The only constant for home health care agencies is change. For many owners, change is both demanding and fatiguing. At some point, owners start thinking about exiting their company. Some owners elect to pass ownership down to their adult children. Some stop taking on new clients/patients and simply close their doors. Others seek to sell their company in the marketplace. This column is written for those owners considering selling in today's marketplace.

The merger and acquisition (M&A) market for home health care providers is currently very robust, with buyers actively acquiring strong agencies. As such, this may be the best time to sell if you're looking to get the highest price, best terms, and well-suited buyers.

Why Are Buyers Eager to Acquire Home Health Care Companies Now?

Home health care agencies are one of the fastest-growing industries in the healthcare sector. Due to an aging population, an increase in chronic diseases, the growth of physician acceptance of home health, medical advancements, increased demand for home-based care (especially for the elderly or in times of a pandemic), and a movement toward cost-efficient treatment options from public and private payors, the industry has flourished. Moreover, the industry is anticipated to grow over the coming years, which will allow providers to compete effectively with institutional care agencies, such as hospitals.

According to the Medicare Payment Advisory Commission's (MedPac) March 2025 report to Congress, the home health market remains broad and accessible. More than 12,000 home health agencies participated in Medicare in 2023, and over 98% of fee-for-service beneficiaries live in a ZIP code served by at least two agencies, underscoring the depth of provider availability across the country. Total Medicare spending on home health services reached $15.7 billion in 2023, reflecting continued investment in the benefit. At the same time, operating performance remains strong, with freestanding home health agencies reporting an all-payer margin of 8.2% and Medicare fee-for-service margins exceeding 20%, indicating that payments continue to outpace costs for many providers.

IBISWorld describes the home care industry as highly fragmented, with no single provider accounting for more than 5% of total market share, reflecting a market composed largely of small, independent agencies. This fragmentation creates opportunities for consolidators to leverage back-office efficiencies, scale operations, and expand market share through acquisition.

If you're thinking of selling your home health care agency, you should know the following:

- The market is strong now because of the vast amount of capital searching for well-performing agencies. It's unclear how long this will last and when it will inevitably slow down. The market can change quickly, and you may lose your opportunity to sell at a favorable price.

- As acquisitions and consolidations continue, you'll likely be competing against larger, better capitalized companies. The competitive landscape is changing. Larger competitors are likely to offer a broad range of services, a strong marketing campaign built around an established brand, efficient business processes, and the ability to bid for value-based contracts with large payors.

- An aging base of independent home health agency owners is contributing to ongoing consolidation, as more agencies explore succession planning and acquisition opportunities. As a result, we expect an increasing number of home health care companies to seek buyers in the coming years.

- Many agencies have already found value in merging to create economies of scale and the resources to better compete with larger organizations.

What Drives Valuation When Selling a Home Health Agency?

In our experience, the most crucial feature buyers are looking for in a company is profitable growth. Buyers want to know that they can take what you have built and build on it. But smart buyers also weigh risks versus rewards when considering the purchase of a company. They'll want to see that your strengths far outweigh your weaknesses (i.e., opportunities for improvement).

Risk Factors That Could Devalue Your Home Health Agency

Some of the perceived risks in the home health care industry are as follows:

- Despite strong growth, industry profitability has been under pressure.

- Reimbursement has been under pressure for more than a decade, including several consecutive years of payment cuts, hindering operating profit growth.

- Although healthcare reform expanded access to insurance for some industry patients, many states chose not to expand access to federal healthcare.

- While in-home health care agencies have always struggled with caregiver retention, the current job market makes growing a workforce nearly impossible.

- There are increasing hospital competitors, fueled, in part, by various federal initiatives (e.g., Acute Hospital Care at Home (AHCAH)).

Advantages Buyers Are Looking for in Home Health Businesses

Most home health buyers have a checklist mentality, where they'll be looking to see that you have at least some of the attributes below:

- Diverse reimbursement/payors

- Strong reputation and quality of services

- Expansion in chronic disease management

- Keen understanding of the current and future required level of staffing

- Relevant certificate of need (CON) moratoriums or other licensure requirements, where applicable

- Continued investment in infrastructure and actions to seek efficiency opportunities

- Low revenue seasonality

- High population base with the right client demographics

- Tenured, experienced workforce with low employee turnover

- Reliable and consistent referral source and/or contracts with providers

- Clean billing audit

- Good revenue growth

- Adjusted earnings before interest, taxes, depreciation, and amortization (EBITDA) margins in the 10%–30% range

- Understanding of subcontractor versus employee handling of service delivery

- Creative staffing with maximization of billable hours

- Multiple service delivery locations, including community-based access

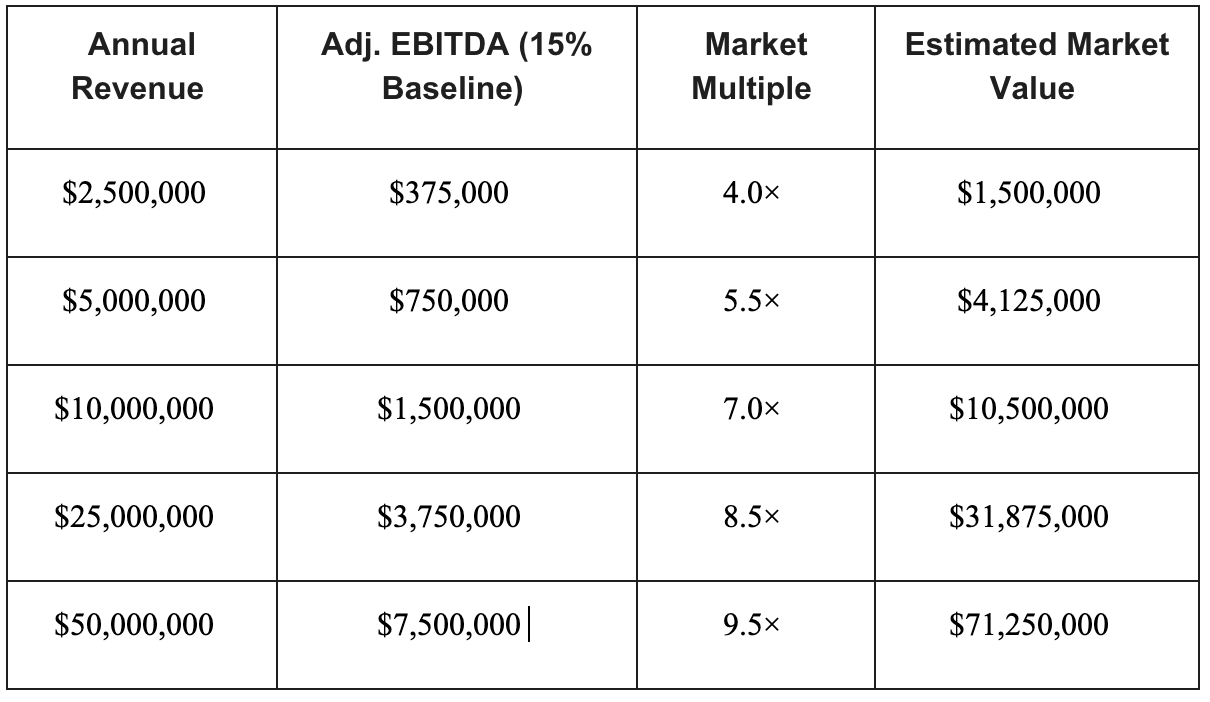

How Much Will Home Health Buyers Pay (Market Multiples)

Typically, buyers go through their risk/reward analysis and come up with an offering purchase price. Usually, the offering price is based on a multiple of normalized or adjusted EBITDA. Adjustments to EBITDA include nonrecurring expenses, such as one-time legal fees; discretionary expenses, such as charitable contributions; and owner-related personal expenses; such as excess owners' salaries and auto lease expenses.

Market multiples refer to the estimated purchase price, or enterprise value, related to adjusted EBITDA. Market multiples for home health care agencies typically range from approximately 5x–8x adjusted EBITDA for small to mid-sized providers, with higher multiples for larger, higher-performing agencies. In practice, smaller agencies tend to transact in the mid-single-digit range, while scaled, high-performing platforms can achieve high-single-digit or higher multiples depending on size, margins, and growth profile. Agencies offering both home health and hospice services often command higher blended multiples, reflecting greater earnings stability and broader service capabilities.

A particular provider falls within the range based on quantitative factors such as historical and projected financial performance, and qualitative factors as highlighted above in the "What Drives Valuation When Selling a Home Health Agency?" section. Moreover, size matters, as larger revenue agencies attract more buyers than smaller agencies.

The following table provides illustrative home health agency valuation estimates. Actual market multiples may vary.

2026 Home Health Agency Valuation Estimates

There are outlier market multiples in unique M&A transactions where optimal buyer/seller synergies push valuations above the norm. Moreover, market multiples change over time depending on the overall economy, regulatory and reimbursement modifications, and industry trends.

Note that using market multiples is an excellent way to estimate a company's value. It is most often accompanied by using a discounted cash flow approach. The discounted cash flow approach estimates a company's value by calculating the future cash flows expected from the company and putting the future cash flows into today's dollars. However, the market multiple approach provides a reasonable shortcut for estimating the value of a company.

How Will My Home Health Company's Debt Affect Its Value?

The market multiples above are used to determine the enterprise value of companies, not the equity value. Most small businesses are sold debt-free, which means that buyers assume that all of the company's debts (not to be confused with non-debt current liabilities) will be paid off by the seller at the time of closing. However, there are occasions where a buyer wishes to assume the company's debt as a way to finance part of the purchase price.

Net Working Capital Adjustments to Price

Working capital is usually calculated by subtracting current assets from current liabilities. Net working capital is used to gauge a company's operating liquidity at a particular point in time.

While all the accounts that make up net working capital are listed on a company's balance sheet, inclusion or exclusion of individual accounts is often negotiated between buyers and sellers. Accounts usually included in the calculation of net are cash, accounts receivable (A/R), inventory, prepaid expenses, accounts payable (A/P), and accrued liabilities. Other current assets and current liabilities that may be included in net working capital include short-term investments, cash advances to employees, insurance claims, owner receivables, notes receivable, security deposits, A/R due from affiliates, 401(k) payables, A/P due to affiliates, customer deposits, and income taxes payable.

Buyers expect a normal amount of net working capital at closing to ensure adequate liquidity the day after the purchase date. Buyers expect a normal amount of collectible A/R, sellable inventory, no past-due A/P, etc.

If there has been a change in the amount of normalized net working capital prior to the closing date, the purchase price of the company is usually increased or decreased accordingly.

Net working capital is an integral part of a company's overall value. As such, it's critical that a normalized amount of net working capital transfers to the buyer at closing.

Capital Expenditure Adjustments to Price

Capital expenditures that are not ongoing maintenance capital expenditures are expenses expected to generate future benefits, such as the cost of purchasing vehicles, information technology equipment, etc. Future projected capital expenditures decrease cash flow to the buyers. Buyers typically subtract future expected annual capital expenditures from EBITDA to estimate future cash flows. A decrease in EBITDA will lead to a lower purchase price.

Selling in Today's Home Health Market

Owners who have prepared their home health company for sale will find a robust market of eager buyers willing to pay for value. Market conditions are currently very favorable to sellers.

If you'd like to know the market value of your agency, or if you're ready to talk about selling your company, reach out to VERTESS to talk to an expert advisor in home health mergers and acquisitions.