Private equity often carries a negative connotation in the healthcare industry. However, if you are considering selling your business, it's crucial to understand the impact private equity has on the overall deal market and the sale of your company. At VERTESS, we focus exclusively on transactions in various healthcare sectors. By tracking the activity of private equity groups, or PEGs, we gain insights into the current market dynamics, allowing us to better advise our clients on what to expect when selling their businesses.

In this column, we will briefly define private equity, then dive into the influence of it on the sale of healthcare businesses, current trends in healthcare private equity activity, and what business owners should consider when planning to sell their companies.

What Is Private Equity? Private equity is an alternative investment strategy that allows institutional and accredited investors to invest in private markets. These groups invest in private businesses to increase their value over a holding period — one typically lasting 5 to 7 years. PEGs have an ultimate goal of selling the businesses for a profit.

One strategy for increasing the value of these portfolio companies is through mergers and acquisitions (M+A), where companies consolidate multiple businesses under a single entity. By acquiring regional and national competitors or businesses with synergistic lines, these portfolio companies can add revenue and earnings, thereby increasing their value when sold.

What Influence Does Private Equity Have on Selling Your Healthcare Business?

Why is private equity important for business owners? When you decide to sell your healthcare business, you will likely receive offers from multiple entities, potentially including private equity-backed portfolio companies and private equity funds. Tracking their activity in the market can help you understand what to expect when selling your business. While private equity groups are not the only buyers in the market, knowing how they acquire and invest in companies provides valuable insights into the market as a whole.

Where Things Stand: A Closer Look at Private Equity Activity in 2024

In 2023, M+A activity was sluggish across most sectors and especially in healthcare. High interest rates lowered business valuations, creating a gap between owners' expectations and buyers' valuations.

In the first half of 2024, private equity showed signs of recovery in the global M+A market. After a slow start, private equity deal activity increased, stabilizing its market share and alleviating concerns about private equity's role in the anticipated M+A rebound. Exit activity, crucial for healthcare industry growth, improved significantly after a long period of stagnation, elevating fundraising and capital availability for future investments.

Private equity fundraising exceeded expectations, showcasing the healthcare industry's resilience and continued investor confidence, despite an anticipated slowdown in the latter half of the year. Middle-market funds performed well, in contrast to the more challenging environment for megafunds.

As the stock market includes more smaller cap stocks, private equity valuations and exit opportunities are expected to improve further. The healthcare industry's adaptability and forward momentum amid challenging conditions highlight its potential for continued growth and success.

Looking at the more recent quarter of 2024 (Q2), healthcare private equity activity showed promise despite a lighter quarter overall. The healthcare sector accounted for a substantial portion of deal activity, with numerous transactions reflecting strong down-market deal flow. Notable deals included Cotiviti's recapitalization by KKR and Veritas and Thomas H. Lee Partners' acquisition of Agiliti, indicating ongoing interest in healthcare investments. Healthcare services dominated private equity deals, while pharma services also attracted significant interest, with multiple platform deals closing.

The demand for weight-loss drugs sparked interest in peptide manufacturing, aligning well with private equity's focus on consistent business models. Despite high valuations and economic uncertainties, the healthcare sector remains robust for private equity investment, driven by strategic acquisitions and divestments.

In conclusion, the first half of 2024 has shown encouraging signs of recovery and growth for private equity in both the general M+A market and the healthcare sector. Improved deal activity, strong fundraising, and strategic investments indicate a resilient and adaptable industry poised for continued success. The healthcare sector, in particular, remains a key area of interest for investment groups, with ongoing investment opportunities driven by market demand and strategic divestments.

Current Private Equity Activity Is Good News for Healthcare Business Owners

Understanding private equity activity is crucial for healthcare business owners considering selling their companies. The current market conditions in the first half of 2024 have shown recovery and growth in private equity, particularly in the healthcare sector. Improved deal activity, strong fundraising, and strategic investments indicate a resilient and adaptable industry poised for continued success.

As deal activity increases for private equity firms, this signals that buyers will be actively seeking investments in the healthcare market. Private equity firms aim to increase the value of their investments through market consolidation and eventually exit from these investments in the coming years. This positive trend in deal activity among private equity firms suggests favorable conditions ahead for the sale of healthcare businesses, regardless of their size. For business owners, staying informed about private equity trends and market dynamics can provide valuable insights and better prepare them for potential sales, ensuring they achieve the best possible outcomes in a competitive market.

At VERTESS, we specialize in healthcare M+A transactions by working with business owners to capitalize on these market opportunities and negotiate the best deal possible for their business. We have built a network of relationships with buyers in our key verticals to ensure we bring the right pool of buyers to any client. This will help not only achieve the best outcome in purchase price but also the best post-transaction fit for their business, employees, and clients. If you would like to learn more about the state of healthcare M+A and investing or how VERTESS is particularly well-suited to help sell your healthcare business, please reach out to us.

Dave Turgeon, CM&AA

I’ve been fortunate to work for several exceptional companies. I’ve contributed in roles that include CEO, COO, and managing growth. I’ve been part of private equity-backed companies focused on building value and growing, which has allowed me to acquire of hundreds of companies and invest billions of dollars. I began focusing on behavioral health about twelve years ago based on a family member. Many people know me from my experience running the M&A efforts at Civitas Solutions leading up to their successful IPO in 2014. I feel very fortunate to be in a position now to help business owners who built companies whose mission it was to care for others. I’m in the unique position of helping them get the very best deal possible

As a Director at VERTESS, I bring extensive experience in sales, consulting, and project management from early-stage startups. With an MBA from Babson College, I have a strong foundation in business strategy, operations, and financial analysis. My personal connection to behavioral healthcare through a family member motivates me to help business owners get the best deal possible while ensuring high-quality care for their clients. Throughout the M&A process, I provide comprehensive support at every step. I have a proven track record in negotiations and client management after working with companies in various industries. I’m excited to join VERTESS and make a meaningful impact on the lives of the owners I work with.

We can help you with more information on this and related topics. Contact us today!

Volume 11, Issue 12, July 2nd, 2024

By: David E. Coit, Jr., DBA, CVA, CVGA, CM&AA, CBEC, CAIM

Why should a buyer's costs of integrating an acquired company be of interest to the seller? The most important reason is that sellers often pay part or all the integration costs of the buyer. According to McKinsey & Co., the average cost of integration is between 15% and 20% of an acquisition's purchase price.

How do buyers' integration costs become a concern for sellers? Buyers typically determine the offering price based on expected future cash flows received from the acquired company. When buyers estimate future cash flows, they often include the anticipated costs of integrating the acquired company. Thus, the purchase price is often net of the buyer's expected integration costs.

If you're considering a sale of your healthcare company, you might be wondering: What can I do to influence the buyer's cost of integration?

That's a great question! There are several actions sellers can take before going to market that can reduce the buyer's integration costs. Moreover, those cost savings may allow potential buyers to increase their offering price because of a perceived increase in first-year cash flows from the acquisition.

How to Cut Healthcare Acquisition Integration Costs

Let's discuss eight areas where sellers may want to take steps before selling their company that can reduce a buyer's integration costs and potentially increase offers and the final sale price.

1. IT software applications

Buyers typically migrate the information technology (IT) used by an acquired company to match the applications the buyer uses. Software migration can be a costly and time-consuming process, especially if the seller is using legacy systems and outdated technology, in-house developed software, and/or has inaccurate or incomplete data. On the other hand, using widely used, industry-specific applications and having clean and current data will considerably ease the migration process.

In addition, providing buyers with a listing of IT applications used, the methodology of data collection and data verification, and a scheduled IT software maintenance program will allow buyers to better determine the estimated time and expense of IT integration.

2. Repair and maintenance

Believe it or not, some sellers defer routine repair and maintenance in the months leading up to the sale of their business. While this may seem like a good way to increase the seller's cash flow before selling their business, buyers will likely discover such deferred expenses during due diligence and predictably take a dim view of such actions. Moreover, buyers will estimate their costs of remedying or mitigating the deferral.

It's better to keep up with scheduled repairs and maintenance as though the business wasn't being sold than having buyers decrease their offering price to account for these necessary expenses. However, sellers should not needlessly incur excess repair and maintenance costs before going to market. Keep in mind that companies sell for a multiple of cash flow. As such, every dollar increase in cash flow returns a greater dollar amount in the price of the company.

3. Turnover

Buyers usually expect a post-acquisition drop in the acquired companies' revenue due to employee turnover, client/patient turnover, or referral source turnover. A key aspect of integration is the retention of essential employees, clients/patients, or referral sources.

If the seller can show buyers that they've taken and will continue to take actions to mitigate turnover, buyers will be less concerned about revenue loss and the associated costs of retention. In addition, sellers who demonstrate a commitment to work after the sale to address possible retention issues show good faith to prospective buyers.

4. Capital expenditures

Buyers often expect that sellers have underinvested in capital expenditures (Capex) leading up to the sale of their healthcare businesses. Appropriate investment versus underinvestment is a difficult issue to address. On the one hand, replacing older equipment does not necessarily increase the offering price from buyers. On the other hand, buyers may adjust their offering price after due diligence once they've determined the estimated costs associated with underinvestment.

A good rule of thumb is to continue Capex dollars based on historical needs. In other words, consider keeping up with maintenance Capex but limit the amount spent on long-term growth Capex. The most typical underinvestment in Capex is new computers for employees. Beware of acquiring new computers that may not meet the buyer's IT specifications. In other words, be smart and frugal with CapEx dollars before going to market.

5. Facilities

Before interacting with potential buyers, a seller won't know the facility needs of buyers. Many buyers don't want to own real estate. Others may have operations with excess capacity near the seller's location(s).

Perhaps the best way to address the issue of facilities is (1) the seller should not undertake any leasehold improvements before going to market, (2) sellers should avoid long-term lease extensions or related commitments, and (3) if the facility(ies) is/are owned, consider looking into alternative options should the buyer chose not to acquire real estate. Sellers don't want to be in a position where the buyer decreases the offering price because the seller needs to unwind facility(ies) commitments.

6. Open staff positions

It's commonplace for sellers to avoid filling open staff positions before selling their business. Such situations can be a two-edged sword. The buyer will discover unfilled positions during due diligence and factor in the cost of filling the positions by repricing their offer. On the other hand, the seller may be able to fill open positions at a wage rate or salary lower than the buyer's estimated compensation. Conversely, the buyer may be able to fill certain open positions where the buyer has existing staff to fill open positions.

I recommend the seller discuss this matter with their healthcare M+A advisor or potential buyers before the buyers make an offer to acquire the business. One other consideration is the potential to outsource open positions with independent contractors. For example, contracting with a fractional chief financial officer rather than hiring a full-time CFO.

7. Contracts, licensing, certifications, and subscriptions

Buyers will discover any past-due, expired, or soon-to-expire contracts, licensing, certifications, or subscriptions (CLCS). Sellers should keep essential CLCS' up to date. However, before going to market, sellers should evaluate each CLCS to determine the value of reviewing or extending the CLCS. For example, older certifications may be of little value because of changes in the industry. Similarly, certain subscriptions may not be of value to buyers and thus an unnecessary waste of funds.

For example, some physicians elect to be members of various associations like the American Medical Association, Medical Group Management Association, and/or state medical societies. If these CLCS do not drive revenue or business value, consider not renewing the CLCS.

8. Accounting/financial reporting

We regularly advise our clients whose financial reporting is on a cash basis to convert to an accrual basis before going to market. Accrual basis accounting is a more accurate method of financial reporting than cash basis accounting. We also recommend that their accrual basis accounting conform with generally accepted accounting principles (GAAP).

One way to ensure that a company's financial statements are GAAP compliant is to have a CPA firm perform an audit. Audited financial statements can provide buyers with confidence in the reliability of the financial reporting.

An alternative to having audited financial statements is to have an accounting firm prepare a seller's quality of earnings (QofE) examination. A QofE is an assessment of a company's performance that removes anomalies and poor accounting or bookkeeping methodologies, and more accurately reports a company's true performance.

Many buyers will undertake a QofE as part of their due diligence process. When sellers provide buyers with a seller's QofE report, as my colleague Bradley Smith discussed in this column, buyers gain confidence in the accuracy of the seller's financial reporting.

Moreover, buyers may either accept the seller's QofE rather than having a third party perform a QofE or hire a CPA firm to review the seller's QofE report. In either case, the buyer saves time and money and will be able to quickly determine the riskiness of the seller's company.

Impact on a Potential Healthcare Acquisition

Imagine you are looking at acquiring one of two healthcare companies in your industry. One of the companies uses similar IT software applications as you; keeps current on routine repairs and maintenance; has a sound record of low employee turnover; has no underinvestment in Capex; has the option to renew their facility's lease (which is now month-to-month); has no unfilled staff positions; is current with all contracts, licensing, and certifications; only has necessary subscriptions; and has accurate and verified financial reporting.

The other company is using proprietary or in-house developed IT software applications, is significantly delinquent in routine repair and maintenance; has higher than usual employee turnover; is underinvested in Capex; has a long-term facility lease contract on an undesirable property; has several unfilled open staff positions; is past-due on renewing contracts, licensing, and certifications; has many unnecessary contractual subscriptions; and has numerous accounting errors in their cash basis financial statements. Which company would you be willing to offer a higher purchase price? Which company would you perceive as a risky investment? Which company would you expect to spend less money on during integration?

It's easy to see how putting in some work to reduce acquisition integration costs can lead to more offers and higher offers while increasing the likelihood of a successful sale. If you are thinking about selling your healthcare company and would like to discuss ways to decrease acquisition integration costs and make your business more appealing to prospective buyers, reach out to me or any other member of the VERTESS team. We would welcome the opportunity to speak with you!

David Coit DBA, CVA, CVGA, CM&AA, CBEC, CAIM

I am a seasoned commercial and corporate finance professional with over 30 years of experience. As part of the VERTESS team, I provide clients with valuation, financial analysis, and consulting support. I have completed over 400 business valuations. Most of the valuation work I do at VERTESS is for healthcare companies such as behavioral healthcare, home healthcare, hospice care, substance use disorder treatment providers, physical therapy, physician practices, durable medical equipment companies, outpatient surgical centers, dental offices, and home sleep testing providers.

I hold certifications as a Certified Valuation Analyst (CVA), issued by the National Association of Certified Valuators and Analysts, Certified Value Growth Advisor (CVGA), issued by Corporate Value Metrics, Certified Merger & Acquisition Advisor (CM&AA), issued by the Alliance of Merger & Acquisition Advisors, and Certified Business Exit Consultant (CBEC), issued by Pinnacle Equity Solutions, and Certified Acquisition Integration Manager (CAIM), issued by Intista. Moreover, the topic of my doctoral dissertation was business valuation.

I earned a Doctorate in Business Administration from Walden University with a specialization in Corporate Finance (4.0 GPA), an MBA from Keller Graduate School of Management, and a BS in Economics from Northern Illinois University. I am a member of the Golden Key International Honor Society and Delta Mu Delta Honor Society.

Before joining VERTESS, I spent approximately 20 years in commercial finance, having worked in senior-level management positions at two Fortune 500 companies. During my commercial finance career, I analyzed the financial condition of thousands of companies and successfully sold over $2 billion in corporate debt to institutional buyers.

I am a former adjunct professor with 15 years of experience teaching corporate finance, securities analysis, business economics, and business planning to MBA candidates at two nationally recognized universities.

We can help you with more information on this and related topics. Contact us today!

At least seven out of 10. That's at the low end of how many mergers and acquisitions (M+As) are likely to fail. The high end? Nine out of 10.

These are not misprints. They are conclusions of research, as referenced by Harvard Business Review and other publications. They tell us that 30% of M+As at most succeed, while only 10% are essentially assured to succeed.

These M+A failure and success figures were determined via examination of a large pool of deals in every business sector. Common reasons frequently cited for such a high failure rate include an uninvolved seller, culture shock at the time of the integration, and poor communications from the beginning to the end of the M+A process.

With the odds seemingly stacked against healthcare business owners, why would you consider selling your company, especially if you expect to be invested (financially and/or personally) in the future of the business after a transaction?

At VERTESS, we have found that the M+A process can be navigated and lead to a higher success rate when have the right information and team to work with. It also helps to understand what can go wrong and how to avoid making these mistakes. I personally have a closing rate of about 82%.

Here are 10 of the factors that can lead to failed mergers and what is necessary to overcome the shortcomings.

1. Not knowing the motivations of buyers and sellers

There are essentially two kinds of sellers: one that looks for the most money for their business and one that needs to find the perfect buyer for the individuals, families, staff, and community related to the business. Buyers, on the other hand, come in all shapes and sizes, from strategic buyers that are looking for growth to financial buyers (private equity) looking to build and flip — and many shades in between.

If a transaction has any hope of being a success, it is important to determine the motivations for both parties. At VERTESS, we always discuss what is most important to sellers well before bringing their business to market. We also carefully screen all buyers to understand their intention and assess if there is a good fit.

These steps help with winnowing down what could be a lengthy list of prospective buyers to those that align well — at least on paper — with a seller. If there isn't good alignment, there is likely no reason to continue conversations with a prospective buyer.

2. Unrealistic expectations

It's not unusual for sellers to believe they should receive a certain amount of money — usually a particularly high amount — for their business because that's what they believed the company was worth. Sellers often estimate what their company is worth after hearing about transactions for other companies in their market, reading articles and columns that discuss multiples and prices paid, or being approached by a prospective buyer that casually threw out some figures.

The numbers sellers envision are often unreasonable. That doesn't mean they don't have a good company that should do well on the market. Rather, it means that most people naturally believe that something they value is valuable — and often more valuable than the market would believe. A financial analysis and valuation can reveal figures that are objective and in line with similar transactions. Most buyers are unwilling to cross certain thresholds, regardless of how amazing a business may be (or seem to be to a seller).

Ultimately, a company is worth what someone is willing to pay for it. The only way to maximize a valuation of a company is to run a process that brings in all the buyers and has them make offers simultaneously. Anything less will likely result in selling your company for less.

A seasoned healthcare M+A professional can help prepare a seller ahead of time for the selling experience, including what offers to anticipate. Both parties should reach an understanding of the expectations of the sale before going to market.

3. Hidden debt and financial instability

Buyers understand sellers sell for many reasons, including the fear of losing the company because of debt or money stresses. However, no one wants to be halfway through a transaction due diligence process only to learn about the numbers trailing downward or worse: the posting of foreclosure notices. This tension for a seller will often lead to poor decisions. Any buyer will be aggressive and take advantage of the situation.

Be forthcoming with your healthcare M+A advisor. Paint the complete, honest picture of your business — its successes and especially the struggles and how you overcame them. Transparency is essential. With a clear understanding of your business, the advisor may have some immediate suggestions to stabilize the situation until the right buyer is found or can help fast-track the process to maximize value.

4. Inaccurate financials

The first step of our process here at VERTESS is to present to sellers a financial picture of their business the way that buyers will assess it. We help formalize even the most difficult financial (e.g., QuickBooks) records. We also complete a proforma that projects future earnings and opportunities.

Despite our best efforts, there are ways these processes can lead to the presenting of incorrect information. How? The numbers we use are provided by the sellers. If the data shared with us is incorrect, we will then be working with incorrect data, and we may not be able to identify all the errors. In addition, most buyers will convert the financials to an accrual basis and expect them to be compliant with generally accepted accounting principles (GAAP). This exercise will compromise a weak set of books and lead to inaccuracies.

We have seen sellers overinflate growth for future years, underestimate the cost of their services, or book revenue incorrectly. We can often secure a great offer with these numbers. However, once under a letter of intent (LOI), the buyer will conduct a quality of earnings (QofE) review. That's often when we learn that the numbers provided to us are not accurate. The result? The buyer either adjusts the purchase price accordingly or pulls the offer.

5. Quality of earnings

Speaking of quality of earnings, in today's healthcare M+A environment, buyers are highly reliant on the QofE report to the point of weaponizing the report to gain leverage on a transaction and ultimately reduce the purchase price. Given these unusual times, I highly recommend completing a seller's QofE prior to going to market.

In my column, "'The Deal Killer': What to Know About Quality of Earnings," I explain that the benefits for a seller that takes this initiative and makes this investment are significant. I further state that it has become a "gamechanger" for sellers. Why?

The buyer will still conduct a seller's QofE at the buyer's expense. However, this QofE will go by quicker and with less disruptions to the transaction process if the seller has completed its own QofE. A seller that completes the QofE can use the insight into its company's financial shortcomings to address any accounting issues identified that could be leveraged against the seller during transaction negotiations. A seller's M+A advisor should be able to help their client avoid most of the challenges and frustrations that can come from a QofE.

6. Change of ownership

It's very easy to change the name of a company owner. For one reason or another, you might decide to put your spouse or child as the owner. No big deal, right? Depends on your plans to sell the company and the regulatory standards of your payers.

In the eyes of many licensing agencies, such as the Centers for Medicare & Medicaid Services (CMS), any "change of ownership" (CHOW) must be reported to these agencies. That's straightforward.

What you may not know is that CMS, as an example, has a rule preventing organizations from undergoing a CHOW more than once every 36 months. If you reported a CHOW 24 months ago, the sale of your company to a new owner would have to wait 12 months.

States often have their own set of regulations around the sale of an organization that could greatly affect how a healthcare transaction should be structured. In addition, every payor will have its own set of rules around the change of ownership, with most payors having preclosing notifications.

To better ensure a smooth sale, know what guidelines exist before you start the process. Your M+A advisor should help you understand the rules that will affect your business and its potential sale.

7. Inflated "add-backs"

During the financial valuation process, we at VERTESS calculate a seller's earnings before interest, taxes, depreciation, and amortization (EBITDA) as well as the adjusted EBITDA. Adjusted EBITDA removes expenses the seller has incurred as a business owner that the next owner will not likely incur, which are referred to as "add-backs." These might be a car payment, executive development coach, or membership at a business club. Adjusted EBITDA is often the basis for valuing the company.

Most buyers will agree with such standard add-backs, but if a seller adds items of a questionable nature that the buyer does not agree with, the purchase price can experience a substantial adjustment. It's important to understand each add-back that you list and be ready and able to support why it is an expense the future owner will not need to incur.

A seller might receive an initial offer that appears generous, but once add-backs are discredited, the price may not be what was anticipated.

8. Lack of communication

The M+A process is lengthy and can take many months — sometimes even a year or more. Effective communication is critical throughout a healthcare transaction, with the communication starting with how your company is represented to prospective buyers during introductions. It becomes more intense when negotiating an LOI and finally during closing. Breakdowns in communication can jeopardize a deal at any stage of a transaction.

Maintaining consistent, transparent communication throughout the due diligence process supports a smoother experience. Expectations should be made clear between the buyer and seller, better ensuring that their post-transaction priorities are aligned. This can help avoid future culture and transition shocks.

Enlisting the expertise of a knowledgeable healthcare M+A advisor to communicate the good, bad, and ugly between buyer and seller can help avoid or at least greatly reduce discomfort and allow each party to work comfortably together following the closing. It is important to know that one person is overseeing each step of the process, from introduction to integration.

9. Poor representation

We have worked with clients that have used their trusted lawyer/friend to represent them during the selling stage. What many of them found was doing so resulted in making the process painfully confusing, time-consuming, and frustrating, often causing the deal to fail.

Let's face it: Buyers are typically experienced and have gone through the M+A process multiple times. Sellers, most likely, have not, which is why they need a lawyer with experience in their area. The details and language involved in a healthcare M+A transaction are often complex. There is often common language and terms that an experienced healthcare M+A lawyer will know to look for. This helps ensure a seller's best interests are represented in the deal.

A knowledgeable lawyer will also not waste time on other common protections for the buyer. If your lawyer is arguing over language or points that are typically standard in a deal, not only are you wasting your time and money, but you may be frustrating and insulting the buyer.

Have someone in your corner who knows the legal pitfalls and vulnerabilities you will encounter during the final stages of a deal. This will help you receive the most protection while making sure you understand the nuances of the legal jargon that will affect the sale of your business.

10. All eggs in one basket

When it comes time to sell your company, you may be tempted to jump at the first prospective buyer that approaches you with a reasonable offer and good fit from a culture perspective. After all, doing so will seemingly reduce the length and stress of the selling process.

This approach can work well, but we have also seen it go south very quickly. The reason: If the buyer knows or believes it's in the driver's seat, it may pay what it thinks is a price likely to get a seller to bite and not necessarily what is fair and appropriate.

Without competition, a seller loses critical leverage and may be pressured into compromises. For example, we worked with a client approached by a buyer directly. This buyer offered an amazing multiple for his company. It was the first offer he received. On paper, the offer looked like a great deal. Unfortunately, once the LOI was signed, the buyer quickly pulled apart the financials and discounted so many items that the multiple was no longer desirable.

Fortunately, the seller was knowledgeable about what he deserved to receive for his company and pulled out of the deal. Unfortunately, he had not engaged in discussions with other prospective buyers, so he lacked alternative avenues to explore. He then needed to start over with us. Had we started the process together, we could have quickly pivoted to other interested buyers when the initial deal fell through.

Making the Best of the Challenging Healthcare Merger Process

The M+A statistics shared at the beginning of this column were not intended to discourage you from selling your company. Rather, these stats help paint a realistic picture of the marketplace. The good news is that with the proper preparation, open communication, knowledge of the transaction process, and support by a team of competent, skilled healthcare M+A advisors, you will greatly increase the likelihood of being in the minority of companies that achieve a successful merger.

To learn how the expert VERTESS healthcare M+A advisors can help you get to the transaction finish line, contact us today!

Bradley Smith ATP, CM&AA

For over 20 years I have held a number of significant executive positions including founding Lone Star Scooters, which offered medical equipment and franchise opportunities across the country, Lone Star Bio Medical, a diversified DME, pharmacy, health IT and home health care company, and BMS Consulting, where I have provided strategic analysis and M+A intermediary services to executives in the healthcare industry. In addition, I am a regular columnist for HomeCare magazine and HME News, where I focus on healthcare marketplace trends and innovative business strategies for the principals of healthcare companies.

At VERTESS, I am a Managing Director and Partner with considerable expertise in Private Equity Recapitalizations, HME/DME, Home Health Care, Hospice, Medical Devices, Health IT/Digital Health, Lab Services and related healthcare verticals in the US and internationally.

We can help you with more information on this and related topics. Contact us today!

Owners of healthcare companies are accustomed to creating financial value for their businesses by focusing on the traditional areas of scope of services, client/patient capacity, and revenue streams via reimbursement yield and patient volume.

While revenue growth and operational efficiency are key value drivers for a healthcare company, neither addresses a critical value factor known as company-specific risk (CSR). CSR, also referred to as unsystematic risk, can be understood as risk unique to a company or industry. Differences in CSR are one of the most significant reasons some healthcare firms get top dollar when sold, while others receive a fraction of their potential sale price.

Let's look at five ways healthcare business owners can increase their financial value by decreasing their CSR.

1. Create a fully developed, written business plan

Few small to medium-sized healthcare businesses create a business plan once they are no longer early-stage companies. Instead, they tend to rely on an informal, ad-hoc approach to planning that relies extensively, if not exclusively, on the activities of the business owner(s).

Taking the time to develop a written business plan at various stages of a company's history provides owners and employees the ability to discuss and create a roadmap that supports the owners' business strategy. A detailed business plan also decreases CSR by addressing issues such as:

Where is the business headed?

How will we get the business there?

How much will it cost us to get the business there?

What are competitors doing to keep us from getting there?

2. Establish an independent and engaged board of directors

Since most healthcare company owners are healthcare professionals who have learned how to be businesspeople through trial and error, they are often not accustomed to seeking advice from seasoned business professionals. That explains why some healthcare business owners believe that assembling a board or directors or advisory board will diminish their independence. However, board members can deliver significant value to business owners by sharing competitive insight, acting as a sounding board for new ideas, enhancing access to growth capital, strengthening company credibility, suggesting alliances, and more.

Company boards reduce CSR by providing strategy guidance, thought leadership, and hands-on experience. Viable businesses often have the support of a group of seasoned business professionals who have a genuine interest in the success of the company.

3. Develop a sustainable corporate culture

Many small to medium-sized healthcare companies have a corporate culture that mirrors the personality of the owner(s). As such, the culture may not be well-suited to capitalize on growth opportunities and may not foster a collaborative environment among disciplines and employees. Moreover, the culture may not actively and effectively develop future leaders throughout the company.

Effective corporate cultures help energize employees, attract new clients, improve the effectiveness of managers, and enhance company reputation. Developing a sustainable corporate culture reduces CSR by lessening the impact of high employee turnover, decreasing unethical behavior, and increasing positive employee interactions.

4. Set up an experienced and focused sales team

Few small to medium-sized healthcare companies have dedicated sales professionals on staff. Instead, they rely on generating business through the likes of referrals and company websites. While these are important for a company's growth, the addition of quality salespeople can be a difference maker. The right sales team can solidify relationships with patients/clients, gather critical feedback regarding the company's performance, and gauge and help a business respond to market trends. A quality sales team can reduce CSR by creating a pipeline of new patients/clients, reducing patient/client concentration, and enhancing barriers to competitive threats.

Why don't many small to medium-sized healthcare companies establish an experienced and focused sales team? Some healthcare providers are under the impression that governmental regulators frown on these kinds of activities. Others believe sales efforts are unprofessional in healthcare. Both perspectives are misguided. Larger healthcare companies almost always have a professional sales staff, which can make it difficult for smaller firms without a sales team of their own to remain competitive.

5. Create and adopt a marketing plan

A well-written marketing plan includes the duties and responsibilities of the marketing person or team, a detailed assessment of the target market, competitive analyses, and brand development, among other topics. A fully developed and adopted marketing plan helps reduce CSR by establishing and sharing knowledge of the company's target market and tactical plans to expand market share. Moreover, a marketing plan establishes a foundation for delivering the desired patient/client experience.

Some healthcare company owners believe that when a marketing plan is created, it will eventually collect dust on the shelf and never be reopened. What they fail to realize is that a functional marketing plan is never finalized. The plan should be treated as a living document that changes as the market environment and the company changes. The plan should also be regularly revisited, evaluated, and updated based upon factors including the success of marketing campaigns, identification of new marketing opportunities, and marketing efforts by competitors.

Learning the Value of Your Healthcare Company

Understanding CSR factors and how to mitigate them can significantly increase company value. To gain a better understanding of your CSR factors, learn about the value of your company, and find out ways you can potentially strengthen the value and performance of your healthcare business, reach out to me or any other member of the VERTESS team. We're help to help!

David Coit DBA, CVA, CVGA, CM&AA, CBEC, CAIM

I am a seasoned commercial and corporate finance professional with over 30 years of experience. As part of the VERTESS team, I provide clients with valuation, financial analysis, and consulting support. I have completed over 400 business valuations. Most of the valuation work I do at VERTESS is for healthcare companies such as behavioral healthcare, home healthcare, hospice care, substance use disorder treatment providers, physical therapy, physician practices, durable medical equipment companies, outpatient surgical centers, dental offices, and home sleep testing providers.

I hold certifications as a Certified Valuation Analyst (CVA), issued by the National Association of Certified Valuators and Analysts, Certified Value Growth Advisor (CVGA), issued by Corporate Value Metrics, Certified Merger & Acquisition Advisor (CM&AA), issued by the Alliance of Merger & Acquisition Advisors, and Certified Business Exit Consultant (CBEC), issued by Pinnacle Equity Solutions, and Certified Acquisition Integration Manager (CAIM), issued by Intista. Moreover, the topic of my doctoral dissertation was business valuation.

I earned a Doctorate in Business Administration from Walden University with a specialization in Corporate Finance (4.0 GPA), an MBA from Keller Graduate School of Management, and a BS in Economics from Northern Illinois University. I am a member of the Golden Key International Honor Society and Delta Mu Delta Honor Society.

Before joining VERTESS, I spent approximately 20 years in commercial finance, having worked in senior-level management positions at two Fortune 500 companies. During my commercial finance career, I analyzed the financial condition of thousands of companies and successfully sold over $2 billion in corporate debt to institutional buyers.

I am a former adjunct professor with 15 years of experience teaching corporate finance, securities analysis, business economics, and business planning to MBA candidates at two nationally recognized universities.

We can help you with more information on this and related topics. Contact us today!

Most successful companies reach points in their history where big decisions must be made that will determine whether these companies largely remain the same size and stay on their current course or undertake significant changes — and usually investments — that lead to a transformation in size and services. Successfully executing this transformation isn't typically easy and often introduces big risks to the viability of the company. For businesses that want to grow, taking risks is a necessity. Fortunately, business can also take steps to reduce the likelihood that these risks will backfire and potentially stifle growth or even cause financial harm.

In this column, I will discuss three types of companies — small, mid-sized, and large — and share key considerations for business owners and operators as they work to successfully move their companies up the growth ladder. Discussions of each company type will be accompanied by a real example of such a company that reached a significant growth turning point and the advice I provided or will be providing that can help turn risk into reward.

Smaller Companies

Let's start with a discussion of smaller companies, and we will define them as companies with revenue between $1 million and $20 million. These tend to be very service-forward companies that often cater to the whim of referral sources and are known in their communities as companies to go to when you want to work with somebody who cares.

That's not to say a larger company can't be a company that cares, but smaller companies tend to have that reputation. In addition, the competitive advantage and differentiator for a smaller company must be its service level — almost bar none. We are in an extremely mature industry that has been on the consolidation trail for a long time. This tells me that if you're a smaller company that wants to stay profitable, flourish, and grow, you need a service component that is your raison d'être.

I recently worked with a small(ish) home medical equipment (HME) company that specializes in diabetes care. It has a few branch locations. The company is known in its community as the company that will be there when push comes to shove. That's their best asset but also their worst detriment because they are known to be the go-to source for everything and anything.

This company recently decided to take on continuous glucose monitoring (CGM) as its next best product area of interest. The service line is being built by a few of the company's core staff members, and it is rapidly taking off. What this tells me is the company is ready to step outside the proverbial small "ma-and-pop" box and into a landscape where it will be able to achieve significant growth.

That's good news for the company, but it presents a big challenge. What they are contending with now is how to tell the community that the addition of this service line and its associated growth will require the company to pull back on being everything to the community all the time. The company still intends to help its customers with anything related to diabetes care because that is its area of specialty, which is supported by a pharmacy. But now the company will be focusing on the CGM line coupled with its CPAP business and other durable medical equipment-related items. That means changes are coming, including only providing one-off items within reason and needing to dropship items like a walker rather than personally deliver it. Alternatively, patients can drop by to pick up their equipment. It may also mean longer times between appointments for homebound CPAP patients and/or a need to deliver equipment and training remotely. And it means that for services that fall outside the company's wheelhouse, the business will refer customers to someone else.

One of the lessons learned for this small — and soon be a mid-sized — company is the importance of determining how to maintain a local feel without needing to be everything to everybody. That is requiring them to focus on the positives — the areas where they can excel as a business — and reduce or eliminate the negatives — the areas that do not make sense for the business. In other words, this company is cleaning up its house, making sure that what people see reflects the business in an accurate, positive way, and eliminating the nonprofitable products and business practices, with very occasional exception.

Mid-Sized Companies

Now let's move to mid-sized companies, which we'll say are those generating between $21 million and $100 million in revenue. They have many locations. They have good processes in place to support the business and growth, but now as they are scaling up and getting closer to becoming large companies, what they need is to become more consistent in the way they run their business.

What do I mean by this? For mid-sized companies, something that often gets overlooked is the notion of being centralized. This can be difficult because mid-sized companies have grown from the successful smaller companies that had a local feel and presence, but now with the larger contracts they have with insurance companies, these mid-sized company must be more consistent in the way they do their business across the enterprise. They must create "by rote" functions, to some extent. They must promote centralization of functions such as purchasing, for example. To further scale the company, non-routine or exception tasks should be reserved for leaders or higher skilled staff.

The challenge and opportunity here is how to achieve this consistency and continue growing without needing to add significant additional human resources that can cut into profitability. This points to the need for automation. Mid-sized companies must explore how to use automation and to begin exploring machine learning in ways they have not yet entertained.

Quickly emerging are the many companies offering services powered by machine learning. Mid-sized companies must start to look at these companies and their services as potential ways to continue to meet payer contract expectations and then be able to scale the company without needing to add extensive resources.

Consider that to handle orders that come in, mid-sized companies generally rely on people to process them. Sometimes that work is performed in-house; sometimes it's outsourced. But in either situation, it's a people-driven process. A person needs to go through the documentation with each order and find the chart note, the prescription (medical necessity form from the treating practitioner, and the other item-related documents. Then they need to electronically file these documents accordingly.

With machine learning, technology can do this work, with the solution essentially becoming the "fax wrangler." This doesn't eliminate the need for people. Rather, you take your really good processors and have them teach the machine what it needs to know and then have these people manage the machine and ensure the work is completed appropriately.

In a mid-sized company consulting engagement last year, one of the tasks I was charged with was coming up with a way to make more consistent use of their people. To do so, we centralized various responsibilities. For example, we created a centralized phone team. That was step one, and a valuable step that will help achieve consistency. What I find fascinating is a next step where the company would investigate how the use of machine learning may be able to reassign people on that phone team.

Let's say this phone team receives frequent questions about the status of a new order. Machine learning (also referred to as "digital experience" by some) should be able to proactively automate a text message to patients that confirms receipt of the order from their doctor, stating an update will follow within 48 hours. While this won't eliminate all calls about new orders, it should greatly reduce the number of calls that come in for order status and thus the number of people who need to answer these calls. In cases where automation is employed, companies have been able to reduce the number of inbound calls for order status by 75% or more.

The best places to start looking at where you should first work to incorporate machine learning are those aspects of your operations requiring the most human resource time, which are likely some of your largest cost centers. Once you've identified these pain point areas, determine what opportunities exist to introduce automation and eventually add machine learning to power this automation. This undertaking is one way to create a much easier and more consistent landscape for a mid-sized company to grow to the next level.

Large Companies

Now let’s discuss our final group: large companies with revenue greater than $100 million. These are businesses that are moving from being a regional player to a national player or a regional player moving into a new region. This growth is complicated because it often occurs through acquisitions, so now you are looking at melding different companies together. These companies have their own way of running their operations, with leaders who have had roles defined based on needs, personality, and demographics of a company. Following the acquisition, these leaders and managers are now being told that the way they have worked and the work they have done will need to change. Those can require difficult conversations and difficult changes.

What a large company needs to do is essentially look at each of the processes for the various companies now part of the larger entity and determine which ones perform the strongest and where large holes exist that need to be filled. For example, let's consider a company that has one contract that does not allow offshore billing and one contract that permits it. The company will want to look within its expanded operations to identify individuals who can champion these distinct efforts. Maybe Susie's company in Kentucky had a fantastic offshore company partner achieving great results. You might want to use Susie and her experience to champion the offshore billing efforts. For payers that do not permit offshore billing, you might find that Bobby's company in Rhode Island had impressive in-house billing performance, so he would champion that effort for the organization.

In larger companies, you typically have defined centers of excellence based on product mix and payer mix within each product. For example, you may have a large HME company with a center of excellence for urological and ostomy supplies and a separate center of excellence for CPAP and CPAP supplies. These centers of excellence are formed by larger companies dividing up the companies they've acquired first by their strengths (in revenue and collections), second by payer (contracts) that dictate how they are going to run their business, and third by product mix.

This brings me to a large client example and how this mindset would play out. One of my large clients recently finished a significant sized acquisition. But the post-acquisition transition is not going as well as they had hoped. Timely payments aren't as seamless as they had been previously because the companies haven't been merged well yet. People who are doing day-to-day work have been tasked with trying to merge the companies, but the work is just too much, and these people cannot focus on their daily tasks and simultaneously handle the merger tasks.

One recommendation for this large company is to assemble a dedicated mergers and acquisition transition team. If this large company is going to continue to pursue acquisitions, which I believe it will, now the company will have a dedicated team to handle merger-related functions, which would include creating centers of excellence.

An important caveat to using a transition team is the need to stay nimble and consider when growing the team would be worthwhile. Perhaps an acquisition necessitates the merging of software. If your transition team lacks a specialist in merging software, you will want to find this talent and add it to the team or use an outside contractor with this specific experience.

Once you have completed a merger, then a large company should further evaluate processes and determine what changes will help it get the biggest return on investment (ROI) based on payers and product mix. Do this by evaluating the best practices of each of the merged companies, including the original company, and determine the ROI from there.

Key Takeaways

I've covered a lot of information here, so I want to conclude by summarizing what I think are some of the key takeaways. For small companies, you must understand the nuances of going from ma and pa to the next stage where you are not and cannot be everything to everybody anymore. You must decide what you want to be "when you grow up." You still need to have a local feel, but inside your operation, your guts must be run much more efficiently.

When you get to the mid-size level, you need to rely on software to scale your company and find those people who will champion this cause. When you have the right people managing the optimal solutions that introduce automation, you will still be able to deliver an exceptional customer experience and achieve success. Lean on your heavy hitters when scaling your capabilities through automation and machine learning.

Finally, when you become a large company and are on an acquisition trail or you have completed an acquisition, you must understand which of the companies is better at payer and product mix integration. Then you must look at how you're going to fit in together as one team. A transition team that can effectively prioritize getting two distinct businesses combined will greatly help in that cause.

Regardless of your size, stay focused on your core competencies and best practices, then plan ahead and pivot as necessary to continue to flourish and profit in the ever-changing healthcare landscape.

Miriam Lieber President, Lieber Consulting LLC

Miriam Lieber is a principal consultant and trainer specializing in home healthcare revenue cycle management. Her extensive experience with Medicare and other third-party payers has brought her national recognition in the homecare industry. With over 25 years in the homecare field, Miriam has consulted with over 500 HME companies nationwide and is a featured author of many articles in the areas of operations management and leadership. She is also a nationally known speaker for many homecare trade associations. She can be reached at 818-692-1626.

Volume 11, Issue 7, April 9, 2024

By: David Purinton

If you own a healthcare company, you are probably receiving inquiries from interested buyers. We view this as buyers marketing themselves to you. At VERTESS, we emphasize the importance of clients marketing their company to buyers as a key step in securing the eventual right buyer and partner.

With potential buyers coming and marketing to you, why should you put in the time and effort to market to potential buyers?

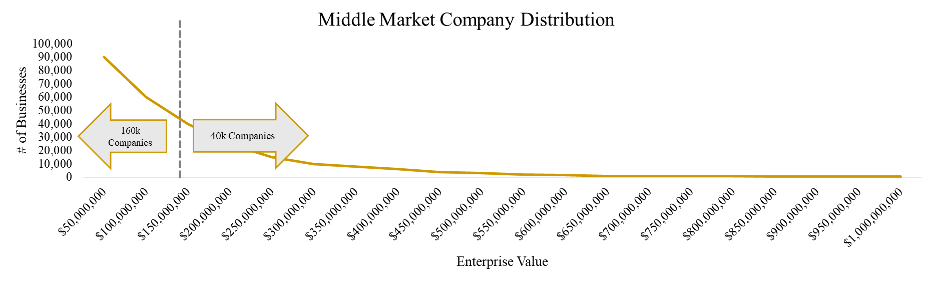

To answer this question, it's helpful to take a step back and understand the current market for sellers and buyers, specifically focusing on the lower middle market. This market has the vast majority of operating companies since most companies have under $150 million in enterprise value, as the following chart represents:

Given the volume of potential targets, there are more investors in the lower middle market than you can probably imagine. The role of these investors (i.e., buyers) is generally to acquire founder-owned companies, professionalize them, scale them organically and inorganically, integrate them, and then sell the larger entity to the next investor. The acquired company scales up as it passes through the hands of various investors.

These investors are financially motivated to market themselves as the appropriate buyer for your company. After all, they stand to make millions of dollars when their acquisition and subsequent growth and transaction strategies succeed. They're aggressively trying to find companies to buy and then execute these strategies.

Buyers view their outreach efforts as a sales cycle. They reach out to X number of business owners, hope that Y number of business owners will engage in discussions about selling their companies, and then the buyers weed out the companies they don't want to own, ultimately acquiring Z. In this sales cycle, buyers are essentially in control.

Owners who market to potential buyers take control of the sales cycle — one that's very similar to the cycle executed by buyers. Owners, usually supported by healthcare M+A advisors like those at VERTESS, reach out to X number of potential buyers and hope that Y number of buyers will engage in discussions about buying the company. Owners and their M+A advisors then weed out the buyers the owners don't want to sell to. The remaining options are engaged in discussions about the potential acquisition, ultimately concluding with the owner signing an agreement with Z.

The Value of Control

Putting the power on your side of the equation matters. Consider the following reasons:

More likely to find the right fit. There are several thousand healthcare investors. Not everyone is going to be a good fit for your company. In fact, most will not. Similarly, a random buyer is not likely to magically be the right fit for you. When you control who you market your company to, you are more likely to market toward companies perceived as potential good fits.

Investors will know you're ready to sell if you're marketing to them. This increases interest and reduces risk. When buyers find potential targets by marketing to companies, the investors usually do not know how willing a seller is to sign a contract. Given the costs of due diligence, that lack of knowledge presents a six- or seven-figure risk.

However, when an owner markets to buyers, investors feel more comfortable spending money in due diligence since they know the owner is more likely to sign the contract at the end of the process. The appearance of an owner interested in at least considering a sale attracts a greater number of investors.

Likelihood of better results. When you can identify multiple potential buyers who might be a good fit for your company, you put yourself in a position to leverage the interest in your asset to negotiate up valuation and terms. You cannot do this without leverage, as buyers aren't interested in spending more money to acquire your business unless they have competition — and competition perceived as legitimate and strong.

Tips for Buyers

While we understand the strategy, we respectfully ask that you stop showing premium valuations in your letters of intent (LOI) to unrepresented sellers. You may not see it as a bait-and-switch tactic, but that's exactly what the seller experiences, and they leave the process believing the initial offer is still achievable with someone else. Even if re-trading has worked for you in the past, this is the kind of tactic that makes sellers skeptical of any buyer.

If you're looking for off-market deals, be prepared for the time and effort required to achieve a discount. First and foremost, develop the relationship before discussing valuation. If the seller asks for an indication of value too soon, you probably know it's not going to the finish line. Cut bait and move on until you find a potential seller willing to spend time forming a relationship with you that can eventually be leveraged into a sale.

If you haven't already done so, create a pre-LOI request list and open a data room. You should have about 75% confidence in a deal before signing an LOI. Submit an LOI that you would submit to an M+A advisory firm like VERTESS. Start with a cash deal you're prepared to execute, then add structure if there's a valuation gap. It's difficult to re-trade down.

Meet With Me at TCIV

I'll be attending TCIV East in Palm Beach Gardens, Florida, from April 15–17. If you will be attending this conference and are interested in meeting up to discuss the topics covered in this column or any other issue concerning M+A, please reach out to me using my contact information below.

Here to Help

If you're an owner thinking about selling, contact the M+A team at VERTESS. We're specialized healthcare advisors who help our clients with exit planning and executing that plan, including marketing directly to those buyers likely to be a good fit for your company and serious about executing an acquisition. We'll help you determine the right path forward for the sale of your business and then do much of the heavy lifting that typically ends with a successful transaction.

David Purinton MBA, CM&AA

After working in M+A advisory and corporate financial consulting, I was fortunate to co-found Spero Recovery, a provider of drug and alcohol recovery services with over 100 beds in its continuum of residential, outpatient, and sober living care. As its CFO I led the company to significant revenue and margin growth while ensuring it adhered to the strictest principles of integrity and client care. After selling Spero I remained in leadership with the buyer as its CFO and quickly realized accretion and integration. Of the myriad lessons not learned while earning my MBA with Distinction in Finance from a Tier 1 university, the most profound was the importance of investing in my staff and clients. I learned that the numbers on a spreadsheet represent humans, families, and dreams, which was a radically different paradigm from investment banking.

At VERTESS I am a Managing Director providing M+A and consulting services to the Behavioral Health, Substance Use Disorder treatment, and other verticals, where I bring a foundation of financial expertise with the value-add of humanness and care for the business owners I am honored to represent.

We can help you with more information on this and related topics. Contact us today!

We will occasionally hear from the owner of a healthcare company something along the lines of the following: "I know someone who just sold their [type of healthcare business] with the help of a business broker. What's the difference between working with a broker and an advisor like you?"

In this column, I will strive to answer this question, which should also help you understand why working with a healthcare M+A advisor is likely to be in your best interest when you determine it's time to sell your company. I'll start by providing some background information on a typical business broker who works in the healthcare space and instances where the role's deliverables may overlap with that of an M+A advisor. Then I will provide further information on what you can expect from working with a healthcare M+A advisor and how this experience is likely to lead to more successful sales.

Role of a business broker

A business broker facilitates the buying or selling of a business. This individual can either represent the buyer or seller in a transaction. The same can be said of a healthcare M+A advisor. Both brokers and advisors can act as intermediaries between buyers and sellers. Both will privately negotiate deals, and both will help with the transfer of ownership of a business to complete a transaction.

That largely defines the role of a broker: making introductions between buyers and sellers, helping with negotiating deals, and aiding in the transfer of ownership. Payment to a broker is typically a pre-established commission contingent about the completion of a transaction.

What is also important to know about most brokers is they tend to serve a wide range of clients operating in a wide range of industries. It's not unusual for a broker to be involved in healthcare transactions as well as those in manufacturing, software, construction, electronics … the list can go on. Brokers can be the jack of many transaction trades and help with many successful transactions. But as a result, they may not build up significant experience and knowledge of a single vertical.

Role of a healthcare M+A advisor

Now let's break down what a healthcare M+A advisor offers to the seller or buyer of a healthcare company. Note: To help with readability, I will focus on what an advisor offers to a seller.

Active from start to finish — and beyond. A healthcare M+A advisor is more of a partner throughout the entire transaction experience, and then some. They are active in the sale process from the initial valuation of a company, through all the extensive work that follows leading up to a company coming on the market, through the bringing in and reviewing of prospective buyers, and through the transfer of ownership. They can advise on any part of the transaction, including valuation, financial, and legal requirements, and help bring on other team members who can assist further in these areas. An M+A advisor will also stay involved after completion of the transaction to help ensure the transfer of ownership is successful and sellers receive any necessary post-close support.

Advisors manage the entire M+A process for a seller, making sure all the boxes needed for a successful transaction are checked (and double-checked). This management helps reduce the likelihood that a critical step is overlooked or not completed properly.

Management by the advisor also enables owners to focus much of their time on the running and needs of their business. Transactions usually take at least several months and sometimes much longer. During this period, it is essential that the business continues to operate as usual. If an owner must allocate extensive time to the M+A process, this increases the risk of harm to the operations and bottom line, and thus the potential sale and sale price. A healthcare M+A advisor who handles the heavy lifting greatly reduces this risk.

Experts in the field. Healthcare M+A advisors tend to be experts in their healthcare field and generally do not work outside of that vertical. They often become advisors after owning and/or operating healthcare businesses in that vertical. This expertise and experience helps a seller and the execution of a successful transaction in many ways.

Communication between advisor and seller tends to go more smoothly since they can speak "the same language." The advisor is also able to identify opportunities for improvement more effectively. Following completion of a valuation, an advisor will discuss the positives and negatives about the business that are affecting the valuation and the avenues that exist to increase the valuation or help a seller hopefully receive an offer on the high end of the valuation. These may be changes or fixes a seller should consider or worthwhile growth initiatives to pursue.

These pre-listing efforts can help ensure the business is in a better position to attract multiple buyers willing to offer higher prices when the company comes to market. This contrasts with a broker, who will generally list a company as soon as they are engaged by a seller.

Larger geography. Healthcare M+A advisors tend to have national and global experience whereas brokers often work in a narrower geography. Broader geographic experience often enables advisors to better understand more of the trends and developments affecting the vertical they serve and attract more potential buyers to a sale of their client's business.

Paid as a percentage of payout. Advisors are generally paid a retainer fee and then a percentage of the total payout (sale price), with the bulk of the payment coming from the payout. This financial model serves as motivation for an advisor to help a seller undertake initiatives that can help increase the sale price. While money is important, the experience an advisor has in the vertical can also serve to help a seller identify the buyer that not only makes a good, fair offer, but is also the right fit for the future of the business — someone who can preserve the company's legacy, maintain high staff and client satisfaction, and preserve other qualities like culture that have come to define the business.

Making a Sound Business Decision for Your Business

A seller typically sells one business in their lifetime. While a broker can help you sell your company, a healthcare M+A advisor may be in a better position to help you sell your company the best way possible. By working with an advisor, you will put yourself in a strong position to make a deal that is the right deal — one you can walk away from feeling like you have passed your business along to the right company and with a payout that reflects the many years of blood, sweat, and tears you put into the company.

At VERTESS, each Managing Director focuses on specific healthcare verticals and brings insights into the ways deal structures should be created for the companies they serve. Please reach out if you have questions about what our team of advisors can do for you or any other matter concerning the future of your business.

Alan Hymowitz CM&AA

During the past decade I have facilitated numerous, diverse M+A transactions in the pharmacy marketplace across the country, as well as providing strategic consultation to national pharmacies and similar organizations. Prior to becoming an M+A advisor, I was a “hands on” owner and manager in the pharmacy and home infusion healthcare marketplace for over 15 years, and successfully sold my pharmacy to a national company after growing and diversifying our income streams in a very competitive market. My specialties in the pharmacy and home infusion marketplace include long term care, retail pharmacy, specialty pharmacy, and home healthcare, and I have attained the URAC Accreditation and Specialty Pharmacy Consultant designations, in addition to other recognition. My educational background includes a Bachelor of Arts from Rutgers University and a Master of Arts from the John Jay College of Criminal Justice.

We can help you with more information on this and related topics. Contact us today!

Want to stay current with trends in the medical/healthcare space as well as receive expert advice of veteran medical entrepreneurs?

SUBSCRIBE TO OUR BI-WEEKLY NEWSLETTER VERTESSPRESS

For over 10 years, we've been teaching ways you can improve the value of your healthcare company, focusing on informing you about mergers + acquisitions, including M+A trends in the healthcare market.