In recent years, we have seen healthcare information technology (IT) companies emerge as a leading investment focus for private equity. Healthcare IT has showcased resilience and steady growth even as other healthcare sectors, like healthcare services, faced evolving regulatory challenges. While Healthcare IT faces its own set of regulatory hurdles — especially around data security, interoperability, and compliance — these differ from the direct care and reimbursement complexities that healthcare services providers confront.

As owners of healthcare IT companies consider their strategic plans for 2025, I believe they have a unique opportunity to consider lucrative exit strategies and other mergers and acquisitions (M&A) opportunities, driven by strong and rising interest from investors who recognize the substantial value of digital transformation in healthcare.

Why Buyers Are Targeting Healthcare IT Businesses

The interest in healthcare IT companies from private equity firms and others stems from the long-term customer relationships and "stickiness" of software platforms, especially in mission-critical areas like revenue cycle management (RCM), quality of care, and provider productivity applications. The ongoing digital transformation in healthcare, coupled with a rising demand for analytics and interoperability, positions healthcare IT companies as high-value targets with scalable revenue potential.

Historically, the lower-middle market in healthcare IT was less attractive to private equity due to the dominance of venture capital investors and a focus on growth at all costs over profitability. However, as fundraising becomes more challenging, companies are shifting to scale with profitability in mind, aiming for cash-flow-positive models. We have seen this shift spur a rise in venture-backed, lower-middle-market software transactions, creating new M&A opportunities for companies that previously had limited exit and partnership options.

Attractive sectors in healthcare IT include RCM, predictive analytics, value-based care, and niche-focused healthcare solutions. RCM platforms are among the most sought-after targets, with significant deal flow driven by the outsourcing of complex billing and coding tasks. Despite some consolidation in recent years, this market remains highly fragmented, offering further consolidation opportunities for private equity, while the long-term relationships these platforms foster enhance scalability and investment appeal.

With the rise of value-based care, platforms centered on financial efficiency, data-driven decision-making, and outcome improvement — such as clinical analytics, care coordination, remote patient monitoring (RPM), and point-of-care decision support tools — are experiencing elevated activity. Tools leveraging artificial intelligence (AI), machine learning, and real-time data integration are particularly scalable across various healthcare settings, making them especially attractive to investors.

Software products focused on specific niches within healthcare are also drawing premium valuations due to their high demand. With barriers to entry and limited competition, these specialized products often establish moats through customer retention and long-term contracts, making them ideal tuck-in acquisitions for larger platforms. Examples include ambulatory electronic health record (EHR) and practice management solutions tailored to specialties like dermatology and ophthalmology, which offer highly specific workflows and patient engagement tools that drive operational efficiency and improved outcomes. Products focused on chronic disease management, such as hypertension- and diabetes-focused RPM, also align well with value-based care models.

Why This Matters for Healthcare IT Business Owners

Private equity interest in healthcare IT companies is driving higher valuations, especially in the sectors outlined above, enabling many owners to achieve attractive multiples when they bring their company to market. Selling to investors that understand the strategic value of specialized software allows for smoother integration into larger platforms, enhancing scalability and impact. Owners can also benefit from flexible exit options, including minority buyouts, majority recapitalizations, earnouts, equity rollovers, and ongoing roles within the acquiring platform, offering various paths to a successful transition.

For Healthcare IT business owners considering a future sale, taking steps now to strengthen and streamline operations can lead to a more attractive valuation and smoother transaction process. Start by ensuring that financial records and key performance indicators (KPIs) are transparent, accurate, and readily accessible. Clear visibility into revenue streams, customer retention rates, and cost structures is essential for attracting potential buyers.

Additionally, focus on reinforcing your platform's scalability and interoperability to align with industry demands for flexible, integrative solutions — features highly valued by private equity and strategic investors. It's also wise to address regulatory compliance proactively, particularly around data security and interoperability standards, as these are increasingly scrutinized in due diligence.

Finally, consider solidifying long-term contracts and deepening relationships with clients. Long-term customer retention enhances the perceived stability and profitability of the business. By preparing these elements now, you'll be well-positioned to capitalize on the favorable market trends when the right opportunity arises.

Maximizing Value in Healthcare IT M&A: Why Founders and CEOs Should Trust VERTESS

At VERTESS, we bring unparalleled expertise and a deep understanding of the healthcare IT sector to every M&A engagement, helping clients achieve the highest possible valuation and a smooth, successful exit. Selling a business is more than just a transaction — it's the culmination of years of hard work and growth. We recognize these efforts and take a personalized approach to transaction engagements, working closely with each client to understand their goals and develop a strategy that highlights the unique value of their company. Our process begins by identifying the ideal target buyer groups, whether they are private equity firms, strategic acquirers, or other specialized investors. With our extensive network, we connect owners with buyers who appreciate the strategic value of their business and are invested in maximizing its future growth potential.

We also excel in crafting a compelling narrative that showcases each company's strengths. By collaborating with clients to emphasize scalability, revenue potential, and competitive advantages, we ensure their business stands out in a crowded market and attracts top-tier buyers. From structuring the deal to navigating due diligence and handling negotiations, VERTESS provides comprehensive support at every step, anticipating and addressing potential challenges to keep the process on track. Our expertise ensures that every detail is managed with precision and care, giving clients the confidence that they're positioned for success.

With private equity attention intensifying and valuations on the rise, now is an ideal time for healthcare IT business owners to consider their exit options. Partnering with seasoned advisors like VERTESS can simplify the M&A process and unlock the full potential of an exit. This will help ensure owners are well-positioned to capitalize on today's healthcare IT market opportunities while preserving the legacy of their healthcare IT businesses.

Jack Turgeon, MBA

As a Director at VERTESS, I bring extensive experience in sales, consulting, and project management from early-stage startups. With an MBA from Babson College, I have a strong foundation in business strategy, operations, and financial analysis. My personal connection to behavioral healthcare through a family member motivates me to help business owners get the best deal possible while ensuring high-quality care for their clients. Throughout the M&A process, I provide comprehensive support at every step. I have a proven track record in negotiations and client management after working with companies in various industries. I’m excited to join VERTESS and make a meaningful impact on the lives of the owners I work with.

We can help you with more information on this and related topics. Contact us today!

In the business world, the concept of the "second bite of the apple" refers to a business owner retaining some ownership of their company (i.e., rollover equity) following a sale to a strategic partner and then the owner earning another payment when the strategic partner sells the company. Thus, the mergers and acquisitions (M&A) meaning of the "first bite of the apple" is when the owner initially sells the majority of their company to a strategic partner.

However, I would argue that defining the bites of the apple in this manner overlooks a lot of the details of the owner's journey to this point in the life of their business. Another way to look at these bites is that the first bite of the apple occurs when an owner starts their business. This bite can be bittersweet. It involves joy, worry, sadness, and the many difficulties that business owners typically will experience and endure on their ownership journey. The second bite of the apple is when the owner capitalizes on their hard work through a sale, leading to a more comfortable retirement or enabling the owner to pursue another venture — all because of the effort and hard work that went into building a successful first company.

To capitalize on the metaphors described and maximize the enjoyment of the second bite of the apple requires getting the first bite right. When starting a business, there are a number of decisions an owner will need to make outside of determining what services the company will provide. Let's look more closely at a few of the most important ones and what new business owners need to know about them. Note: While missteps concerning these decisions are not uncommon, owners that recognize and address their mistakes can better ensure their second bite is as sweet as it can be.

Debt

All new businesses take on debt. Be precise and strategic about how you take on this debt. Ensure the debt does not over leverage your business and can be paid even if revenue declines due to normal deviations. You do not want to compromise your ability to maintain credit and compromise your working capital. To elaborate further, if you rent a building or office space, one of the most important considerations is whether the cost fits your business model of expenses versus revenue.

When it becomes time to expand your company, do not overextend yourself financially. Follow the original expenses versus revenue model and ensure expenses remain an appropriate percentage of tracked revenue.

Accounting practices

Accounting practices are key to a successful business. Most new businesses may use some type of internal accounting process via QuickBooks and/or utilization of an office manager. Most businesses will also need to contract outside accounting services to track taxes, payroll, and other expenses. Maximizing tax deductions is important for a new business. Hiring the right accounting firm will ensure you properly track and document monthly profit and loss (P&L) and receive ongoing, proper counsel. Advice can include the best methods to save on taxes and track progress accurately. The ability to present accurate, complete data is important if you are audited by the IRS — and when it eventually becomes time to sell your business.

Clean financials are key to surviving buyer due diligence during an acquisition, and they are an essential element of a buyer defining your business attractive and a worthy investment. If cleaning up your financials requires too much work, this will turn many buyers away.

Personnel

One of the most important — if not the most important — steps business owners must take is hiring personnel. Owners need to find the right personnel and maintain strong employee relationships throughout the journey of running the business.

While one would hope that employees will be as devoted to a business and its success as an owner, achieving this is often unrealistic. Owners have much more to gain and lose. But owners will still want to work to develop employee loyalty to the company, which requires keeping employees engaged, excited to come to work every day, and feeling like they are part of something bigger than themselves.

Achieving these goals starts with transparency. Share the company's ongoing progress — good and bad — with employees. That means not just bring up performance when sales are down.

Make employees a bigger part of the business. Profit sharing is one great way to do so. It better ensures transparency, and when revenue grows, employees directly feel the impact of their work and the company's success beyond receiving a regular paycheck. ESOP companies — those with an employee stock ownership plan — have been extremely successful for this very reason.

Profit sharing also promotes tenure, which is extremely important in keeping quality staff for the long term. The better staff understand the business, the better they will be at performing their work and supporting the business and its growth.

Impacts on a Transaction

The decisions you make concerning debt, accounting, and personnel are just as critical to the start of your company as they are to its end when ownership is transferred. Let's jump to the moment where you're looking to sell your business or find a strategic partner. The first step you will want to take is to highlight your business performance. Owners often get focused on the products or services they provide and the value and benefits these deliver to consumers. However, if your business model and structure are not solid, a buyer is not going to want to acquire your company, or you will not receive what you believe to be a fair offer.

It's important to know that most transactions are debt free. Any debt you have, whether it be tied into your real estate, fleet, renovations, expansion projects, or any other area of operations, will be deducted from the purchase price. Some debt is not necessarily bad, but if it's based on risk and not normal working liabilities, you will be at a financial loss.

If your bookkeeping is not clean, you can expect a difficult transaction process and one that may never reach the finish line. Clean bookkeeping is not about the minimum you can get away with when filing your taxes. It's about convincing a buyer that your business is the perfect acquisition opportunity — one worthy of an investment and one that can be scaled appropriately so the strategic company or private equity investors will generate a return on the investment.

The most crucial test of whether you have achieved clean bookkeeping comes when you go under a letter of intent and the buyer starts the quality of earnings (QofE) report, which is performed by a third party. A QofE is always the immediate telltale on how appropriately you have run your business. For any business that keeps good bookkeeping, with invoices that can be matched with revenue, expenditures at what the market would expect, and no large list of add backs and personal expenses rolled into the company, the QofE should align with your true revenue, often described as adjusted 12-month trailing EBITDA. What is often revealed through a QofE is a reduction in EBITDA, with the third party determining problems with your true revenue. This risk is why it's imperative for business owners to have a proven accounting team handling a company's financials throughout the life of the company.

Finally, personnel is often a company's most valuable commodity. It is not only important to have a well-trained and loyal employee base, but you will want a second, third, and sometimes fourth person in command or capable of assuming command when transitioning ownership. If an owner wants to stay on board and roll over equity post-acquisition, then the number two or three person in charge may not be as important to a buyer. However, if an owner is looking to take a reduced role in the company or completely sell the company and step away, the owner is going to need to prove that the next people in the chain of command know as much about the business as the owner does and will remain just as committed to the business following completion of the transaction.

Find the key leaders in your organization. Teach them the business until you are at a place where you know you can go on vacation for weeks at a time and not need to worry about how the daily operations will run because you have full confidence in the people you have appointed to oversee the company in your absence. If you successfully reach this point, it will be easier to demonstrate to buyers that you have worked for many years to prepare for the transition of oversight and management and are confident that it has reached a level where you can step aside.

The Time to Think About the Value of Your Company Is Always

Many people do not think about the value of their business until they think about selling the company. But the value of your business will be predicated by how well you have run your business throughout its many years of operations.

While it may seem counterintuitive, you should think about the value of your company starting the day you launch your business and then never stop. Best practices, like those highlighted earlier, should be top of mind throughout your entire ownership journey. Otherwise, when you finally decide to pursue a transaction, you will likely find yourself spending a lot of time and money trying to clean up existing processes. Even if you are successful in cleaning these processes, a buyer will likely determine that the consistency you are hoping to show is deceiving. This can cost you offers and the value of offers, but it's simple to avoid if you start on the right track from day one (or as close to this as possible).

Speaking of value, how would an owner know the right time to maximize on that value through a transaction? The best time to sell a business or find a strategic partner is when the business is running on all cylinders. However, when business is performing great, this is usually when an owner thinks the least about selling. It's the time of ownership where running the company is perhaps the most fun, in part because of the tremendous profits. Why would an owner want to share this with anyone else (besides employees)?

To answer this question, look at the scenario from a buyer's perspective. A buyer will see the most value in a business when everything is clicking — margins are great, employees are happy, and there is plenty of current and future business. The worst time to try sell your business is when performance starts going downhill or when you are ready to retire and are unable or unwilling to be part of the next chapter of the company after it has been acquired. While the buyer may not want you to remain involved, many buyers like the option of keeping an owner engaged for at least a short period of time to maintain some continuity and help ensure a smoother transition.

By selling your business at the height of its performance, this will essentially guarantee you the best valuation multiple and will help you get through the acquisition process, which can take many months during which there may be some peaks and valleys in the financials. If you are already maximizing revenue when you decide to launch your sale, you should be able to weather any storms.

To help you get to the finish line that you want for your company, hire an experienced M&A firm familiar with your type of business. As your M&A advisor oversees the creation of your company's confidential information memorandum (CIM) and completion of its financial analysis, they will identify any inconsistencies and irregularities that may have occurred in your business. With this information, your advisor will help you determine what you need to do to address these potential red flags or ensure you explain these issues early in the transaction process. Being upfront demonstrates your commitment to full transparency with prospective buyers and will help you avoid having any "skeletons" in your closet discovered during due diligence.

If you have questions about anything in this column, want to learn whether the time is right for your company to consider sale, are interested in finding out more about the transaction process, or are interested in discussing anything else concerning the future of your company, reach out to our team of expert healthcare M&A advisors at VERTESS. We'd love to hear from you!

J. Blake Peart, RRT, CM&AA

I have had the opportunity of an extensive and diverse career in healthcare for over twenty years. In the past ten years, I have served as CEO for multiple hospitals of Fortune 500 companies and CEO for several large Ambulatory Surgery Centers. In addition, my operations and business development knowledge has allowed me to experience the entire M&A process from start to finish focusing primarily on private equity transactions. My history as both a CEO and clinician provides a unique perspective based on years of experience and empathy when working with business owners seeking M&A advice. My expertise is in Ambulatory Surgery Centers, Physician Practices, and independent hospital businesses. I am here to support healthcare business owners who select the M&A direction as one who has walked in their shoes. I know that every transaction is unique and tailored to a seller’s need in getting the best deal and providing a positive experience throughout the entire process.

We can help you with more information on this and related topics. Contact us today!

There's the expression, "You never get a second chance to make a first impression." For many healthcare business owners thinking about selling their company, the first impression they may personally make on prospective buyers will come from a confidential information memorandum (CIM). If that CIM doesn't represent the business in a professional, positive, and transparent manner, the owner may not get a chance to receive a fair offer.

What exactly is a CIM? It's the confidential document used to market a healthcare business to potential buyers. It may go by other names, including a pitch deck, investor deck, the "book," or confidential information presentation (CIP). The marketing document is typically called a CIM when used in the sale of a mature healthcare businesses and a pitch deck for healthcare startups.

While the name is interchangeable, the content is not. A CIM is the initial source of data and information a buyer uses to evaluate the candidacy of an investment target relative to its investment thesis. Broadly speaking, the CIM explains what the business does and the type of transaction the owners are seeking.

Most business owners do not create a CIM until they are prepared to actively market their business for a sale. However, if an unsolicited buyer takes interest in your company, immediate signals are sent if you do not have a CIM, let alone one that's current: You're unprepared for a sale, and the buyer is in a good position to negotiate a value deal. At least those are the signals potential buyers receive, regardless of whether they're true. Simply responding to interested buyers with an annually updated CIM signals a posture toward prospective buyers that you are not interested in a low-ball offer.

On the other hand, if you intend to execute a coordinated, professional healthcare M&A process to sell your business, a CIM is required. You will be marketing your business to dozens — if not hundreds — of potential buyers, many of whom analyze numerous potential acquisitions each week. Without the data about your healthcare business consolidated in a professional manner, buyers are much less likely to invest the time into understanding your company's raw information. Note: Marketing your healthcare company is essential to finding the right buyer and securing a fair price for your business, which I previously discussed in this column.

Moreover, organizing and presenting the data allows you to structure the narrative in ways that emphasize your company's strengths while providing explanation on any potential weaknesses. You can tell your story to potential buyers in ways that benefit you as opposed to allowing a buyer to "discover" the hair — the operational, legal, financial, or other aspects of the business that have had errors, inefficiencies, or other liabilities — and speculating on any other skeletons that could be in your closet.

This column takes a closer look at the importance and development of a CIM is written for two audiences: 1) sellers who are hiring a professional healthcare M&A advisor, like VERTESS, to help them proceed with a sale and develop a supporting CIM or to double check that their current advisor included the relevant, key points in the CIM and 2) owners who endeavor to manage the sale of their business without a professional M&A advisor (not advisable) and therefore need tips and best practices to create an impactful CIM.

Confidential Information Memorandum Best Practices

Let's take a look at a few general CIM best practices before we discuss key components of a well-rounded CIM.

First, do not use a Word or similar document to create your CIM. Nobody wants to open up a CIM and be greeted by a wall of text — even a wall that has an occasional chart or image dropped in. Buyers review hundreds of CIMs, so the last thing you want to do is have a CIM that makes a negative first impression (remember what I said in the first paragraph). Make your CIM simple, nice to look at, and easy to review and digest. Include graphics, charts, and pictures, and present them in an attractive layout. This is best achieved using software like Microsoft PowerPoint.

Second, don't exaggerate or attempt to mislead a reader. An investor competent enough to buy your company is also competent enough to eventually learn the truth about your company. Be as honest as possible in the CIM. That's what buyers are expecting.

Third, and this goes back to the purpose of the CIM: Keep it concise. This means around 40 pages, although fewer is fine if that's what's required to effectively tell your story. If you feel compelled to create a CIM that's longer than 40 pages, you should feel that those "extra" pages are absolutely essential to better positioning your company in a competitive landscape.

After sending a CIM to potential buyers, you will find many will respond with additional questions deriving from their specific investment thesis. You can't try to get ahead of every question as questions change between differing theses. An industry specialist can help you create a CIM with specific data points that all investors in your vertical will want to understand. Investors will begin analyzing the data, using it in their own models; ask questions relating to their own thesis; and, if they feel like there could be an interesting opportunity, they will set up a "coffee meeting." This meeting gets final questions out of the way. When using a healthcare M&A advisor, the coffee meeting isn't something you should need to do as the seller.

From here, a potential buyer should have the preponderance of data needed to meet with you, the seller; identify chemistry and synergy; dig deeper into the data; visit your operations (if applicable); and eventually, if all goes well, submit a letter of intent (LOI).

What To Include in Your Healthcare Confidential Information Memorandum

Below we identify some of the core components of a good CIM. There may be reasons to exclude, modify, or expand on this list. Each business is different, and your M&A advisor should know what is most important to include in your CIM, assuming your advisor is a specialist in your healthcare industry.

Company overview

The first page of the CIM with meaningful content — usually the overview — gets a fair amount of attention and then most buyers will scroll to the financial section found later in the CIM. If buyers like both pages, they'll go back and read the rest of the document.

In your business overview, summarize the offering in a way any reader (potential buyer) can understand. Define your audience, which is often demographics of end users, the business types you sell to, and/or possibly a job function (i.e., your customers). Show how you solve a problem(s) and explain it in a way that's easy to follow.

The final element to include in your overview is your "secret sauce" — your unique approach to solving the problem with your target audience.

Some quick tips for writing the overview:

Avoid using adjectives like "first," "only," "huge," or "best," which are words that signal inexperience and possibly exaggeration.

Take time to properly define your target audience.

Eliminate buzzwords or jargon.

Keep it concise.

Include the ownership structure, reason(s) for the sale, and details on the desired deal structure, if known.

Company history

When you reflect on the history of your business, you'll probably think about the experience of opening the company, your first customer, the first time you hired and fired someone, your first insurance reimbursement check, a customer experience that went wrong, or a major accolade. Investors want to know about the background of your company, but they are really looking to understand your history through the lens of growth. Help buyers visualize the way your footprint expanded, customers grew, patients diversified, contracts were secured, and staff increased. Include the challenges and risk factors you faced along the way and how you overcame or navigated them.

Remember: A buyer is acquiring your business so they don't need to face all the challenges you encountered and overcame. If they wanted to face those challenges, they would start their own company. Let buyers know how much work it took to grow the company to its current state, even if those growth pains are in your distant memory.

After reading the history, potential buyers should come away with two sentiments: 1) I'm glad I don't have to go through all that effort, and 2) The skill, effort, and luck involved to advance the business to its current state are difficult to reproduce, so it's less risky to buy than build.

Team

Include an organization ("org") chart and explain why your team is qualified to execute your operations better than competitors. Work history, networks, and skills are key points to highlight, as is your history together as a team. This may include how you knew each other before working together.

Resume highlights or short bios are expected. Limit these to your leadership team. While the organization chart may show all the positions (ideally grouped by division or function), investors are most interested in and likely looking to acquire your management team. They want to know the management team that they're acquiring is worth their investment.

Healthcare market

In many healthcare verticals, the market is known or assumed, but potential buyers want to know how big the opportunity is associated with your company. Yes, they may plan to expand your business, but the core market is a starting point, and they want to know that you know it.

Beyond providing a market overview, also provide a clear picture of your audience. What is your market size? Who are they, and how many are in your market? How do you reach/communicate with your audience? What are your referral sources? What is your market position?

When putting together this market analysis, you may decide to share the "total addressable market" (TAM), which includes every potential member of your audience seeking services or products from your business, or you may decide to refine it to your "total serviceable market" (TSM), which are the customers you are able to reach.

Business model

How do you make money? Who pays you, how much, when, and from where? I've seen sellers drop the business model canvas into a pitch, but that may signal inexperience. You should be able to synthesize your business model into a succinct, visual, and possibly creative way where everyone can understand the model.

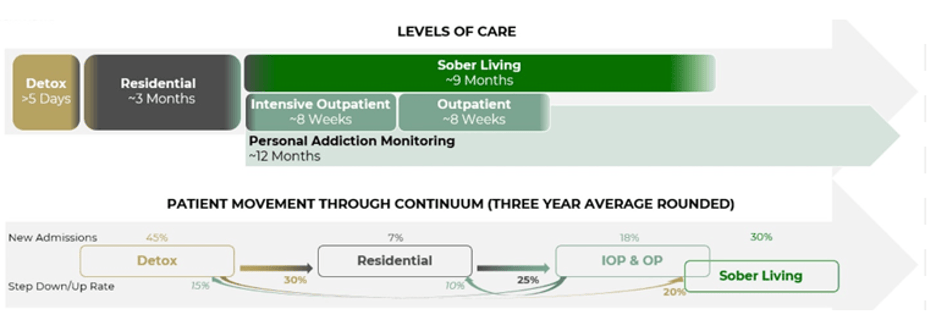

For example, with substance use disorder (SUD) providers, I model the American Society of Addiction Medicine (ASAM) continuum in a visual, then overlay the company's position in the continuum and add relevant data. See an example below. It's a simple visual to depict a client's business model, and even an investor not experienced in the space will understand exactly what the client does, how they're paid, how patients move around the continuum, and some outcome measurements.

Competition

Not all CIMs include information on competition, but I personally like to discuss it. In the SUD/mental health spaces, it's helpful to see the density of providers in a geography since that helps buyers understand in-network reimbursement rates better.

When providing a competitive analysis in the CIM, you do not need to know and/or identify every competitor, but you should have command over the competitors in proximity to your operations. Communicate how they're trying to address the problems you're working to solve and how your solution is similar or different — or whether any difference matters.

If you have a competitive advantage, share it. If your service is similar to your competitors, leave this section out. It may be unnecessary and spur questions you don't want to answer.

Business growth

Buyers deploy capital to generate a return on their investment. How might they generate a higher return on capital with your asset versus another? While you might not receive the "credit" in valuation for future revenues associated with growth (the buyer will need to do the work to achieve that growth, so they're not going to pay for it ahead of time and be accountable to execute it), you'll see increased interest from potential buyers if you can show demonstratable pathways to that growth.

Case studies that highlight a recent initiative and discuss how that initiative and its success can be reproduced is one effective way to demonstrate growth opportunities. In SUD, this may be a new level of care in an existing geography or starting an intensive outpatient program (IOP) to see if there's demand in a new geography before launching a residential treatment center (RTC). In mental health, a case study might speak to marketing to new populations, telehealth, psychedelics, or transcranial magnetic stimulation (TMS). Including data points that give a clear picture of the path toward growth can effectively demonstrate growth potential.

There are areas of low-hanging fruit for growth in most businesses. Even if they seem obvious, explain them. There are also growth initiatives you may have considered but chose not to pursue due to the effort, capital requirements, lack of manpower, lack of expertise, or simply because you were approaching a sale. Put numbers and timelines to these initiatives and offer the buyer a blueprint to a higher return on capital.

You're the expert. Help show it in the CIM. Buyers want to know what you might do to grow first before considering their own plans.

Financial overview

Historical and projected financials are key elements to a CIM. Explain volatility, and defend the proforma. Potential buyers will scrutinize any years where revenue and expense variance were substantial, so it helps to set the narrative for those likely questions in the CIM.

It's best that proformas provide a realistic outlook for the current scope and scale of the business if it is mature or a defensible and conservative outlook for growth initiatives for a newer business or startup. Sellers tend to have a bright outlook for future performance, but buyers know that storms can quickly appear in even the bluest of skies. In other words, your proforma should point "up and to the right" (it would be uncommon for an owner to believe plans will result in declining revenues) but avoid signaling inexperience by including assumptions that paint an unrealistic or overly optimistic growth trajectory.

Make sure the data you've peppered throughout your CIM clearly ties to and is reflected accurately in the proforma. We call this "tick and tie," where advisory teams put a "tick" mark next to every data point in a CIM and "tie" them out to all the other data to ensure everything checks out. If you don't tick and tie your CIM, there's a good chance a buyer will — and if they do, expect them to catch any errors, which will damage your credibility.

Metrics

Not all businesses operate off metrics, which is a travesty. If you have metrics, the key is to compare yours to industry norms. Common metrics in healthcare businesses include prior authorization versus claims collected, census, inventory turnover, and rounding, so you should be able to identify the benchmarks (a healthcare M&A advisor will help with this as well). If you have substantial variance from any benchmarks, you must address the reason(s) why. It's better to have an upfront explanation than to let buyers discover these variances and develop their own narrative for why your business is underperforming.

Creating An Optimal Healthcare Confidential Information Memorandum

Developing an informative and effective healthcare CIM takes time, expertise, comfort with software, and other skills. An experienced M&A advisor will have these skills or a team supporting them with such talents. An advisor will know how to present your company's most important data and what data to omit. An advisor will also know how to pepper the CIM with data points allowing buyside analysts to prepare their own models so they can analyze your business operating in their portfolio or model.

Completing a CIM is possible without an expert M&A advisor but doing so is not without risks. For most business owners, the work required to create a proper CIM is usually difficult to effectively execute while operating and leading the company and do so in a way that creates a limited auction for the company.

Since the CIM is essentially the first true experience, interaction, and impression a potential buyer will have with you and your company, it's likely in your best interests to hire a healthcare M&A advisor and task them with taking the lead on drafting the CIM. This will better help ensure the final document communicates what buyers want to see, positions your business correctly under current market conditions and buyer interests, and gives qualified buyers a starting point for the "coffee meetings."

David Purinton, MBA, CM&AA

After working in M+A advisory and corporate financial consulting, I was fortunate to co-found Spero Recovery, a provider of drug and alcohol recovery services with over 100 beds in its continuum of residential, outpatient, and sober living care. As its CFO I led the company to significant revenue and margin growth while ensuring it adhered to the strictest principles of integrity and client care. After selling Spero I remained in leadership with the buyer as its CFO and quickly realized accretion and integration. Of the myriad lessons not learned while earning my MBA with Distinction in Finance from a Tier 1 university, the most profound was the importance of investing in my staff and clients. I learned that the numbers on a spreadsheet represent humans, families, and dreams, which was a radically different paradigm from investment banking.

At VERTESS I am a Managing Director providing M+A and consulting services to the Behavioral Health, Substance Use Disorder treatment, and other verticals, where I bring a foundation of financial expertise with the value-add of humanness and care for the business owners I am honored to represent.

We can help you with more information on this and related topics. Contact us today!

Many small healthcare business owners struggle when they achieve a certain size or revenue stream. While these owners may see an opportunity to scale, there are challenges: They still have the "mom-and-pop" ideology (i.e., small company mentality) and their organization is not ready or capable of scaling up.

This can be a frustrating experience for an owner. They feel their company can do so much more business, yet they lack the capital, know-how, technology, and/or experience to transform their healthcare organization from a small business (e.g., $20 million in revenue) business to a much larger business (e.g., $100 million in revenue).

Such a situation is risky for a healthcare business owner. If the owner attempts but struggles to grow the revenue and/or EBITDA of the company, this could greatly devalue the business in just a few years. But that doesn't mean owners should abandon their vision for growth. Rather, they may want to explore a sale or recapitalization.

By pursuing one of these options, owners can accomplish a few worthwhile goals. They can get a nice, first "bite of the apple" for their business. They reduce their financial risk by no longer having so much of their finances in one basket. If they stay involved with the company as either a CEO or board member, they can work with a financial or strategic buyer with the experience and resources to scale and accelerate growth. This collaboration can make achieving growth goals possible and do so in much less time than if the owner attempted to achieve such growth on their own. If growth is successful, the owner and existing (or new) management team would be able to get a second — and likely much bigger — bite of the apple and then cash out with the right rollover or stock incentives.

7 Steps to Achieving an Ideal Healthcare Transaction

If proceeding with a sale or recapitalization sounds like a good plan for your business, follow these seven steps to help find the right buyer and partner who can help you take your healthcare company to a much higher level.

1. Set your healthcare transaction goals

Take time to determine the goals for the transaction you're considering. Make goals lofty but achievable. To accomplish the latter, put together a supporting team that will provide the backing and expertise you need to develop an optimal plan for moving forward. This team should be comprised of key internal executive leaders, such as the chief operations officer and chief financial officer, and key external professionals, such as a healthcare M&A advisor (like one from VERTESS), attorney, and accountant.

2. Outline your ideal situation as the owner/leader

How much of your company are you willing to sell to acquire the resources needed to achieve your growth plan? In what capacity do you want to remain with the organization following a transaction? Answering these and related questions concerning what you envision as your company's post-transaction situation and your level of continued involvement is important to ensuring an optimal outcome when your company goes to market.

3. Assess your organization's personnel

Start with your immediate leadership team and cascade down. Ask yourself questions like: Do they have the drive, capability, and experience to take on this journey? Can you envision them as part of a company you hope will be a few or even several times larger in just a few years? If you cannot answer these questions with a confident "yes," you may need to consider changes to your personnel — which brings us to the next step…

4. "Topgrade" your leadership team

Before you proceed with bringing on a financial partner, you will want to consider topgrading your leadership team. Topgrade means two things: It can be a nice way of saying upgrade your team by replacing existing leaders with better qualified leaders, and it can mean improving your current team though training.

Why is topgrading important when contemplating a sale or recapitalization? This is not the time to hope you have the right people or look past shortcomings that make these individuals less effective in their roles. Be prepared to replace leaders or find them new roles that will be better fits in support of the overall growth plan, or at least consider whether training can strengthen your existing leadership team.

If you have a solid leadership team, it's still worth taking the time to identify knowledge gaps and then invest in training and executive coaching. A financial buyer will see much higher value in an organization that comes to the table with an all-star leadership team already in place and ready to put in the work that can help achieve growth goals.

5. Test the transaction waters

Even when owners are not necessarily looking to sell, they should always be putting feelers out to gauge buyer interest in their company. This way, they won't miss key opportunities to bring in a partner, sell, or recapitalize.

If you're serious about testing the waters, this is a great time to speak to a healthcare M&A advisor and receive a valuation on your organization. A good advisor will coach you on whether it is the right time to sell and provide advice on what you should do to better prepare for a successful sale. An advisor can share competitive insights (e.g., previous competitive sales and multiples) and paint a picture of what buyers are currently looking for — and, just as important, not looking for.

If you decide to sell, an advisor can be invaluable in creating that competitive environment that attracts buyers and drives up your sale price. In addition, an advisor will aid in all the transaction negotiations and help ensure the appropriate stock options and rollover equity are included in the deal. Learn more reasons why you should work with a healthcare M&A advisor in this column by fellow VERTESS team member, Bradley Smith.

6. Identify your ideal partner

If you feel it's time to grab that first bite of the apple and your organization is ready to scale with the right plan and the right team, think long and hard about what the ideal buyer looks like. Is it a financial partner? Do you want a strategic buyer who will make your company part of a larger competitor's organization? VERTESS's Alan Hymowitz recently discussed the three predominant healthcare buyer types and the challenges associated with completing transactions with these buyers in this column.

In most scenarios where owners want to stay on with their company and cash out even bigger in a few years, the financial buyer tends to be the clearer path forward. This is not to say a strategic partnership cannot work. In some cases, it's the right decision. However, when you are looking to drive the organization beyond your current capabilities, someone who is going to invest quickly into the company and target its key needs for growth tends to be the right partner.

This is also an area where a healthcare M&A advisor can prove very helpful. Most advisors, especially ones specializing in your line of business, have extensive resources and "rolodexes" of potential buyers and can quickly help you cast the right, wide net to initiate discussions with high-quality, potential buyers.

7. Fish or cut bait

After going through the processes discussed thus far, which should help you gain a better understanding of your company, its leadership, and your potential paths forward for sale or other type of transaction, it's time to make a decision. As the owner, you will want to do what is right for you and the future of your company, including your team and its customers. If you decide to proceed with pursuing a transaction, the work you have put in should help ensure a more successful outcome. If you feel it's best to wait a year so you can better get your house in order, you will be in an even stronger position when the time is right to proceed.

Understanding Your Healthcare Transaction Options

Selling your "baby" can be emotional but exciting as well. Following the steps above and better understanding your healthcare transaction options will put you in a much stronger position regardless of whether and when you sell.

If you have questions about pursuing a sale or recapitalization, reach out to our team of expert healthcare M&A advisors at VERTESS. We'd love to learn about your business and talk about how we can work together to achieve the best path forward for you and your company.

Gene Quigley

For over 20 years I have served as a commercial growth executive in several PE-backed and public healthcare companies such as Schering-Plough, Bayer, CCS Medical, Byram Healthcare, Numotion, and most recently as the Chief Revenue Officer at Home Care Delivered. As an operator, I have dedicated my career to driving value creation through exponential revenue and profit growth, while also building cultures that empower people to thrive in competitive environments. My passion for creating deals has helped many companies’ platform and scale with highly successful Mergers and Acquisitions.

At VERTESS, I am a Managing Director with extensive expertise in HME/DME, Diagnostics, and Medical Devices within the US and international marketplace, where I bring hands on experience and knowledge for the business owners I am privileged to represent.

We can help you with more information on this and related topics. Contact us today!

Considering the substantial global and national turmoil of the past several years, it should come as no surprise that the current mergers and acquisitions (M&A) landscape is complex, and navigating it is challenging. These are a few of the main reasons why healthcare business owners and buyers frequently reach out to the VERTESS team: They are looking for expert help with executing successful transactions that meet personal and professional goals in this dynamic landscape.

A significant role we play as healthcare M&A advisors is to answer questions from our clients and prospective clients about the issues affecting sellers, buyers, and transactions more broadly. Below are 10 of the questions we are being asked and answers intended to capture the current sentiments and strategic considerations in the M&A market.

Q1: M&A deals declined in the first half of 2024. What was the cause?

A: Several factors contributed to a fairly significant downturn in deal activity. Among them: high interest rates, lower current valuations than the same period last year, and political uncertainty.

Q2: Is M&A activity likely to increase in the near future?

A: Yes, there is a strong belief that M&A activity will rebound, and it will be driven by pent-up demand from both buyers and sellers as uncertainties that have been weighing on the market begin to resolve.

Q3: How are private equity firms responding to the current M&A landscape?

A: Many private equity firms are feeling increased pressure to sell, particularly those with portfolios comprised of numerous aging companies. Such a scenario is prompting an elevated focus on realizing returns to maintain investor confidence.

Q4: Are there signs of increased activity among sellers?

A: We have seen a noteworthy rise in sale preparations, which include the development of full-potential business plans and vendor due diligence engagements.

Q5: I heard that the need for M&A is greater now than in previous periods. Why is this the case?

A: We canpoint to the cumulative pressures of low-growth economic conditions combined with the need for businesses to adapt and innovate as reasons that are driving an elevated interest in strategic transactions.

Q6: Artificial intelligence (AI) continues to be a big topic of discussion within and outside of healthcare. How could AI influence M&A transactions?

A: Generative AI, which is the use of algorithms (e.g., ChatGPT) to create content, has the potential to disrupt various sectors, including healthcare. Disruption creates challenges and opportunities for companies. This then influences M&A strategies — potentially significantly, depending upon the extent and short- and long-term impact of the disruption.

Q7: When is the optimal time to sell my business?

A: The optimal time to sell is when you, as the owner, feel personally ready to move on to your next chapter, whether that's retirement, starting a new venture, or spending more time with family.

Q8: How should I take market conditions into consideration when deciding whether to sell my company?

A: While market conditions usually influence the valuation and sales price of a company, they should not be the primary factor in your decision to sell. The timing should be based on your readiness rather than trying to time the market. My colleague, Bradley Smith, tackled the topic of timing the market for an exit in this column.

Q9: How do rising interest rates impact the sale of my business?

A: Rising interest rates can affect the overall financing landscape, making it more expensive for buyers to obtain the loans they typically need to make acquisitions. However, it's important to understand that buyers adapt to these changes. While the cost of debt has increased, many buyers are shifting toward equity financing and still actively seeking acquisitions. Interest rates may influence buyer behavior, but they won't necessarily deter potential buyers from pursuing your business.

Q10: Is feeling burned out with my business a good reason to consider selling?

A: It's a very good reason to consider selling. When enthusiasm for owning and operating a company declines, it will likely negatively affect your business and its performance. This may not only hurt your company's valuation and thus its sales price, but it may also turn away buyers who see a company moving in the wrong direction.

Ready to Answer Your Healthcare M&A Questions

These questions and their responses help paint a picture of the current M&A market and key considerations for sellers and buyers. They also emphasize the importance of remaining adaptable and well-informed as you pursue a sale of your healthcare company or acquisitions of businesses. If you are looking for expert assist with transactions, including getting questions like those above answered, reach out. The VERTESS team of Managing Directors, who are focused on specific healthcare verticals, would welcome the opportunity to speak with you about your situation and what we can do to help ensure you achieve the best transaction outcome possible.

Anna Elliott CM&AA

With over 15 years of experience in healthcare technology, post-acute care, hospice, and urgent care, I am a highly experienced healthcare executive. I have successfully supported numerous private equity roll-ups and exits in the home healthcare sector. My extensive knowledge of the healthcare industry and my leadership in the M&A community, as a certified M&A Advisor (CM&AA) and member of the Executive Committee of the Chapter of the Association for Mergers & Acquisitions Advisors (AM&AA), distinguish me from others in the field.

Throughout my career, I have specialized in healthcare and have excelled in attracting healthcare technology firms and industries that are growing through Mergers + Acquisitions. I have a strong ability to target specific needs and opportunities in the business supply and demand process, resulting in over $150 million in value delivered to organizations.

As a co-founder of M&A Finders, a boutique Merger and Acquisition advisory firm in Pittsburgh, I have been able to pursue my passion for advocating on behalf of buyers and sellers in achieving their M&A goals. I am excited to bring my skills and network to VERTESS, where I have access to the necessary resources to further expand my impact in the healthcare industry.

We can help you with more information on this and related topics. Contact us today!

Last year, I wrote a column on "Choosing a Buyer: Private Equity vs. Search Fund vs. Strategic." As the title would suggest, this well-received piece discussed the three predominant buyer types — private equity group (PEG), search fund, and strategic buyer — healthcare business owners are likely to encounter when they decide it's time to sell their company and what sellers should know about them. I have had the good fortune of closing deals with each of these buyer types over the past few months, so I thought it would be worthwhile to do a follow-up piece to this column — one that discusses the challenges associated with getting transactions involving these buyers to and across the finish line.

Each buyer type has its own challenges, and understanding how to navigate them most effectively and efficiently is one of the most important roles I play as a healthcare M&A advisor. As I collaborate with seller clients to overcome these roadblocks and any curveballs, I am focused on achieving not only the best valuation for clients but also the deal structure that would most benefit them. Understanding how buyer types differ in how they structure offers and prefer to proceed through the due diligence phases is essential to achieving a seller's goals and ultimately a successful transaction and transition.

Let's take a closer look at each of these three buyer types and key points to know about their acquisition approach.

Private Equity

PEGs are also referred to as financial buyers. As this name suggests, their approach is largely based on a healthcare company's financials. Broader due diligence focuses primarily on intense auditing of documents like profit and loss (P&L) statements, balance sheets, and bank statements for the trailing 12 months up until 30 days prior to close.

Legal due diligence will focus on areas like contracts, state boards, and regulatory issues. Sellers should expect weekly due diligence calls with a PEG's legal, tax, regulatory, management, accreditation, licensing, and human resources representatives, and must be prepared to answer their questions and produce any documents requested. At closing, other legal steps must be completed, such as a reorganization.

The deal structure will likely include shared risk, rollover equity, non-competes, earnouts, and employment agreements. Given this continued involvement from ownership, it is worth noting that PEGs used to largely approach acquisitions with a 5-7-year turnaround plan. That plan can now last longer, even surpassing 10 years.

A PEG is more likely to desire keeping the existing management team in place, unless a necessary change is identified during due diligence.

Search Fund

Also referred to as unfunded sponsors, search funds take a "buy-and operate" approach to acquisitions. This translates to current owners usually only remaining for a short consulting period post close.

Search funds come to transactions with previous and fairly extensive knowledge about the company's sector and what's required for success within it. These buyers focus less on financials and the likes of P&L and balance sheets. They look for profitable companies with strong potential growth and return. These are important given that search funds usually have no growth capital, which places greater emphasis on current and potential legacy growth.

Search funds tend to require strict non-competes and expect that current, essential staff will remain with the company while also usually turning over upper management. Scrutiny and audits of an acquisition focuses on regulatory issues, changes of ownership (CHOWs), and any legal issues past and present.

Following the signing of a letter of intent, search funds work to secure funding for the acquisition. The capitalization table (i.e., cap table), which shows a company's ownership structure, will change daily or weekly depending on what's discovered in due diligence up until the day a transaction closes. Each search fund investor has its own requirements.

Finally, search funds tend to hold onto assets longer than PEGs.

Strategic Buyers

These are typically what are referred to as "non-financial" (to contrast PEGs) or "buy-and-build" buyers. They tend to already be well-established in the industry in which they are pursuing an acquisition. Thus, they come to the transaction table with vast knowledge but not necessarily the personnel, so they tend to need the talent and resources that come with the acquisition.

As the descriptor of non-financial buyer suggests, strategics are less focused on financials of the company. Rather, the acquisition is motivated by one or more of needing the acquisition's location, talent, contracts, or customers, or a desire to eliminate a competitor. Strategic buyers also view acquisitions as a way to pursue and further achieve economies of scale.

Strategic buyers tends to have a shorter due diligence period than the other buyer types.

Private Equity, Search Fund, and Strategic: Completing Your Sale

If you're operating a good company, finding interested buyers is usually easy. What comes next is much more difficult, which points to the value of working with a healthcare M&A advisor, like those at VERTESS. Determining a desired exit strategy and optimal buyer type, bringing a company to market, attracting the right buyers, properly vetting buyers, selecting a buyer, and finally navigating the subsequent transaction processes all include challenges that can derail an optimal and successful outcome.

The VERTESS team is comprised of advisors with extensive experience operating healthcare companies and working with all buyer and seller types. We support clients through the entire M&A process and beyond, which includes helping clients achieve a smooth post-transaction transition.

Reach out to learn more about how VERTESS is helping business owners like you achieve successful sales.

Alan Hymowitz, CM&AA

During the past decade I have facilitated numerous, diverse M+A transactions in the pharmacy marketplace across the country, as well as providing strategic consultation to national pharmacies and similar organizations. Prior to becoming an M+A advisor, I was a “hands on” owner and manager in the pharmacy and home infusion healthcare marketplace for over 15 years, and successfully sold my pharmacy to a national company after growing and diversifying our income streams in a very competitive market. My specialties in the pharmacy and home infusion marketplace include long term care, retail pharmacy, specialty pharmacy, and home healthcare, and I have attained the URAC Accreditation and Specialty Pharmacy Consultant designations, in addition to other recognition. My educational background includes a Bachelor of Arts from Rutgers University and a Master of Arts from the John Jay College of Criminal Justice.

We can help you with more information on this and related topics. Contact us today!

When we are approached by healthcare business owners contemplating a sale and researching their options for assistance, a common question we're asked is: "Why should I hire a specialized healthcare mergers and acquisitions (M&A) advisor for my company?"

The simple answer is that an M&A advisor who specializes in healthcare is more likely to help owners achieve successful transactions, with "success" including a fair sales price and the passing along of the business to a company that will continue to treat staff and customers well.

9 Reasons to Work With a Healthcare M&A Advisor

For a more complete answer to why healthcare business owners should work with healthcare M&A advisors, here are nine reasons.

1. Leveraging extensive experience

A healthcare M&A advisor generally has experience in representing companies in various healthcare verticals and broad knowledge of the healthcare industry. This will help a business owner prepare for the sales process with insights about the owner's unique market. When the advisor is part of a larger healthcare M&A advisory firm, like VERTESS, they are further supported by other advisors and experts who can share additional insights.

2. Improving the selling process

Selling a healthcare business is a complex process filled with multiple tasks that can be overwhelming and often underestimated by owners given that most have not experienced the sale of a company before. Simultaneously, a healthcare business owner is typically busy running their company, which limits the amount of time and energy that can be allocated to the sales process.

Bringing aboard a healthcare M&A advisor can smooth the transaction process while better ensuring a high return on investment. There are always obstacles and bumpy roads in the process of selling a healthcare company, but a savvy advisor helps sellers navigate them and avoid the many reasons transactions can fail to secure a successful agreement with a buyer or investor.

3. Maximizing healthcare business value

A healthcare M&A advisor will be able to market the healthcare company to more targeted buyers, and this will often lead to more high-quality partner options for the seller. More value could mean creative strategic partnerships, maintaining the owner's legacy, retaining a core management team, and higher price and/or better terms in the sales agreement.

4. Integrating healthcare knowledge into marketing

Effective healthcare M&A advisors integrate their knowledge of a specific healthcare vertical and broader healthcare industry knowledge into their marketing approach. Utilizing established industry relationships and networks, a healthcare M&A advisor can connect sellers with buyers and investors that have the highest appreciation for the seller's market segment and potential value of their business.

5. Showcasing value

Through their many years working in the healthcare industry, a veteran M&A advisor has learned what financial analysis and presentation will resonate most with potential buyers. As a result, they will make sure that marketing materials feature a professional financial analysis that contributes to the highest valuation.

6. Painting a complete picture

Skilled healthcare M&A advisors generate a confidential information memorandum (CIM) — otherwise known as "the marketing book" — to tell a healthcare company's story to prospective buyers. The CIM includes information that speaks to significant areas of interest for buyers, such as successes, differentiators, growth opportunities, local market dynamics, and larger healthcare market trends. The completeness of the CIM is usually correlated to the healthcare M&A advisor's understanding and experience and their ability to tell the compelling story of the healthcare business and its owner(s).

7. Managing the healthcare transactions process

Competent healthcare M&A advisors will manage a sales process in which various buyers are screened by level of interest, commitment, and financial qualification to complete a fair transaction. Within their networks, healthcare M&A advisors often access unique market intelligence to assist them in their representation and execution.

8. Closing the deal

Healthcare M&A advisors often know about unique, market-related nuances that will help with the final negotiation of deal terms. This understanding can help guide the business owner through escrows, non-compete or interim management agreements, and other critical decisions on the way to a successful sale.

9. Delivering value

The ninth and final reason to work with a healthcare M&A advisor — delivering value — is a composite of the above. In a time of much turbulence and opportunity in today's healthcare industry, an accomplished healthcare M&A advisor often brings value that far exceeds their fee while helping sellers reach the goals that were established prior to starting the sales journey.

VERTESS: A Top Healthcare M&A Advisory Firm

If you're contemplating a sale of your healthcare business and are looking for a partner that can help you achieve your sales goals, reach out to VERTESS. Our team of Managing Directors, who specialize in specific healthcare verticals, has the extensive healthcare transaction experience that leads to more successful sales. This track record recently helped us earn the distinction of being named the #1 lower middle market investment bank for the first quarter of 2024 by Axial, and I was proud to be recognized as the advisor for one of Axial's top 8 deals in 2023.

To learn what VERTESS advisory services can do for you and your healthcare business, reach out to us today!

Bradley Smith ATP, CM&AA

For over 20 years I have held a number of significant executive positions including founding Lone Star Scooters, which offered medical equipment and franchise opportunities across the country, Lone Star Bio Medical, a diversified DME, pharmacy, health IT and home health care company, and BMS Consulting, where I have provided strategic analysis and M+A intermediary services to executives in the healthcare industry. In addition, I am a regular columnist for HomeCare magazine and HME News, where I focus on healthcare marketplace trends and innovative business strategies for the principals of healthcare companies.

At VERTESS, I am a Managing Director and Partner with considerable expertise in Private Equity Recapitalizations, HME/DME, Home Health Care, Hospice, Medical Devices, Health IT/Digital Health, Lab Services and related healthcare verticals in the US and internationally.

We can help you with more information on this and related topics. Contact us today!

FORT WORTH, Texas, July 24, 2024 /PRNewswire/ -- As healthcare-specific merger and acquisition (M&A) advisors, VERTESS (https://vertess.com/) has been asked frequently by healthcare business owners "How is the market in 2024?" and "Is now a good time to sell my company?" We understand that most owners believe they must wait until the market tea leaves reveal the optimal time to sell to secure the best price. In response, we can speak to significant macro conditions, such as interest rate activity, inflation shifts, and global events. Those all will generally have an impact on prices of transacted companies. However, the far more critical indicator for when a sale is optimal will always be when the owner is ready to move on to whatever is next in life.

At VERTESS, we recognize that owners are likely the most important person to the business. They are its biggest cheerleader. They have invested more in it than anyone else, so they typically will make the biggest and greatest impact on the business. If owners wait to try to time the market or take advantage of some other perceived opportunity, they run the risk of souring on the business and becoming burned out or disenfranchised. If that happens, the business is going to suffer, and that will likely lead to a decline in sales price.

Of course, interest rates continue to be a substantial issue affecting healthcare businesses. They are high and the Fed isn't likely to start reductions until the end of this year or the beginning of 2025 due to sticky inflation and a strong labor market. If an owner wants to get a bank loan for their business, they're looking at 10-plus percent. How has the market responded to rising interest rates? Bank loan activity has slowed, and people are deploying more equity. Private equity firms are maybe doing one or two turns of debt equity, with the rest of their payment coming out of pocket. Two years ago, when interest rates were about half of what they are now, these firms might do half a deal in debt.

Buyers find a way to evolve to what's happening in the market and buy the businesses they want to acquire. Buyers, especially strategics, bake acquisitions into their growth strategies. It's their "buy-and-build" strategy. Buyers know they're going to grow organically every year at X rate, and then they plan for inorganic growth at a certain rate, which is accomplished through acquisitions. Inorganic growth is typically identical to, if not larger than, organic growth rate.

Regardless of the market today or what's projected over the next 12-plus months, buyers are going to set acquisition mandates and work to achieve them. Buyers need to buy companies to scale their businesses. It's part of part of the fabric of their operations and what they're used to doing — and that's not going to change, regardless of what's happening nationally and internationally.

"Ultimately, owners should know what's happening in the market as this can affect matters like budgeting, staffing, and purchasing. But when it comes to selling your company, don't let what is happening in the market influence your plans. The risks of doing so far outweigh any potential benefits," cautions VERTESS Managing Director/Partner Bradley Smith. "If you own a successful business, you should be able to find a buyer and one that offers you a good, fair price, regardless of what's happening in the market. The key to a successful sale is to run a proper process that results in all interested buyers — and the right buyers — coming together simultaneously and making their best offers. That's how you'll know you're getting the best price for your company."

For more information, please contact Vaughne Glennie at 380788@email4pr.com or +1.520.395.0244.

FORT WORTH, Texas, July 16, 2024 /PRNewswire/ -- VERTESS (https://vertess.com), a leading healthcare mergers and acquisitions (M&A) advisory firm, is pleased to announce the successful completion of a third pharmacy deal this year. This deal closely follows two additional pharmacy transactions completed in Q2.

Keystone Specialty Pharmacy (https://keystone-pharmacy.com/), a customized, specialty pharmacy out of Mississippi, was purchased by Novastone Capital Advisors (NCA) (https://www.novastone-ca.com/index.php), a Switzerland-based private equity firm, as part of their Entrepreneurship through Acquisition (ETA) Program. Keystone prides themselves on offering health care providers new resources to treat serious infections while also being committed to maintaining the highest ethical standards in business. Dr. Lisa Piercey, NCA's Entrepreneur, will lead the pharmacy as it continues its mission of providing critical care.

The transaction was overseen by VERTESS Managing Director, Alan Hymowitz, who previously owned and operated a pharmacy before his tenure at VERTESS. His unique background was invaluable in leading this transaction to a successful conclusion. He noted what a demanding and lengthy process this transaction was, but that he is thrilled for his clients to see this deal across the finish the line.

Keystone owners, Jeffrey and Kim Clark, reflected on the transaction process sharing, "Alan Hymowitz and the team from VERTESS understood the importance of finding a strategic investor who would continue our mission 'Our goal is to heal and not refill.' VERTESS found the ideal fit for our pharmacy, one who we have confidence will take care of our patients with excellence while expanding the business we started. We are extremely grateful to Alan, David Coit, and the rest of the VERTESS team for their diligence and expertise in bringing our deal to close. Their guidance through this process has been a blessing to us both."

For more information, please contact Vaughne Glennie at 380413@email4pr.com or +1.520.395.0244.

Volume 11, Issue 12, July 2nd, 2024

By: David E. Coit, Jr., DBA, CVA, CVGA, CM&AA, CBEC, CAIM

Why should a buyer's costs of integrating an acquired company be of interest to the seller? The most important reason is that sellers often pay part or all the integration costs of the buyer. According to McKinsey & Co., the average cost of integration is between 15% and 20% of an acquisition's purchase price.

How do buyers' integration costs become a concern for sellers? Buyers typically determine the offering price based on expected future cash flows received from the acquired company. When buyers estimate future cash flows, they often include the anticipated costs of integrating the acquired company. Thus, the purchase price is often net of the buyer's expected integration costs.

If you're considering a sale of your healthcare company, you might be wondering: What can I do to influence the buyer's cost of integration?

That's a great question! There are several actions sellers can take before going to market that can reduce the buyer's integration costs. Moreover, those cost savings may allow potential buyers to increase their offering price because of a perceived increase in first-year cash flows from the acquisition.

How to Cut Healthcare Acquisition Integration Costs

Let's discuss eight areas where sellers may want to take steps before selling their company that can reduce a buyer's integration costs and potentially increase offers and the final sale price.

1. IT software applications

Buyers typically migrate the information technology (IT) used by an acquired company to match the applications the buyer uses. Software migration can be a costly and time-consuming process, especially if the seller is using legacy systems and outdated technology, in-house developed software, and/or has inaccurate or incomplete data. On the other hand, using widely used, industry-specific applications and having clean and current data will considerably ease the migration process.

In addition, providing buyers with a listing of IT applications used, the methodology of data collection and data verification, and a scheduled IT software maintenance program will allow buyers to better determine the estimated time and expense of IT integration.

2. Repair and maintenance

Believe it or not, some sellers defer routine repair and maintenance in the months leading up to the sale of their business. While this may seem like a good way to increase the seller's cash flow before selling their business, buyers will likely discover such deferred expenses during due diligence and predictably take a dim view of such actions. Moreover, buyers will estimate their costs of remedying or mitigating the deferral.

It's better to keep up with scheduled repairs and maintenance as though the business wasn't being sold than having buyers decrease their offering price to account for these necessary expenses. However, sellers should not needlessly incur excess repair and maintenance costs before going to market. Keep in mind that companies sell for a multiple of cash flow. As such, every dollar increase in cash flow returns a greater dollar amount in the price of the company.

3. Turnover