining options are engaged in discussions about the potential acquisition, ultimately concluding with the owner signing an agreement with Z.

The Value of Control

Putting the power on your side of the equation matters. Consider the following reasons:

More likely to find the right fit. There are several thousand healthcare investors. Not everyone is going to be a good fit for your company. In fact, most will not. Similarly, a random buyer is not likely to magically be the right fit for you. When you control who you market your company to, you are more likely to market toward companies perceived as potential good fits.

Investors will know you're ready to sell if you're marketing to them. This increases interest and reduces risk. When buyers find potential targets by marketing to companies, the investors usually do not know how willing a seller is to sign a contract. Given the costs of due diligence, that lack of knowledge presents a six- or seven-figure risk.

However, when an owner markets to buyers, investors feel more comfortable spending money in due diligence since they know the owner is more likely to sign the contract at the end of the process. The appearance of an owner interested in at least considering a sale attracts a greater number of investors.

Likelihood of better results. When you can identify multiple potential buyers who might be a good fit for your company, you put yourself in a position to leverage the interest in your asset to negotiate up valuation and terms. You cannot do this without leverage, as buyers aren't interested in spending more money to acquire your business unless they have competition — and competition perceived as legitimate and strong.

Tips for Buyers

While we understand the strategy, we respectfully ask that you stop showing premium valuations in your letters of intent (LOI) to unrepresented sellers. You may not see it as a bait-and-switch tactic, but that's exactly what the seller experiences, and they leave the process believing the initial offer is still achievable with someone else. Even if re-trading has worked for you in the past, this is the kind of tactic that makes sellers skeptical of any buyer.

If you're looking for off-market deals, be prepared for the time and effort required to achieve a discount. First and foremost, develop the relationship before discussing valuation. If the seller asks for an indication of value too soon, you probably know it's not going to the finish line. Cut bait and move on until you find a potential seller willing to spend time forming a relationship with you that can eventually be leveraged into a sale.

If you haven't already done so, create a pre-LOI request list and open a data room. You should have about 75% confidence in a deal before signing an LOI. Submit an LOI that you would submit to an M+A advisory firm like VERTESS. Start with a cash deal you're prepared to execute, then add structure if there's a valuation gap. It's difficult to re-trade down.

Meet With Me at TCIV

I'll be attending TCIV East in Palm Beach Gardens, Florida, from April 15–17. If you will be attending this conference and are interested in meeting up to discuss the topics covered in this column or any other issue concerning M+A, please reach out to me using my contact information below.

Here to Help

If you're an owner thinking about selling, contact the M+A team at VERTESS. We're specialized healthcare advisors who help our clients with exit planning and executing that plan, including marketing directly to those buyers likely to be a good fit for your company and serious about executing an acquisition. We'll help you determine the right path forward for the sale of your business and then do much of the heavy lifting that typically ends with a successful transaction.

David Purinton MBA, CM&AA

After working in M+A advisory and corporate financial consulting, I was fortunate to co-found Spero Recovery, a provider of drug and alcohol recovery services with over 100 beds in its continuum of residential, outpatient, and sober living care. As its CFO I led the company to significant revenue and margin growth while ensuring it adhered to the strictest principles of integrity and client care. After selling Spero I remained in leadership with the buyer as its CFO and quickly realized accretion and integration. Of the myriad lessons not learned while earning my MBA with Distinction in Finance from a Tier 1 university, the most profound was the importance of investing in my staff and clients. I learned that the numbers on a spreadsheet represent humans, families, and dreams, which was a radically different paradigm from investment banking.

At VERTESS I am a Managing Director providing M+A and consulting services to the Behavioral Health, Substance Use Disorder treatment, and other verticals, where I bring a foundation of financial expertise with the value-add of humanness and care for the business owners I am honored to represent.

We can help you with more information on this and related topics. Contact us today!

Preparing an ambulatory surgery center (ASC) for a sale is a worthwhile process for center owners regardless of whether they intend to sell their facility in the near future. The process examines an ASC from a potential buyer's perspective, generating tremendous insights into where an ASC is thriving (what a buyer would find attractive) and where it needs improvement (what a buyer would find troublesome). With this information, owners can undertake initiatives that would further strengthen the ASC's infrastructure and operations, likely leading to financial improvements and increased competitiveness while putting the center in a stronger position for an eventual sale.

The following are six key recommendations for how ASC owners can run a more successful center — recommendations that will also set owners up for a successful sale.

1. Think about growth from the start

When opening a new ASC, owners are typically hyper-focused on getting to the finish line so they can open the doors and start performing procedures. But at least some energy and resources should go toward building a strong business foundation. Doing so will not only help an ASC succeed, but it will become more attractive for investors.

Among the key steps owners should take early in the ASC's development include assembling business and supply teams with healthcare and preferably ASC experience who can keep owners current on performance, trends, and developments. Owners should ensure they or their administration carefully research software choices and revenue cycle management (RCM) service partners if they intend to outsource some or all of RCM. Also, prioritize ensuring processes are not duplicated and automation is fully leveraged wherever possible.

2. Develop a basic exit plan when you're developing the ASC

Another important step to take early in an ASC's history — and likely even before the ASC opens — is understanding the future exit plans of your physicians and business partners, even if it's many years away. Such alignment is essential early and only becomes more critical as owners approach their exit phase. When you choose physicians to work at your ASC, they must be willing to purchase equity in the center, be willing to work under the umbrella of a corporate entity, and be receptive to an eventual acquisition.

One of the biggest mistakes a physician-owner can make is selling their ASC when they are ready to retire, unless certain steps are taken in advance. These include keeping the business scalable and making the transfer of vendors, maintaining employee retention, and keeping a transferable payer structure top of mind.

Also, be careful not to have one or just a few physicians perform a majority of your cases unless you are confident that these physicians will buy in to an acquisition. This will be critical to a buyer's ability to acquire your center or become your strategic partner.

A key test when preparing your ASC for an acquisition is to assess what would happen if you took a vacation for 4 weeks. If the business would still run smoothly and continue to perform well financially, the center is likely in good shape for a sale. If a vacation of 4 weeks would cause significant harm to profitability and operations, this should be viewed as a red flag.

3. Take time to understand the business side of running an ASC

ASC owners cannot afford to be absent from the business side of the facility. A lack of engagement can lead to poor decisions that harm financial performance, hinder growth, and lead to a disappointing exit. Owners should take the time to understand critical concepts like acceptable accounts receivable ranges, bad debt, and key performance indicators, and the benchmarks for the costs of clinical and non-clinical staffing.

Owners would be wise to pay market salaries and distributions to themselves and their partners as anything above market is likely to be frowned upon by a prospective buyer and new partners.

When hiring staff, seek professionals who are likely to remain with the ASC following an acquisition and generally avoid hiring and promoting through nepotism unless the individuals are qualified and expected to remain on staff when there is a transfer of ownership.

Owners should understand and be involved in vendor contact negotiations to help achieve cost savings for their ASC.

Finally, if possible, owners should surround themselves with physician-owners and non-physician-owners who have been through acquisitions to help with understanding the process and what's required for success.

4. Conduct periodic self-audits to identify opportunities for improvement and growth

Don't develop an ASC that has a mentality of: "This is how we always have done it, so we are not going to change." Change is critical to success, both when change will correct a problem and when change will improve performance.

How do you discover what you should change? Conduct internal audits, and be proactive in preparing for surveys, such as those conducted by your state and accreditation organization. Provide continuing education for staff, have a thorough onboarding orientation process for new hires, and encourage team members to always speak up when they have suggestions or concerns (i.e., creating a "just culture"). Build a culture that protects your patients backed by policy and supported by best practices.

5. Prioritize treating patients, but don't lose sight of the business

Patient safety and quality of care are always first, but if you don't manage your expenses and pursue growth opportunities when they present themselves, you may end up with the best ASC that went bankrupt. And a bankrupt ASC can't help patients.

6. Step up sales preparation several years in advance

While planning the exit from your ASC should be an ongoing process, there is an optimal time to step up your preparation. When you believe you have about 5 years left of performing surgical procedures, begin to more seriously consider your exit and seek ways to further increase value and buyer interest in the center.

This is also a good time to list the center and consider taking on a strategic partner, especially if you're interested in maximizing your earnings from the sale through a rollover (i.e., equity roll).

The Sooner You Start Thinking Sale, the More Successful You Will Be

If you own an ASC and are thinking it's time to sell your facility or if you're wondering what you can be doing to best position your center for a sale, I'd welcome the opportunity to speak with you and talk through your opportunities. Please contact me using my information below. If you're interested in learning more about how to know when it is time to consider a strategic partner, I discussed this topic on the HST Pathways "This Week in Surgery Centers" podcast. You can listen to the episode on YouTube or through platforms like Apple Podcasts and Spotify.

J. Blake Peart RRT, CM&AA

I have had the opportunity of an extensive and diverse career in healthcare for over twenty years. In the past ten years, I have served as CEO for multiple hospitals of Fortune 500 companies and CEO for several large Ambulatory Surgery Centers. In addition, my operations and business development knowledge has allowed me to experience the entire M&A process from start to finish focusing primarily on private equity transactions. My history as both a CEO and clinician provides a unique perspective based on years of experience and empathy when working with business owners seeking M&A advice. My expertise is in Ambulatory Surgery Centers, Physician Practices, and independent hospital businesses. I am here to support healthcare business owners who select the M&A direction as one who has walked in their shoes. I know that every transaction is unique and tailored to a seller’s need in getting the best deal and providing a positive experience throughout the entire process.

We can help you with more information on this and related topics. Contact us today!

by David E. Coit, Jr., DBA, CVA, CVGA, CM&AA, CBEC

After spending many years building your healthcare company, it's increasingly likely that you will find yourself thinking about the prospects of selling it. Whether you have a formalized exit strategy or are taking a "seat-of-the-pants" approach to preparing for sale, you must be able to view your company from a buyer's perspective.

More specifically, you will want to understand the key "value drivers" of your company. These are the qualities prospective buyers are most interested in seeing and learning about. To gain a better understanding of how your company is performing — specifically concerning these value drivers — buyers will typically ask you the following questions:

Does your company have a history of consistent growth?

Is your company part of a growing sector?

Are you increasing your share of the market?

Have you created barriers to competition?

Are any of your customers/patients contractually committed?

Are any of your products or services unique, and do they provide you with a competitive advantage?

Do you have a recognizable brand?

Is your company innovative?

Are you utilizing state-of-the-art technologies?

Do you enjoy net margins greater than the industry average?

Do you have a diversified customer/patient base?

Do you have a diversified payer mix?

Are you using best practices for accounting and financial matters?

Is your company sustainable without you?

Are your products or services delivered in a systematic and process-driven manner?

Do you track key measures of customer/patient satisfaction?

Do you have a skilled leadership team that succeeds in meeting or exceeding your goals and objectives?

Can your company attract, develop, and retain quality employees?

Are all your company's legal matters in order?

If you find it difficult to confidently answer these questions, your company might not be ready to sell, or at least not sell at a price you desire (To gain a better understanding of whether your company is likely to sell, I encourage you to read my column, "How to Determine the Probability of Closing a Healthcare Transaction"). The good news is that holes in your operations that may stand in the way of a successful transaction are usually fixable.

Preparing your company/practice for sale may require the following steps:

Financial statements: Ensure your financial statements are accurate and up to date. This includes balance sheets, income statements, and cash flow statements.

Document processes: Clearly document all operational processes. This can make the transition smoother for the buyer.

Legal compliance: Ensure your business is compliant with all relevant laws and regulations.

Market analysis: Understand your market position, including strengths, weaknesses, opportunities, and threats,

Self-due diligence: Conduct a thorough internal due diligence process to identify and address any potential issues before they are discovered by a buyer.

M+A and legal: Engage experienced healthcare M+A and legal advisors to guide you through the selling process.

Deal structure: Determine the preferred deal structure (e.g., asset sale vs. stock sale) and negotiation terms.

Contingency planning: Anticipate potential issues and have contingency plans in place.

Tax advisors: Consult with tax advisors to optimize the tax efficiency of the transaction.

Timing: Consider market conditions and the economic environment when deciding the timing of the sale.

Customer relationships: Strengthen customer relationships to enhance the perceived value of the business.

If you intend to sell your company in the near or at least the not-so-distant future, don't delay. The healthcare M+A market is very active, and this activity is expected to continue in 2024. Buyers are eagerly acquiring healthcare companies that create investor/buyer value. Company owners only have one opportunity to make a first impression on buyers. Will your first impression lead to a successful sale at the price you want for your company, or will it leave you with long-term regrets?

The work you put in today can significantly influence the reward you earn tomorrow. That work will likely be easier and that reward increased by partnering with a healthcare M+A advisor, such as one from our team at VERTESS. Learn what we can do for you and your healthcare company by reaching out using my contact information below.

David E. Coit, Jr., Director of Finance + Valuation / Partner

David is a seasoned commercial and corporate finance professional with over 30 years’ experience. As part of the VERTESS team, he provides clients with valuation, financial analysis, and consulting support. He has completed over 150 business valuations. Most of the valuation work he does at VERTESS is for healthcare companies such as behavioral healthcare, home healthcare, hospice care, substance use disorder treatment providers, physical therapy, physician practices, durable medical equipment companies, outpatient surgical centers, dental offices, and home sleep testing providers.

David holds certifications as a Certified Valuation Analyst (CVA), issued by the National Association of Certified Valuators and Analysts, Certified Value Growth Advisor (CVGA), issued by Corporate Value Metrics, Certified Merger & Acquisition Advisor (CM&AA), issued by the Alliance of Merger & Acquisition Advisors, and Certified Business Exit Consultant (CBEC), issued by Pinnacle Equity Solutions. Moreover, the topic of his doctoral dissertation was business valuation.

David earned a Doctorate in Business Administration from Walden University with a specialization in Corporate Finance (4.0 GPA), an MBA from Keller Graduate School of Management, and a BS in Economics from Northern Illinois University. He is a member of the Golden Key International Honor Society and Delta Mu Delta Honor Society.

Before joining Vertess, David spent approximately 20 years in commercial finance, having worked in senior-level management positions at two Fortune 500 companies. During his commercial finance career, he analyzed the financial condition of thousands of companies and had successfully sold over $2 billion in corporate debt to institutional buyers.

He is a former adjunct professor with 15 years' experience teaching corporate finance, securities analysis, business economics, and business planning to MBA candidates at two nationally recognized universities.

Want to stay current with trends in the medical/healthcare space as well as receive expert advice of veteran medical entrepreneurs?

SUBSCRIBE TO OUR BI-WEEKLY NEWSLETTER VERTESSPRESS

For over 10 years, we've been teaching ways you can improve the value of your healthcare company, focusing on informing you about mergers + acquisitions, including M+A trends in the healthcare market.